Subscriptions

The Richmond Fed publishes several quarterly magazines each year. Order recent or archived issues or subscribe to our publications.

The Richmond Fed publishes several quarterly magazines each year. Order recent or archived issues or subscribe to our publications.

As a consequence of the Federal Reserve's response to the financial crisis of 2007–08 and the Great Recession, the supply of reserves in the U.S. banking system increased dramatically. Historically, over long horizons, money and prices have been closely tied together, but over the past decade, prices have risen only modestly while base money (reserves plus currency) has grown substantially. A macroeconomic model helps explain this behavior and suggests some potential limits to the Fed's ability to increase the size of its balance sheet indefinitely while remaining consistent with its inflation-targeting policy.

Macroeconomic models have long predicted a tight long-run relationship between the supply of money in the economy and the overall price level. Money in this context refers to the quantity of currency plus bank reserves, or what is sometimes called the monetary base. As the monetary base increases, prices also should increase on a one-to-one basis.

This theory also has been confirmed empirically. According to Robert Lucas of the University of Chicago, who received the Nobel Prize in Economics in 1995 in part for his work in this area, "The prediction that prices respond proportionally to changes in money in the long run … has received ample — I would say, decisive — confirmation in data from many times and places."1

But recent events have called the relationship Lucas spoke of into question. Over the past decade, the monetary base in the United States grew at an average annual rate of 16 percent as the Federal Reserve dramatically increased the amount of reserves in the banking system in response to the financial crisis of 2007–08 and the Great Recession. At the same time, prices grew at only 1.8 percent per year on average. This Economic Brief provides one explanation for this behavior and examines whether there might be limits to the decoupling of money from prices.

A Period of "Unconventional" Policy

In response to the financial crisis of 2007–08, the Fed employed a number of extraordinary measures to stabilize the financial system and help the economy weather the Great Recession. Between the summer of 2007 and the end of 2008, the Fed created several lending facilities to provide liquidity to the financial system while the Federal Open Market Committee (FOMC) brought its target for the federal funds rate down from 5.25 percent to effectively zero. With no more room to cut rates, the Fed turned to more unconventional policies, such as large-scale asset purchases known as "quantitative easing" (QE). The Fed used QE and related programs (such as Operation Twist) in an effort to lower long-term interest rates to stimulate the economy and spur recovery from the Great Recession.2 These actions grew the Fed's balance sheet to roughly $4.5 trillion.

In order to pay for the QE purchases, the Fed issued reserves.3 Banks have always been required by law to hold some reserves, but historically they have held very little in the way of "excess" reserves because the opportunity cost of doing so was high. Before 2008, reserves paid no interest, so choosing to hold excess reserves meant banks would need to forgo whatever interest they could earn in the market. Banks that found themselves short of their reserve requirement at the end of the day could borrow them overnight from banks that ended the day with a surplus, further reducing any incentives to hold excess reserves. This low-reserve environment was intertwined with how the Fed traditionally set monetary policy. The Fed's target policy rate, the fed funds rate, is the rate that banks charge one another to borrow reserves overnight. By changing the supply of reserves in the market, the Fed could target the fed funds rate it desired, executing monetary policy in line with the decisions of the FOMC.

In October 2008, the Fed gained the authority to pay interest on reserves, allowing it to set a floor for market rates while increasing the supply of reserves in the banking system. This tool soon became less important as the Fed's target rate fell closer to its effective lower bound in December 2008. But, in general, by paying interest on reserves, the Fed could give banks greater incentives to hold excess reserves than in the past.

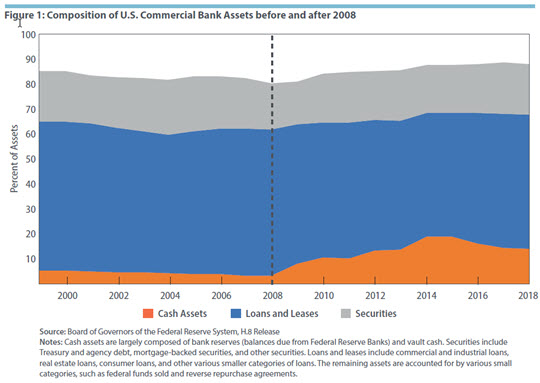

From late 2008 through 2014, the amount of reserves in the banking system grew significantly as a result of the lending facilities and the QE programs, with reserves becoming a much larger proportion of total assets on banks' balance sheets. (See Figure 1.) At various times during the unconventional monetary policy period, many policymakers expressed concerns that the massive increase in reserves from QE could eventually trigger inflation. For example, in a 2012 speech, then Philadelphia Fed President Charles Plosser warned that "once the recovery strengthens — and it surely will — long rates will begin to rise and banks will begin lending out their excess reserves. … In such an environment, policymakers might need to tighten policy quickly to contain inflationary pressure."4 But as the recovery proceeded, inflation remained low despite the unprecedented level of excess reserves in the system. Why?

Modeling an Economy with Large Excess Reserves

To improve our understanding of this issue, it is useful to study a model of the macroeconomy that explicitly includes a banking system with a nontrivial balance sheet. In a recent paper, one of the authors of this Economic Brief (Ennis) studies such a model.5 In the model, bankers can make loans and also can borrow from other banks in the interbank market. There is a central bank that controls the total supply of monetary assets (reserves plus currency) in the economy but not the split (that is, banks determine whether to hold reserves or transform them into currency). In the model, as in reality, only banks can hold reserves.

When reserves are "scarce" or when banks have no reason to hold excess reserves (for example, because reserves pay no interest), the model predicts that there will be little to no demand for excess reserves. Under these conditions, prices move together with the quantity of monetary assets. This aligns well with the observed real-world, long-run relationship between prices and monetary assets that Lucas referred to in his 1995 lecture.

On the other hand, if the central bank pays interest on reserves at market rates, banks are willing to hold excess reserves, and prices no longer need to move in step with the quantity of money. In this situation, the quantity of reserves in the banking system could increase considerably without any significant effect on the price level. This configuration closely matches the monetary behavior of the U.S. economy over the past decade.

Limits to the Decoupling of Money and Prices

As experience demonstrates — and Ennis's model explains — paying a market rate on reserves allows a central bank to increase the supply of monetary assets without generating a corresponding response in the price level. But does the central bank face limits in its ability to continue increasing the supply of reserves while maintaining a stable price level? In September 2012, the Fed announced its third QE program. This program differed from the first two in that the Fed agreed to purchase a fixed amount of assets ($85 billion) per month "indefinitely." Simultaneously, the Fed pledged to maintain its inflation target of 2 percent. The fact that the program had no fixed duration implied that the total increase in the size of the balance sheet and, in particular, excess reserves in the banking system were left unspecified.

Relatedly, the recently released FOMC transcripts for 2013 reveal that some participants at the time worried about the possibility of facing limits in the Fed's ability to continue QE purchases for an extended period of time. In the April/May 2013 meeting, then Dallas Fed President Richard Fisher asked "what the practical limits are on the size of our balance sheet."6 Fed staffers recognized the uncertainty and complexity of the question while also acknowledging that a limit must exist as eventually "there won't be anything left for us to buy." Ultimately, the Fed ended asset purchases in 2014 before these issues became more pressing, but the question of potential limits to QE remains pertinent for future policymakers.

Beyond the extreme case of running out of assets to buy, there may be other, more subtle limits to the Fed's ability to increase the size of its balance sheet without triggering a corresponding increase in the price level. Ennis's model suggests one such limit. In particular, the model indicates that a growing supply of reserves eventually could become incompatible with stable prices even if the central bank has the authority to pay interest on reserves. Because only banks can hold reserves, the amount of reserves they can hold is tied to the size of their balance sheets. If banks face capital requirements (due to regulation or other market-induced reasons), then the total value of reserves that banks can hold is linked to the total amount of bank capital available in the economy. Eventually, as bank capital becomes scarce, the cost of holding additional reserves becomes higher than the interest paid on reserves and banks again become sensitive to the quantity of reserves outstanding. At this point, the model predicts that prices would once again move together with the quantity of monetary assets.

Looking Forward

The potential limits identified by the model never materialized for the Fed in the aftermath of the Great Recession, but knowing about them may prove useful for policymakers in the future.7 After the third QE ended, the Fed maintained the size of its balance sheet by reinvesting any securities that matured. Starting in October 2017, the Fed began a process of normalization for its balance sheet by reducing the value of securities it reinvests by a fixed amount each month. That said, many economists and Fed officials anticipate that the Fed's balance sheet will remain larger than prior to the crisis of 2007–08 at least for some time to come.

At the same time that it has been normalizing its balance sheet, the Fed also has been raising its target for interest rates. The ability to pay interest on reserves has been crucial to allowing the Fed to raise its target rate while there are still significant excess reserves in the banking system. Despite these rate increases, due to various secular reasons, interest rates are expected to remain historically low for a long time. This could mean that the unconventional tools that the Fed employed during the last crisis may become more common in future downturns if the effective lower bound on interest rates again becomes binding for the conduct of monetary policy. Improving our understanding of the workings of such tools, and their limitations, is therefore an important objective of economic research, and the model and ideas discussed here contribute to that collective effort.

Huberto M. Ennis is the group vice president for macro and financial economics, and Tim Sablik is an economics writer in the Research Department at the Federal Reserve Bank of Richmond.

Robert E. Lucas Jr., "Nobel Lecture: Monetary Neutrality," Journal of Political Economy, August 1996, vol. 104, no. 4, pp. 661–682.

The Fed's Maturity Extension Program and Reinvestment Policy that began in September 2011 and ran through the end of 2012 was called "Operation Twist," in reference to a similar program the Fed employed in the 1960s. In the more recent case, the Fed sold a total of $667 billion in short-term Treasuries and used the proceeds to buy longer-term Treasuries. This was a way for the Fed to put downward pressure on longer-term interest rates and provide additional easing during the recovery from the Great Recession. See Tim Sablik, "Jargon Alert: Operation Twist," Federal Reserve Bank of Richmond Region Focus, Fourth Quarter 2012, p. 10.

See Todd Keister and James J. McAndrews, "Why Are Banks Holding So Many Excess Reserves?" Federal Reserve Bank of New York Current Issues in Economics and Finance, December 2009, vol. 15, no. 8.

Charles I. Plosser, "Good Intentions in the Short Term with Risky Consequences for the Long Term," Speech at the Cato Institute 30th Annual Monetary Conference, Washington, D.C., November 15, 2012. See also Huberto M. Ennis and Alexander L. Wolman, "Excess Reserves and the New Challenges for Monetary Policy," Federal Reserve Bank of Richmond Economic Brief No. 10-03, March 2010.

Huberto M. Ennis, "A Simple General Equilibrium Model of Large Excess Reserves," Journal of Monetary Economics, October 2018, vol. 98, pp. 50–65. Other papers that also have studied this question include Mark Gertler and Peter Karadi, "A Model of Unconventional Monetary Policy," Journal of Monetary Economics, January 2011, vol. 58, no. 1, pp. 17–34; Vasco Cúrdia and Michael Woodford, "The Central-Bank Balance Sheet as an Instrument of Monetary Policy," Journal of Monetary Economics, January 2011, vol. 58, no. 1, pp. 54–79; and Stephen D. Williamson, "Interest on Reserves, Interbank Lending, and Monetary Policy," Journal of Monetary Economics, forthcoming.

"Meeting of the Federal Open Market Committee," April 30–May 1, 2013, pp. 114–115.

Ennis and Wolman study in detail the distribution of reserves across banks in the United States and document that most of the banks holding large excess reserves during the QE period were not facing tight capital constraints. See Ennis and Wolman, "Large Excess Reserves in the United States: A View from the Cross-Section of Banks," International Journal of Central Banking, January 2015, vol. 11, no. 1, pp. 251–289.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Receive a notification when Economic Brief is posted online.