What Does the FOMC's Shift in Fed Funds Rate Target Language Mean?

Economic Brief

July 2021, No. 21-22

In September 2020, the Federal Open Market Committee shifted its language regarding maintaining the federal funds target range. The FOMC was now planning to maintain the rate until the economy not only was moving in the preferred direction, but had actually achieved its goals. Taken in isolation, this shift presents some risks, but additional language in FOMC statements makes clear that the committee will further shift its plans should conditions arise that compromise its goals.

After its September 2020 meeting, the Federal Open Market Committee (FOMC) released a statement noting that it expected to maintain its current target range for the federal funds rate "until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time." This was a notable departure from the previous FOMC meeting in July 2020, when the statement read, "The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals." The new language has been included in every FOMC meeting statement since September.

The shift in language represented a significant shift in the committee's thinking:

- In July, the committee had expected to keep the fed funds target at the effective lower bound until the economy was on track to achieve its goals.

- By September, the committee expected to maintain that level until the economy had reached those goals and then some.

This was a major shift not just relative to July, but also relative to the FOMC's historical behavior. In this Economic Brief, I contrast the policy described in the September FOMC statement to past Fed behavior and explain the rationale for the policy shift. I acknowledge risks that commentators have raised regarding the statement and explain how the statement as a whole guards against those risks.

Interpretation

The September 2020 FOMC meeting was the first one to occur after the Aug. 27 release of the FOMC's revised Statement on Longer-Run Goals and Monetary Policy Strategy ("Consensus Statement"). As discussed in detail in the Econ Focus article "The Fed's New Framework," the August update signified that the FOMC had revised its strategy regarding inflation: While the 2 percent inflation target remained, the committee moved from expressing concern if inflation were running persistently above or below target to aiming for inflation that averages 2 percent. This includes targeting inflation that is moderately above 2 percent for some time following periods when inflation has been running persistently below 2 percent.

Coming soon after the August update to the Consensus Statement, the September FOMC statement should be interpreted as adapting that modified strategy for the purposes of current policy. However, while the September FOMC statement is consistent with the Consensus Statement, it is by no means a necessary implication.

With inflation having been persistently below target in recent years, the Consensus Statement essentially obligated the Fed to aim for inflation moderately above 2 percent for some time. The FOMC decided at its September meeting that the best way to accomplish that goal was to keep the federal funds rate at its effective lower bound until both the inflation goal had nearly been reached and the FOMC's maximum employment goal had been reached.

Historical Context

Since the early 1990s, inflation in the U.S. has been low and stable: From January 1993 to April 2021, the three-year average PCE inflation rate has been between 0.7 percent and 3.2 percent, averaging 1.9 percent. In contrast, the corresponding range over the previous 28 years was 1.3 percent to 9.8 percent, with an average of 4.9 percent.

Over the more recent period, the FOMC has adjusted its short-term interest rate instruments in a very different manner with respect to the labor market than what is described in the FOMC statement as quoted above.

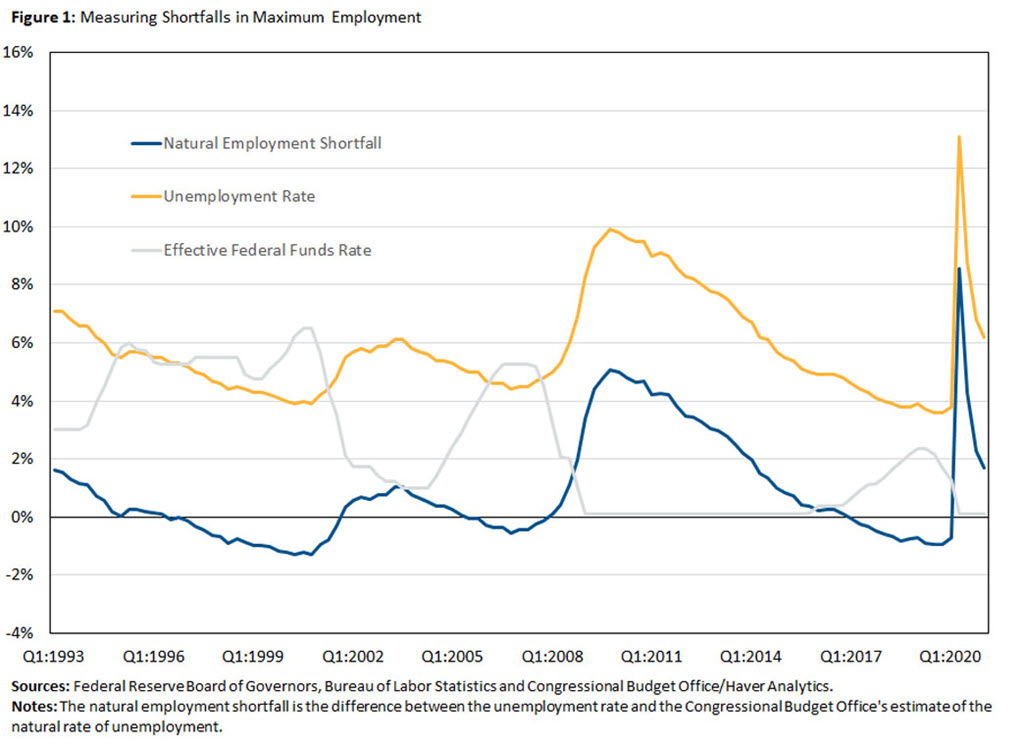

The message from the September statement is that the FOMC expects to refrain from raising interest rates until the economy is at maximum employment. There is no consensus measure of maximum employment, so Figure 1 displays the effective fed funds rate with two measures of the shortfall from maximum employment:

- The unemployment rate

- The difference between the unemployment rate and the Congressional Budget Office's estimate of the natural rate of unemployment

I interpret the unemployment rate as indicating a shortfall from maximum employment if its next turning point is a trough, and I interpret the difference between the unemployment rate and the natural rates as indicating a shortfall if it is greater than zero. That is, if the unemployment rate or unemployment gap is falling, I interpret the labor market as being short of maximum employment.

Since 1993, there have been four "tightening cycles," or episodes in which the FOMC has increased its fed funds rate target in a persistent manner. In each cycle, the labor market was short of maximum employment according to the unemployment trough criterion. In three of the four cycles, there was a shortfall according to the deviation-from-CBO-natural-rate criterion.

The one exception in the latter case was the tightening episode that began in July 1999: The gap between the unemployment rate and the natural rate turned negative in March 1997 and became increasingly negative, although the unemployment rate did not reach its trough until March 2000. However, the tightening cycle that started in July 1999 should perhaps be interpreted as the delayed continuation of a longer cycle that began in early 1994, as there was no recession during this period and the unemployment rate declined continuously apart from a period of stability from January 1995 to December 1996. There was a pause in that longer tightening cycle from September 1998 to July 1999, in the wake of the Russian debt default and the near-collapse of Long Term Capital Management.

Rationale for FOMC Strategy Shift

As shown above, the interest rate policy described in the September FOMC statement represents a major departure from FOMC behavior over the past 30 years. However, there is theoretical support for both the earlier policy and that which was adopted in September.

In a broad range of macroeconomic models, monetary policy can achieve a goal for inflation over the long run but has much less ability to control employment. Indeed, this perspective is conveyed in the FOMC's Consensus Statement, that while "The maximum level of employment … is not directly measurable and changes over time owing largely to nonmonetary factors that affect the structure and dynamics of the labor market…. The inflation rate over the longer run is primarily determined by monetary policy."

Furthermore, a large body of research (for example, a 1997 paper by Marvin Goodfriend and Robert G. King and a 1999 paper by King and myself) argues that it is not just feasible but optimal for monetary policy to aim for approximate price stability. To achieve price stability, the short-term nominal interest rate should mimic the behavior of the economy's underlying real rate of interest. This typically means that the real interest rate should move around with the strength of the real economy, arguably well-proxied by the unemployment rate or the gap between the unemployment rate and the natural rate.

In other words, this research provides theoretical support for the policy pursued by the FOMC from 1993 to 2020, when the fed funds rate target tended to move inversely with the unemployment rate, and inflation was low and stable. This policy is sometimes called pre-emptive, indicating that the interest rate moves up before inflation rises. But if one instead views inflation as stable (fluctuating only in a narrow band), it makes more sense to think of the policy rate as loosely tracking the economy's underlying real interest rate.

To understand the theoretical rationale for last September's change in policy, note first (as seen in Figure 1) that the unemployment rate was rising from January to November 2009 but the fed funds rate target was at its effective lower bound. Thus, the FOMC could not reduce interest rates as the economy weakened. Furthermore, inflation has been persistently below the FOMC's target for the last 10 years, albeit by a small amount.

In the early 2000s, a new body of research extended the theory of optimal monetary policy to situations in which the lower bound on nominal interest rates interferes with the basic approach outlined above. The standard approach to policy can lead to inflation being below target and real economic activity being undesirably low. Several papers showed that when monetary policy is constrained by the lower bound, it can be optimal to commit to keeping the short-term interest rate at that bound beyond the time when "conventional" policy would raise it. These papers include:

- The 2000 paper "Three Lessons for Monetary Policy in a Low-Inflation Era" by David Reifschneider and John C. Williams

- The 2003 paper "The Zero Bound on Interest Rates and Optimal Monetary Policy" by Gauti B. Eggertsson and Michael Woodford

- The 2012 working paper "Managing a Liquidity Trap: Monetary and Fiscal Policy" by Iván Werning

The September FOMC statement has this flavor: Whereas past FOMC behavior has involved raising the interest rate as the unemployment rate declined toward maximum employment, now the committee plans to hold rates at the lower bound until the economy has reached maximum employment.

What About Risks of the New Strategy?

Amid the recent high inflation numbers, some commentators have expressed concern about the Fed's plan to deviate from its previous approach. They worry that inflation could become unanchored. For example, see Martin Wolf's June 9 article in the Financial Times "The Fed Risks Being Too Slow on Inflation."

When commentary focuses on the FOMC's expectation that it will keep rates at their lower bound until its goals have been reached, it is not hard to understand why risks come to mind, for the figure shows what a significant change this represents. In previous episodes, the Fed would raise interest rates as the unemployment rate fell. Once the Fed's employment goals were reached, it was generally far along in that tightening process and would soon reduce interest rates as the economy began to weaken for one reason or another.

For example, the unemployment rate reached its cyclical low of 3.8 percent in March 2000, and the FOMC began lowering interest rates in January 2001 as the unemployment rate rose following the dot-com crash. Likewise, unemployment reached its cyclical low of 4.4 percent in October 2006, and the FOMC began lowering interest rates in September 2007.

However, commentary that highlights the risks of inflation becoming unanchored ignores an important element of the FOMC statement. The last paragraph of the statement includes the following passage: "The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals."

Unanchoring of inflation would clearly impede the attainment of the committee's goals. If the committee perceives that inflation would become unanchored if it keeps rates at zero until maximum employment, then presumably it will change its plan. Such a change would not mean the committee was forsaking its new Consensus Statement. Rather, it would mean that the committee felt that the plan outlined in September was no longer the best way to operationalize the Consensus Statement under prevailing economic conditions.

Alexander L. Wolman is a vice president in the Research Department of the Federal Reserve Bank of Richmond.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us