Are Markets Becoming Less Competitive?

Economic Brief

June 2019, No. 19-06

National markets in many U.S. industries seem to be increasingly dominated by large companies. Some policymakers have argued that this growing market concentration is a sign of weakening competition, but concentration by itself does not necessarily translate into market power. It may be too soon to reach a decisive conclusion about whether market power, not simply market concentration, is on the rise.

Many sectors of the U.S. economy seem to be increasingly dominated by a handful of large and powerful players. The tech sector offers a number of well-known examples. The vast majority of smartphones run software developed by one of two companies — Apple or Google. For 98 percent of consumers, the talk and data services that power those phones come from one of four providers — Verizon, AT&T, T-Mobile, or Sprint. And virtually all of the web-based searching on phones and computers flows through one of Google's many platforms, to the point that "googling" has become synonymous with internet searching in general.1

Other industries are exhibiting signs of growing concentration as well. By one measure, concentration in the retail sector has increased by more than 400 percent since 1982, and concentration in finance has more than doubled since 1992.2 Some policymakers have argued that this growing concentration is a sign of weakening competition. A 2016 report from the Council of Economic Advisers (CEA) under former President Barack Obama highlighted this concern: "When there is little or no competition, consumers are made worse off if a firm uses its market power to raise prices, lower quality for consumers, or block entry by entrepreneurs."3

The CEA report and other studies point to signs of rising market concentration and falling entry rates for new firms as evidence that markets are becoming less competitive. But while firms with market power are indeed more likely to operate in concentrated markets, concentration by itself is not necessarily a sign of market power. Markets could become concentrated because the most efficient companies outperform their less-productive competitors, for example. Such an outcome presumably would make consumers better off, not worse. Indeed, many sectors of the economy follow a life cycle in which the number of competitors gradually shrinks over time. Mature industries consolidate around the most efficient firms, and this consolidation is not necessarily the result of anticompetitive behavior.4

Thus, a key question for policymakers is whether market power, not simply market concentration, is on the rise. Researchers have been hard at work attempting to answer this question. But, as this Economic Brief will show, it may be too soon to reach a decisive conclusion.

Why Market Power Matters to the Fed

The Federal Reserve is among the policy institutions keeping a close eye on competition. If firms' market power is rising, that could result in a number of changes for the economy that matter for monetary policy. Monopolistic firms would tend to charge higher prices above their costs of production and underproduce compared with those in competitive environments. The ratio of price to cost is known as the firm's "markup." A recent study found that "the welfare costs of markups are large," primarily because they act as a tax on output.5 Firms with more market power also may invest less, resulting in slower productivity growth.6 To the extent that this behavior is widespread across industries, it could lead to a general slowdown in productivity and, as a result, impair long-run economic growth.

It might be natural to infer that higher markups also would result in higher inflation, something that certainly would be a concern for the Fed. However, the relationship between markups and inflation is not entirely straightforward. Inflation is a measure of rising prices generally, but markups measure how much individual firms set prices above their costs. Thus, it is possible for markups to rise because firms facing little competition are able to set prices high or because efficient firms have found ways to reduce their costs while keeping prices stable. In the latter case, prices and inflation could remain flat. Inflation also measures the rate of change in prices across a period of time (typically year-over-year). As a result, even if markups were rising because firms with market power were raising prices, they would need to do so across time and across industries in order to have an impact on inflation. It also may be difficult to discern a connection between markups and inflation if the Fed is pursuing monetary policy that offsets inflationary pressure from markups.

Rising market power also has implications for maximizing employment, the other component of the Fed's dual mandate. Basic economics implies that businesses with market power withhold at least some production in order to keep prices high. Thus, if firms produce less due to a lack of competition, they also may hire fewer workers, which could raise unemployment or, in the long run, reduce workforce participation. And, to the extent that firms have the power to set wages in labor markets, they may be able to pay workers less.

The Fed tracks wage growth both as a sign of labor market health and as a signal of labor productivity. In a competitive environment, the largest portion of firms' productivity gains should be passed on to workers in the form of higher wages. Firms compete for labor, and the most productive firms will pay more for workers to expand production. But if firms face less competition for workers, they can reap the rewards of higher productivity as pure profits rather than passing them on in the form of wage increases. Thus, market competitiveness matters for how the Fed interprets changes in the rate of wage growth. Slow wage growth in a competitive market could be a sign of slowing productivity and economic growth, which might bolster the case for expansionary monetary policy. But slow wage growth in an increasingly monopolistic environment may not be a sign of slowing productivity because gains from productivity could be going to firm profits. In this case, the argument for expansionary monetary policy is weaker.

Higher market power also may reduce the effectiveness of the Fed's traditional monetary policy tool of influencing short-term interest rates. As noted earlier, firms with more market power may produce and invest less, depressing aggregate productivity growth. There is also some evidence that weak investment on the part of firms may depress the natural rate of interest in the economy. In a 2016 paper, Callum Jones of the International Monetary Fund and Thomas Philippon of New York University's Stern School of Business found that, given firm profitability, corporate investment in the United States has been lower than expected since the early 2000s. Had investment been more in line with expectations, they estimated that interest rates would have begun rising away from near-zero levels starting at the end of 2010 rather than in 2016, when rates actually did increase.7 To the extent that increased market power among industry leaders is contributing to lower investment and real interest rates, the Fed may encounter the zero lower bound more often.

Firms with more market power also may be less responsive to monetary policy stimulus. One way that the Fed stimulates the economy during a downturn is by reducing the cost of capital by pushing interest rates down. But if firms are less inclined to invest because of market power and they have the ability to capture higher profits through markups, they may absorb some of the interest rate changes in the form of profits rather than investing more.8 This result would tend to make traditional monetary policy less effective.

Clearly there are many reasons for the Fed to be concerned about a general increase in market power in the economy. But determining whether market power is actually going up is a challenge. Economists cannot directly measure changes in market power, but they can attempt to infer its presence by looking at other indicators, such as changes in industry concentration, markups, and firm profitability. Unfortunately for policymakers seeking clear guidance, the evidence in each of these cases has thus far been mixed.

Are Markets Becoming More Concentrated?

Increasing market concentration may be one of the most visible signs of rising market power. Firms with a large market share presumably face less competition than firms in markets with many players. Beyond the examples noted at the beginning of this Economic Brief, researchers have documented a general rise in concentration across industries. One striking finding comes from a paper by Gustavo Grullon of Rice University, Yelena Larkin of York University, and Roni Michaely of the Geneva Finance Research Institute. They found that concentration levels have increased in more than three-quarters of U.S. industries over the past two decades. Moreover, the market shares of the four largest firms in most industries have increased, and both the average and median size of public firms (which tend to be larger than private firms) have tripled.9

As noted at the outset of this Economic Brief, rising concentration alone does not necessarily mean that market power is going up. Firms with large market shares still may be subject to competitive pressures from new entrants, for example. But research showing that startup activity has fallen since 2000 suggests that firms may be facing less outside pressure today than in the past.10

Another way concentration could rise without a comparable increase in market power is if the most efficient firms are capturing greater market share by outcompeting their rivals. Such a scenario would be less troubling for consumer welfare than monopolistic firms abusing market share. To address this point, Grullon, Larkin, and Michaely looked at data on stock market reactions to mergers and acquisitions. If firms are more profitable in concentrated markets because they face less competition, the authors reasoned that "the market should react more positively to announcements of transactions that further erode product market competition." Indeed, they found that the market reaction to mergers was more positive when the merger involved firms in concentrated industries.

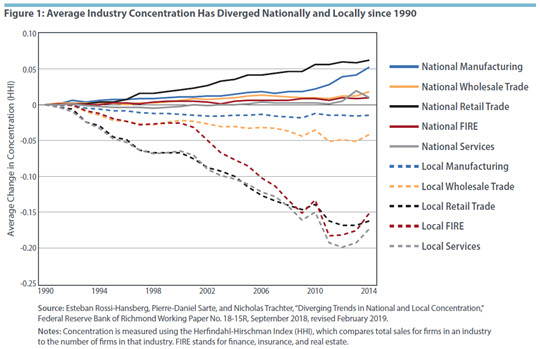

While these findings seem to suggest that the recent rise in concentration is a sign that market power has been going up, such conclusions depend crucially on how one defines the market. Evidence presented by Grullon, Larkin, and Michaely, as well as others, shows concentration has gone up in national industry groups. But in many industries, competition happens locally not nationally. For example, Walmart may account for a large share of national retail sales, but in any given market, it may compete with other national chains as well as locally owned stores.

One of the authors of this Economic Brief (Trachter) along with Esteban Rossi-Hansberg of Princeton University and Pierre-Daniel Sarte of the Richmond Fed highlighted this distinction in a recent paper.11 Using data from the U.S. National Establishment Time Series, they found that while national industry concentration rose on average from 1990 through 2014 across a variety of industry groups, local concentration in those same industries actually declined.12 (See Figure 1.) Moreover, these two trends appear to be strongly correlated: a large fraction of workers in the economy are employed by industries that had both rising national and falling local concentration.

It would appear that rather than forcing the exit of local competitors when they enter a market, national brands such as Walmart or Starbucks simply add to the competition. To the extent that local competition determines market power, the findings that national industry concentration has been increasing may not be cause for alarm.

Measuring Markups

Rising markups could be another sign that firms are gaining market power. In a competitive environment, markups should be low. If firms tried to substantially raise their prices above their costs, new companies would enter the market to undercut them, driving the markups down. Thus, some researchers have pointed to evidence of higher markups as proof that markets have become less competitive.

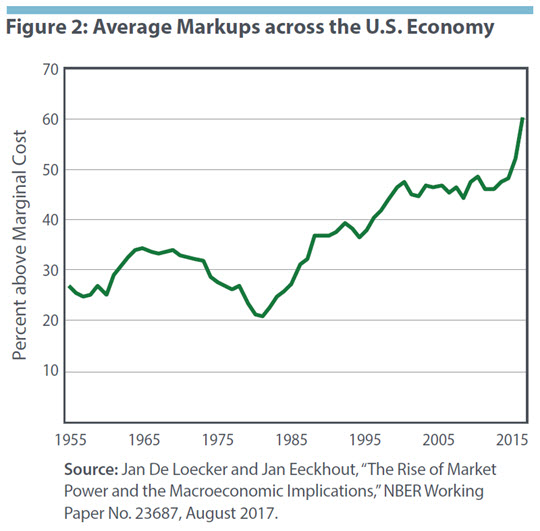

One of the leading studies in this area of research comes from Jan De Loecker of Katholieke Universiteit Leuven and Jan Eeckhout of the Barcelona Graduate School of Economics. In a 2017 paper, they found that markups increased substantially across all U.S. industries, from 21 percent in 1980 to 61 percent in 2016.13 (See Figure 2.) They found a similar increase in markups for firms globally in another paper, though the trend was strongest in North America and Europe.14 Tying these results to observations of rising market concentration, De Loecker and Eeckhout found that the increase in markups has been driven by the top firms by market share in each industry.

While this research has received a lot of attention, measuring markups across the entire economy and across time has historically proven difficult to do. It requires economists to model industry competition and to make assumptions about how firms behave in order to estimate their marginal costs, which typically are not publicly known. These constraints have tended to limit economists to studying markups only in specific sectors of the economy where good data were available. De Loecker and Eeckhout took a different approach in order to overcome these constraints, but their findings remain a source of ongoing debate among economists.

For example, decisions about how to measure firm costs can change the result of markup estimates. Other researchers found that including the costs that firms face in marketing and delivering their products and services to consumers may largely account for the increase in markups.15 These indirect costs have become a larger share of firms' variable costs since 1980, and it may be these rising costs rather than rising prices that De Loecker and Eeckhout measured.16

Given these measurement challenges, it is not yet clear whether estimates of rising markups necessarily point to rising market power. Researchers also have looked at whether firms in concentrated markets have more pricing power over their inputs of production, such as labor. If so, that might also suggest a rise in market power. Multiple studies do find that firms in concentrated sectors are able to pay lower wages.17 But, again, to the extent that firms compete for labor locally in the same way that they compete for customers locally, it is important to study the ties between local concentration and wages.

A 2018 paper by Kevin Rinz from the U.S. Census Bureau found that while firms in concentrated sectors are able to pay lower wages, local employer concentration actually has been falling since the 1970s (in line with the findings of Rossi-Hansberg, Sarte, and Trachter). This result would suggest that firms' pricing power in terms of labor is actually falling in the geographies that matter most for employees.18

Rising Profits, Falling Investment

Some economists have looked at a third potential signal of rising market power: rising profits for the largest firms. As in the case of markups, measuring profits is challenging because they are typically not directly observable. Instead, researchers have proposed novel ways of inferring them from the data available. For example, the London Business School's Simcha Barkai examined the share of production accruing to labor and capital costs, which are known, and reasoned that any remainder must be accruing to firms in the form of profits.19 He found that both the labor and capital shares have fallen over the past three decades, suggesting that the profit share has increased substantially over the same period.

But, as with markups, the difficulty of measuring firm profits has sparked disagreements among researchers. One study extended Barkai's methodology to the pre-1980 period and found that profits and productivity growth should have been much more volatile than what was actually observed over those decades if Barkai's assumptions were correct.20 Economists also disagree over what may be driving the fall in capital and labor shares. David Autor of the Massachusetts Institute of Technology and his coauthors found that large firms in concentrated industries have higher productivity growth per worker than other firms, and this greater efficiency results in these "superstar" firms spending a smaller share of their total sales on labor income.21

Another dispute is whether capital investments have truly shrunk or whether they are being mismeasured. Nicolas Crouzet and Janice Eberly of Northwestern University's Kellogg School of Management found that the rise of intangible assets since the 2000s can explain much of the capital investment shortfall.22 They found that intangible investments have been associated with productivity gains in some industries, such as the tech sector, suggesting that rising market concentration could be a symptom of greater efficiency and productivity.

On the other hand, intangibles also can be used by large firms to defend their market power from competitors. Research and development are often nonrival and excludable, which means other firms could benefit from that knowledge without diminishing the ability of the originating firm to use it, but legal restrictions such as patents and copyrights can make those assets exclusive to the owner. Such exclusivity promotes investment in intangibles, but it also may contribute to industry concentration by allowing firms to benefit from economies of scale and solidify their market power. Additionally, as firms face less competition, they may have fewer incentives to invest in both intangible and tangible capital.23 Ultimately, as in the case of markups, the evidence on profits and investment remains inconclusive and evolving.

An Unsettled Debate

As the preceding survey of the literature on this topic shows, there is evidence both for and against the rise of market power in the modern economy. In many cases, this conflicting evidence reflects different interpretations of phenomena that are inherently difficult to measure. Many economists agree that national industry concentration has been rising. But is this because the economy is increasingly driven by firms that rely on network effects and other economies of scale that naturally produce large winners? Or are large firms investing in assets protected by patents and copyrights to keep out competitors? Could both explanations be at play? Some of the apparent contradictions in evidence also may be explained by industry concentration trending up at the national level at the same time it is falling locally. This possibility raises another important question: Should policymakers be worried about higher national concentration when most markets for goods, services, and labor are local?

Unfortunately, the research does not yet provide decisive answers to these questions. It also could be the case that these trends are being driven by other factors unrelated to market competition. A recent study argues that the decline in new firm creation and the rise in market concentration can be explained by the aging U.S. population. The authors argue that as baby boomers age and retire, labor force growth is shrinking, leading to less startup activity. Existing firms age and grow, leaving even fewer workers to fuel startups and driving the rise in industry concentration.24 Another study based on a model found that industry-leading firms have stronger incentives to invest in a low interest rate environment than laggard firms. To the extent that this is the case, the low interest rates of the past decade could have contributed to rising concentration as leaders continued to invest and pull further away from smaller competitors.25

In summary, there is no shortage of explanations for the observed phenomena of rising market concentration and markups, and not all of those explanations point to a commensurate increase in market power. In his own review of the evidence, University of Chicago economist Chad Syverson summarized the debate this way: "The macro market power literature has offered an immense service by documenting and emphasizing the potential connections between several trends: labor's declining share of income, increasing corporate profits, increasing margins, increasing concentration, slower productivity growth, decreasing firm entry and dynamism, and reduced investment rates. … Where the literature, at this point at least, has not yet reached a conclusion is whether and to what extent increases in the average level of market power in the industry is responsible for each or all of these trends."26

Until that conclusion is reached, this topic will remain an important area of research in the years to come, and policymakers should weigh evidence carefully before deciding whether to respond to allegations of rising market power.

Tim Sablik is an economics writer and Nicholas Trachter is a senior economist in the Research Department at the Federal Reserve Bank of Richmond.

1

For other examples, see Open Markets Institute, "America's Concentration Crisis," https://concentrationcrisis.openmarketsinstitute.org/.

2

David Autor, David Dorn, Lawrence F. Katz, Christina Patterson, and John Van Reenen, "Concentrating on the Fall of the Labor Share," American Economic Review: Papers and Proceedings 2017, May 2017, vol. 107, no. 5, pp. 180–185.

3

Council of Economic Advisers, "Benefits of Competition and Indicators of Market Power," Issue Brief, April 2016.

4

Michael Gort and Steven Klepper, "Time Paths in the Diffusion of Product Innovations," Economic Journal, September 1982, vol. 92, no. 367, pp. 630–653.

5

Chris Edmond, Virgiliu Midrigan, and Daniel Yi Xu, "How Costly Are Markups?" NBER Working Paper No. 24800, July 2018.

6

It's also possible for this relationship to go in the opposite direction. Firms protected from competition may invest more knowing that they can reap all of the rewards of innovation themselves. This is the rationale behind patent protections in some fields, such as pharmaceuticals, where initial research and development is costly but replication is relatively cheap. Firms exposed to competition might choose to forgo costly research and instead free-ride on the efforts of other companies, resulting in fewer new drugs being developed. In theory, giving a firm temporary monopoly over a new drug provides an incentive to undertake costly research.

7

Callum Jones and Thomas Philippon, "The Secular Stagnation of Investment?" Manuscript, December 2016.

8

John Van Reenen, "Increasing Differences between Firms: Market Power and the Macro-Economy," Federal Reserve Bank of Kansas City Economic Policy Symposium Proceedings, Jackson Hole, Wyoming, August 24, 2018.

9

Gustavo Grullon, Yelena Larkin, and Roni Michaely, "Are U.S. Industries Becoming More Concentrated?" Review of Finance, forthcoming.

10

Ryan Decker, John Haltiwanger, Ron Jarmin, and Javier Miranda, "The Role of Entrepreneurship in U.S. Job Creation and Economic Dynamism," Journal of Economic Perspectives, Summer 2014, vol. 28, no. 3, pp. 3–24.

11

Esteban Rossi-Hansberg, Pierre-Daniel Sarte, and Nicholas Trachter, "Diverging Trends in National and Local Concentration," Federal Reserve Bank of Richmond Working Paper No. 18-15R, September 2018, revised February 2019.

12

National and local banking also exhibit this trend. See Lawrence J. White, "Antitrust and the Financial Sector," Money and Banking blog, January 21, 2019.

13

Jan De Loecker and Jan Eeckhout, "The Rise of Market Power and the Macroeconomic Implications," NBER Working Paper No. 23687, August 2017.

14

Jan De Loecker and Jan Eeckhout, "Global Market Power," NBER Working Paper No. 24768, June 2018.

15

James Traina, "Is Aggregate Market Power Increasing? Production Trends Using Financial Statements," University of Chicago Booth School of Business New Working Paper Series, No. 17, February 2018; Loukas Karabarbounis and Brent Neiman, "Accounting for Factorless Income," NBER Working Paper No. 24404, March 2018, revised June 2018.

16

De Loecker and Eeckhout addressed this concern in more recent work with Gabriel Unger of Harvard University. They acknowledged that while such overhead as a share of costs has gone up in recent decades, it still cannot fully explain the rise in markups they found. See Jan De Loecker, Jan Eeckhout, and Gabriel Unger, "The Rise of Market Power and the Macroeconomic Implications," Manuscript, November 22, 2018.

17

José Azar, Ioana Marinescu, and Marshall I. Steinbaum, "Labor Market Concentration," NBER Working Paper No. 24147, December 2017, revised February 2019; Efraim Benmelech, Nittai Bergman, and Hyunseob Kim, "Strong Employers and Weak Employees: How Does Employer Concentration Affect Wages?" NBER Working Paper No. 24307, February 2018.

18

Kevin Rinz, "Labor Market Concentration, Earnings Inequality, and Earnings Mobility," U.S. Census Bureau CARRA Working Paper No. 2018-10, September 24, 2018.

19

Simcha Barkai, "Declining Labor and Capital Shares," Manuscript, 2017.

20

Karabarbounis and Neiman (2018).

21

Autor et al. (2017).

22

Nicolas Crouzet and Janice Eberly, "Understanding Weak Capital Investment: The Role of Market Concentration and Intangibles," Federal Reserve Bank of Kansas City Economic Policy Symposium Proceedings, Jackson Hole, Wyoming, August 24, 2018.

23

Germán Gutiérrez and Thomas Philippon, "Investment-Less Growth: An Empirical Investigation," NBER Working Paper No. 22897, December 2016, revised January 2017.

24

Hugo Hopenhayn, Julian Neira, and Rish Singhania, "From Population Growth to Firm Demographics: Implications for Concentration, Entrepreneurship, and the Labor Share," NBER Working Paper No. 25382, December 2018.

25

Ernest Liu, Atif Mian, and Amir Sufi, "Low Interest Rates, Market Power, and Productivity Growth," NBER Working Paper No. 25505, January 2019.

26

Chad Syverson, "Macroeconomics and Market Power: Facts, Potential Explanations and Open Questions," Economic Studies at Brookings, January 23, 2019.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Market Structure and the Macroeconomy Workshop

The Federal Reserve Bank of Richmond held a workshop in May 2019 about market power and concentration. Watch the presentations on YouTube or view the agenda on our website.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us