Are Some Homebuyers Strategically Transferring Climate Risks to Lenders?

Economic Brief

April 2022, No. 22-14

Recent empirical research suggests that certain homebuyers may be strategically transferring climate risks to banks via the mortgage market, and banks may be transferring such risks to government-sponsored enterprises via securitization. The evidence highlights the nuanced ways in which participants in the financial markets strategically adapt to climate change.

As the issue of climate change becomes increasingly salient, there has been increased attention to the need for economies to adapt. A large and growing economic research literature documents that physical adaptation strategies — ranging from adopting more drought-resilient crops to equipping buildings with air conditioning and upgrading urban infrastructure to be more resilient to floods and hurricanes — are expected to help protect households, firms and communities from intensifying climate-related disaster risks.1

However, we know less about financial adaptation, or how participants in financial markets adapt to climate change and whether their actions have implications for society at large. And generally, much less is known about how climate risks affect debt markets (including the mortgage market) despite the critical role these markets play in the financial system.2

Financially Adapting to Climate Risks

In my recent working paper "Leveraging the Disagreement on Climate Change: Theory and Evidence" — co-authored with Laura Bakkensen from the University of Arizona and Russell Wong from the Richmond Fed — I found some fascinating patterns of a certain financial adaptation strategy taken by some participants in the U.S. coastal residential property and mortgage market.

We leverage an extensive proprietary database by Corelogic to examine the complete history of single-family home sales across the U.S. East Coast from 2001 to 2016, including property and sales characteristics and the associated mortgage contracts (if used). Using the property's precise location, we match each property with its projected exposure to coastal inundation risk under various sea level rise (SLR) scenarios, using a high-resolution mapping tool developed by the National Oceanic and Atmospheric Administration.

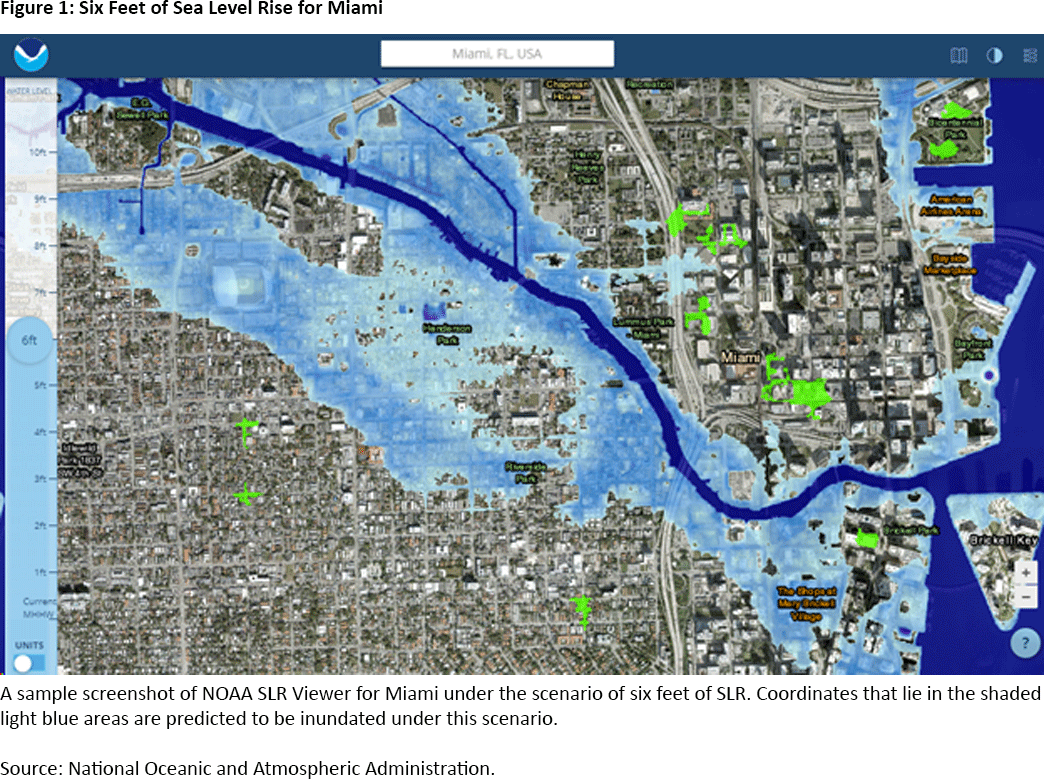

Figure 1 provides an example of the high-resolution spatial variation of exposure to inundation risk under the scenario of six feet of SLR for Miami. We focus on SLR risk as it is one of the most important and salient physical risks associated with climate change.3

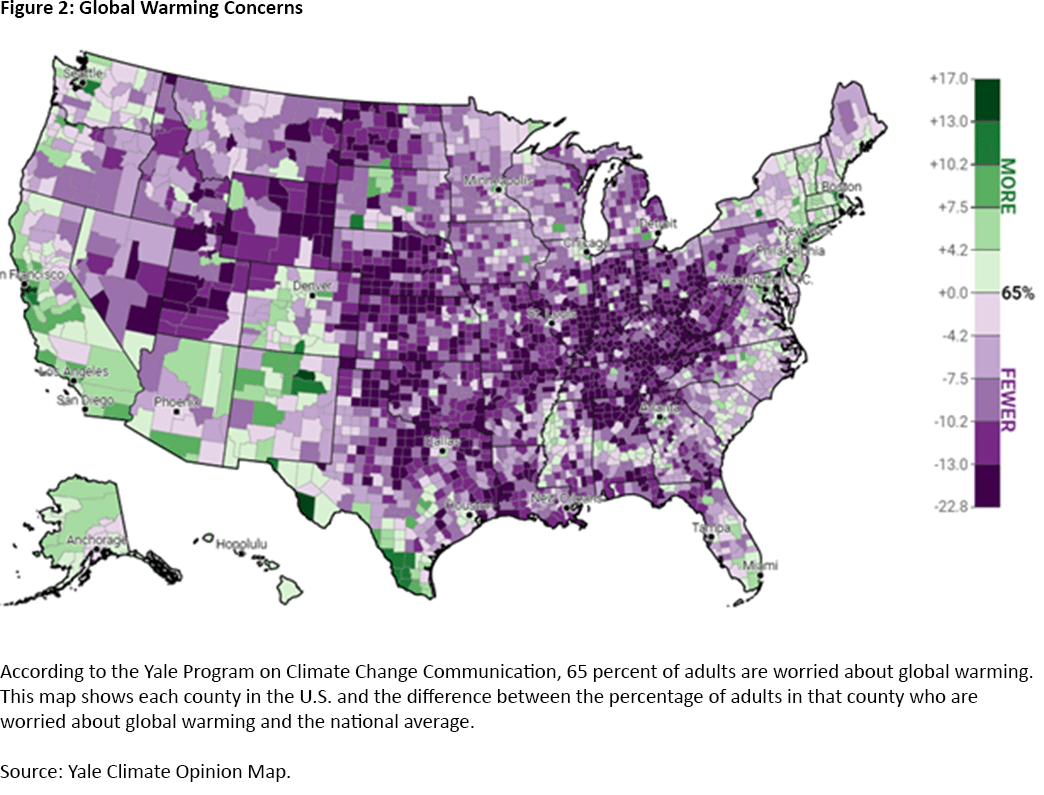

One important characteristic of climate change is that there is significant heterogeneity in people's beliefs about it. Figure 2 illustrates this belief heterogeneity, averaged across U.S. counties and using data from a well-known survey conducted by Yale University's Climate Communication program. We incorporate this Yale climate opinion survey data into our analysis.4

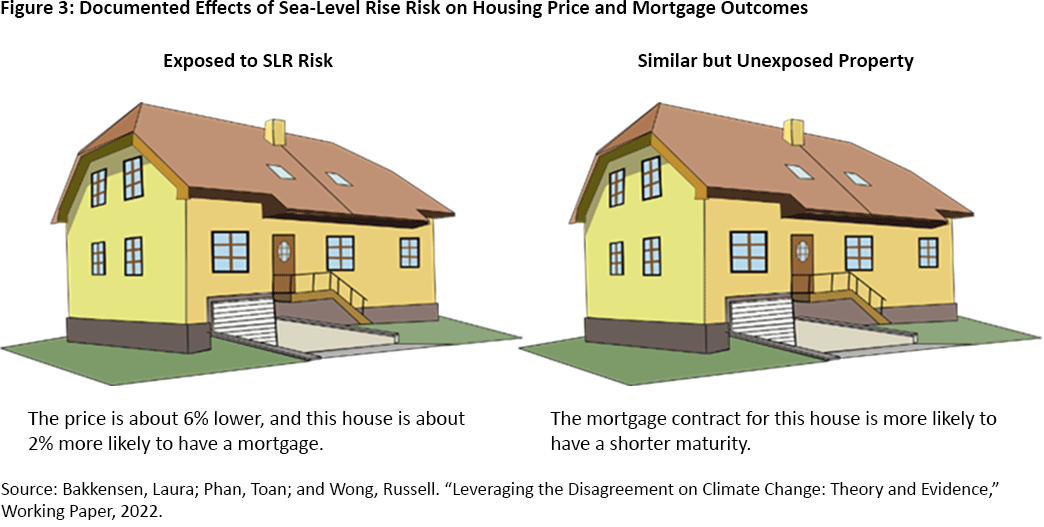

To identify the effects of SLR on real estate and mortgage outcomes using our data of nearly a million coastal property transactions, we compare the purchases of properties that are exposed to SLR risk to those of unexposed properties but are otherwise very similar (same ZIP code, same number of bedrooms, same transaction month/year, similar elevation and similar distance to coast). Our results are summarized in Figure 3 below.

We find robust evidence that purchases of homes more exposed to SLR risk are more likely to be leveraged and tend to use mortgage contracts with longer maturity (and hence more exposed to future climate risks), despite lower property prices. These results are driven by buyers from counties with more pessimistic climate beliefs, who are more likely to be aware of and concerned about SLR risk.

These findings suggest that buyers with more pessimistic climate beliefs (buyers from more pessimistic counties) could be strategically transferring climate risks to banks by taking long-term leveraged investment on properties exposed to future SLR. In fact, the findings are entirely consistent with a theoretical model of real estate transaction where homebuyers have varying degrees of beliefs about a property's long-run risk, and they choose whether to leverage with a defaultable mortgage debt contract and choose the contract's maturity.

Modeling Mortgage Risk and Climate Risk

We develop such a model in our paper. The model predicts that buyers with sufficiently pessimistic beliefs relative to bank lenders are more likely to trade their exposure to climate risk via long-term defaultable debt contracts.

Our model also predicts that expansionary monetary policies — which tend to increase the supply of bank credit — could induce more leverage by pessimists and hence make the mortgage market more vulnerable to climate change. This prediction is also supported by our data: We find that pessimists are more likely to leverage on properties exposed to SLR risk especially in times when the nominal interest rate is low.

Our findings on the shifting of climate risks via the mortgage market resonate with those in the 2021 paper "Mortgage Finance and Climate Change: Securitization Dynamics in the Aftermath of Natural Disasters." That paper finds evidence that banks can shift climate risks to government-sponsored enterprises (GSEs) through securitization and sale of mortgages below the conforming loan limit. This mechanism is potentially relevant and complementary to our story.

Suppose banks can securitize and sell conforming mortgage contracts to GSEs, whose rules and fees tend to reflect only current official flood-plain maps and do not necessarily reflect future climate risks. We may expect that the effects of SLR exposure interacted with the climate belief of buyers on leverage and maturity outcomes to strengthen in the segment of conforming loans.

In contrast, suppose banks cannot as easily sell nonconforming mortgage contracts and are thus more likely to hold them on their balance sheets. We may expect the effects of SLR exposure and climate belief to weaken in the segment of nonconforming loans. This is exactly what we find in our data: Our leverage and maturity results are almost entirely driven by conforming loans as opposed to nonconforming loans.

Conclusion

To conclude, we think that there are two characteristics that make climate risks special:

- They could have potentially large damages, especially to durable assets such as real estate.

- There is substantial disagreement over future climate risks, especially in the U.S.

Our paper finds that the combination of these two features is key in understanding the effects of climate risks on the financial system. Our analysis implies that adaptation strategies in financial markets — which are known to be subject to agency problems — may have nontrivial implications, specifically due to the strategic transfers of climate risks. Whether this could lead to concentration of climate risks and whether it could affect financial stability or general welfare remain open questions for future research.

Toan Phan is a senior economist in the Research Department at the Federal Reserve Bank of Richmond.

1

See for example the research literature survey in the 2021 book "Adapting to Climate Change."

2

Also see two of my articles from last year — "Climate Change and Financial Stability? Recalling Lessons from the Great Recession" and "Pricing and Mispricing of Climate Risks in U.S. Financial Markets" — on this topic of climate risks in the financial markets.

3

For example, as highlighted in the 2018 U.S. National Climate Assessment, more than 40 percent of Americans live in coastal shoreline counties, which are subject to SLR risk.

4

We use the 2014 vintage of the survey, as it overlaps with the sample period of our real estate data.

To cite this Economic Brief, please use the following format: Phan, Toan. (April 2022) "Are Some Homebuyers Strategically Transferring Climate Risks to Lenders?" Federal Reserve Bank of Richmond Economic Brief, No. 22-14.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us