Asset Bubbles and Global Imbalances

Economic Brief

January 2020, No. 20-01

What caused the housing boom and bust of the early 2000s? Capital inflows from emerging markets to developed economies can contribute to the formation of bubbles in asset prices. Those bubbles encourage the accumulation of debt, and the deleveraging of that debt exacerbates the decline in economic activity when the bubble bursts.

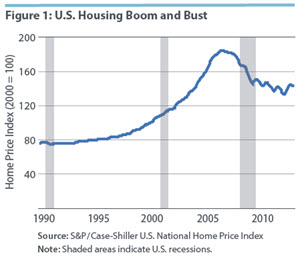

The dramatic decline in housing prices was a key component of the Great Recession. From January 2000 to July 2006, the S&P/Case-Shiller U.S. National Home Price Index grew by 85 percent before shedding 27 percent of its peak value by February 2012. (See Figure 1 below.) Economists have struggled to fully explain this boom and bust in terms of economic fundamentals, such as demographics, construction costs, or interest rates.1 As a result, many observers have described this run-up and decline in housing prices as a bubble.

The Global Saving Glut

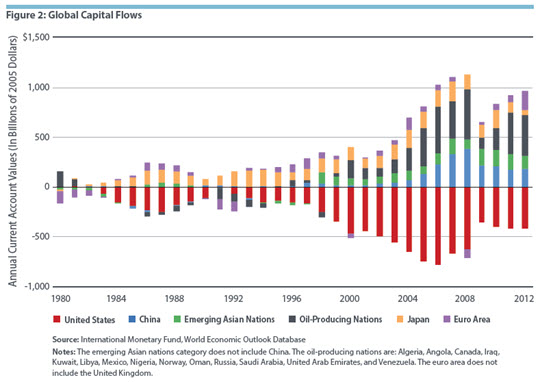

Since the 1980s, the United States has been a net importer of capital. Countries can finance investments through domestic savings or by importing capital from abroad. When they do the latter, they run a current account deficit. In a global economy, basic accounting arithmetic requires that if one country is running a current account deficit, others must be running offsetting surpluses. In other words, if the United States is borrowing from abroad, other countries must be lending. In recent decades, much of the capital flowing into the United States has come from emerging economies, such as China and oil-rich nations in the Middle East. That trend accelerated in the early 2000s leading up to the Great Recession. (See Figure 2 below.)

In 2005, former Fed Chair Ben Bernanke coined the phrase "global saving glut" to describe this flow of capital from emerging markets to the United States.2 Bernanke and other economists argued that this global saving glut might be contributing to low interest rates in the United States. Emerging economies are less financially developed than the United States.

As a result, savers in those countries have fewer options for investment, and those investments tend to pay lower returns than assets in developed economies. If countries are open to financial trade, savers in emerging economies would choose to invest in developed economies, exporting capital to those countries. Rising global demand for U.S. assets pushes up their prices and lowers their yields, resulting in lower interest rates in the United States.

Low interest rates help create the perfect environment for the formation of bubbles. Domestic investors in the United States, facing lower returns on traditional assets, may choose to speculate on riskier assets in search of higher returns. Such widespread speculation can fuel the emergence of bubbles.

Feedback Loops

Two of the authors of this Economic Brief (Ikeda and Phan) explore the relationship between global imbalances and bubbles in a recent article in the American Economic Journal: Macroeconomics.3 They model a setting with two open economies, which they call the North and the South. The North represents the United States, and the South represents emerging economies, such as China. The only difference between the two countries in the model is that the North is more financially developed than the South.

When the two economies are integrated through trade, Ikeda and Phan find two major effects. First, capital flows from the less financially developed South to the more financially developed North. Investors in the South are attracted to the higher rates in the North, which are a result of the greater financial sophistication of the North. But the influx of capital from the South lowers interest rates in the North. This fuels the development of bubbles in the North, Ikeda and Phan's second finding. Falling rates in the North make it more attractive for investors there to engage in speculation. The growth of bubbles, in turn, makes it even more attractive to invest in the North, inviting further capital flows from the South, which fuel more bubble growth. Thus, in the model, global imbalances in capital flows lead to the emergence of bubbles, and those bubbles further exacerbate global imbalances, which feed greater bubble growth.

In the past, some economists have argued that bubbles are unlikely to emerge in developed economies, such as the United States, because their financial markets are efficient.4 But Ikeda and Phan's model suggests that, even if a developed country, such as the North, has efficient financial markets, bubbles still can develop if the North is financially integrated with the inefficient markets of the South.

Conclusion

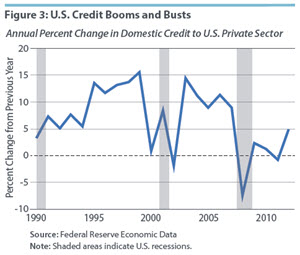

The model developed by Ikeda and Phan supports the "saving glut" hypothesis advanced by Bernanke. Interpreting the events of the early 2000s through the lens of the model, capital inflows from emerging economies, such as China, contributed to falling interest rates in the United States, which in turn helped fuel the emergence of a bubble in housing. The growth in housing wealth prompted U.S. businesses and consumers to take on additional debt. The eventual collapse of the bubble slowed these capital inflows and depressed economic activity in the United States, and that shock was exacerbated by the overextension of credit that accompanied the run-up in asset prices. This research illustrates how global imbalances in capital can contribute to financial instability in developed economies.

Daisuke Ikeda is a senior economist at the Bank of Japan. Toan Phan is a senior economist and Tim Sablik is an economics writer in the Research Department at the Federal Reserve Bank of Richmond.

1

Atif Mian and Amir Sufi, House of Debt: How They (and You) Caused the Great Recession, and How We Can Prevent It from Happening Again, University of Chicago Press, 2014. Robert J. Shiller, Irrational Exuberance, third edition, Princeton University Press, 2015.

2

See Ben S. Bernanke, "The Global Saving Glut and the U.S. Current Account Deficit," speech at the Sandridge Lecture, Virginia Association of Economists, Richmond, Virginia, March 10, 2005. Also, see Ben S. Bernanke, "Global Imbalances: Recent Developments and Prospects," speech at the Bundesbank Lecture, Berlin, Germany, September 11, 2007.

3

Daisuke Ikeda and Toan Phan, "Asset Bubbles and Global Imbalances," American Economic Journal: Macroeconomics, July 2019, vol. 11, no. 3, pp. 209–251.

4

Andrew B. Abel, N. Gregory Mankiw, Lawrence H. Summers, and Richard J. Zeckhauser, "Assessing Dynamic Efficiency: Theory and Evidence," Review of Economic Studies, 1989, vol. 56, no. 1, pp. 1–19.

5

Alejandro Justiniano, Giorgio E. Primiceri, and Andrea Tambalotti, "Household Leveraging and Deleveraging," Review of Economic Dynamics, January 2015, vol. 18, no. 1, pp. 3–20.

Views expressed in this article are those of the authors and not necessarily those of the Bank of Japan, the Federal Reserve Bank of Richmond, or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us