Anticipated FOMC Policy, Inflation and Credibility

Economic Brief

September 2022, No. 22-37

Following through on its September 2020 plan, the FOMC waited to raise interest rates until March 2022, when inflation was high and unemployment was below its perceived long-run level. However, by early fall 2021, markets were predicting a rate increase, and policymakers were signaling an increase in their Summary of Economic Projections. In contrast to the 1980s and 1990s, when the Fed fought inflation scares even as actual inflation trended down, long-term inflation expectations have been relatively stable even as actual inflation has risen far above target. This stability has likely been facilitated by the SEP reinforcing the Fed's commitment to its 2 percent inflation target.

The Federal Open Market Committee began raising short-term interest rates in March. By then, unemployment had returned to its pre-COVID levels, and PCE inflation had been well above 2 percent for almost a year.

In retrospect, the FOMC stuck to its plan (announced in September 2020) of waiting to raise interest rates "until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time." It did not invoke the "escape clause" which stated that "The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals."

As I discussed in a previous article examining the FOMC's shift in fed funds rate target language, this plan represented a significant departure from the typical policy that the Fed had followed in the stable-inflation period from 1995 to 2019. However, although the FOMC did not raise short-term rates until this past March, markets began to anticipate an increase in rates well in advance, around the same time that the FOMC's own Summary of Economic Projections (SEP) began to reflect anticipated future rate increases.

In this article, I first provide measures of the market's expectations and FOMC participants' projections for the timing of future rate increases. I then show how FOMC participants' projections evolved together with their expectations for future inflation. Finally, I relate FOMC policy to the relative stability of long-term inflation expectations.

The Market's Expectations for Future Policy

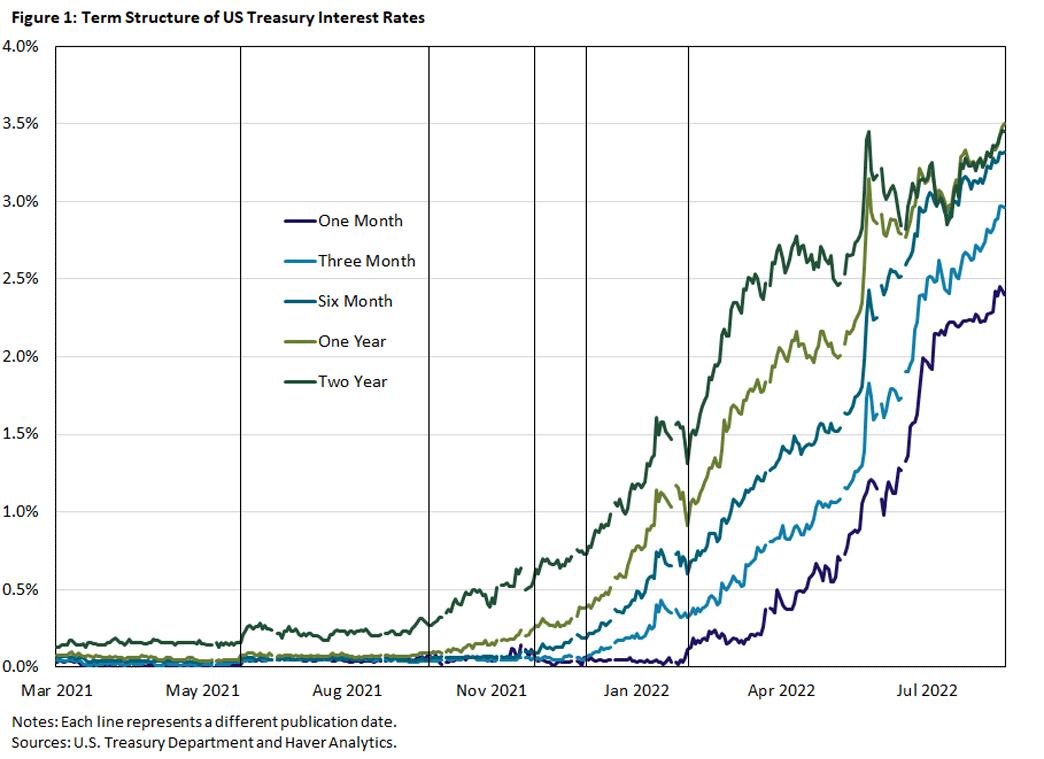

Figure 1 displays daily interest rates on U.S. Treasury securities at maturities of one month, three months, six months, one year and two years for the period from March 2021 to August 2022. If we interpret the term structure of interest rates as determined by the pure expectations hypothesis — a simplifying assumption which is not innocuous but nonetheless a useful first pass — then current yields on these securities reflect only market participants' expectations of future yields. In that case, Figure 1 provides information about the evolution of the market's expectations for liftoff and the path of future short rates more generally. The vertical lines indicate the approximate dates at which each interest rate first rose above the range at which it had settled in 2020:

- For the two-year rate, this was June 2021.

- For the one-year rate, it was September 2021.

- For the six-month, three-month and one-month rates, it was December 2021, January 2022 and March 2022, respectively.

Although the FOMC first raised its fed funds rate target in March 2022, markets began to see liftoff on the horizon in the summer of 2021. From then on, markets gradually pulled forward the date of expected liftoff, and by January 2022 markets were accurately forecasting when liftoff would occur.

While the monetary policy instrument is a short-term interest rate, for the relatively short maturities displayed in Figure 1, the expected path of that policy instrument is an important determinant of longer-term rates. As such, a lesson from Figure 1 is that monetary policy implicitly began to tighten in the summer of 2021, although markets revised up their expectations of the speed of "actual" tightening well into the spring of 2022.

FOMC Participants' Projected Policy

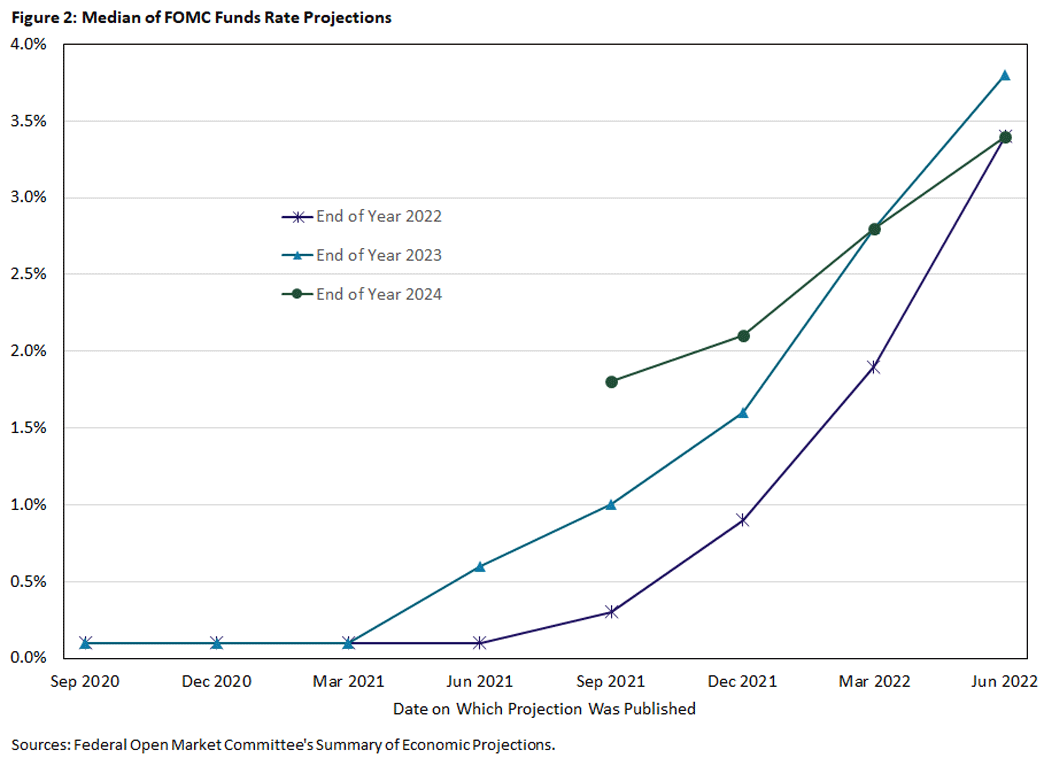

Whereas Figure 1 provides rough information about markets' expectations of the path of policy rates, Figure 2 provides direct information about what FOMC participants themselves projected as the appropriate path for future policy.

The figure plots data from each of the FOMC's eight SEPs from September 2020 to June 2022. For each projection date, the figure displays the median participant's fed funds rate projection for end-of-year 2022 (blue line), 2023 (purple line) and 2024 (green line). Note that the SEP typically contains projections two years out, so not all years are available for all projection dates.

Reassuringly, policymakers' projections in Figure 2 tell a similar story to market expectations in Figure 1: Starting in June 2021, the median projection showed rates beginning to increase sometime in 2023. And each subsequent meeting saw a higher median projection for the year-end funds rate. Thus, if we use a broad notion of policy that encompasses policymakers' intentions for the near-term path of the policy rate, policy began tightening in the summer of 2021, with further tightening at each subsequent meeting to June 2022.

Note however that the projected rate path implied by the median projection flattened then inverted in March and June of 2022. That is, the median projection in June 2022 showed a higher funds rate at end of 2023 than at end of 2024. For the most part, the same qualitative features appear as in Figure 1, under our assumption that Figure 1 mainly reflects market expectations.

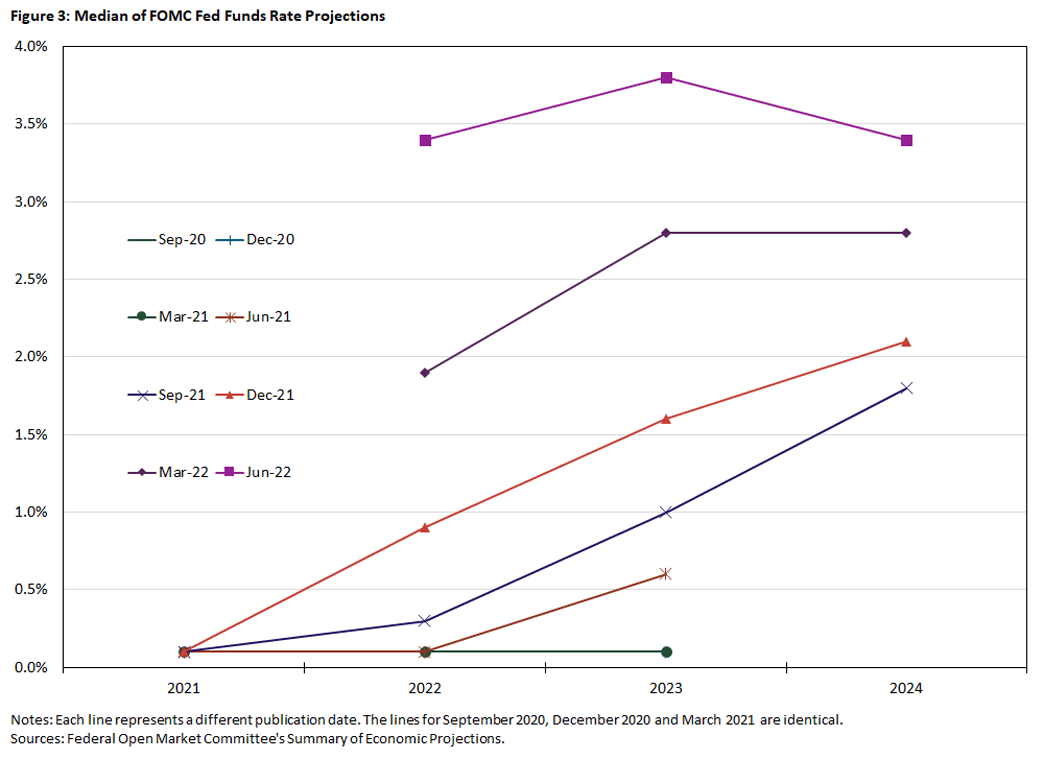

Figure 3 provides a different perspective on the same SEP data as Figure 2: The x-axis is now the year being forecasted, and the lines represent different dates of publication. I note three dates in particular:

- September 2020, when the median funds rate projection was flat over the forecast horizon

- December 2021, when the median projection showed a steady increase

- June 2022 (the most recent SEP), which shows a steep increase in 2022 (much of which has already occurred), a small further increase in 2023 and a reduction in the funds rate target in 2024

Policy Projections and Expected Inflation

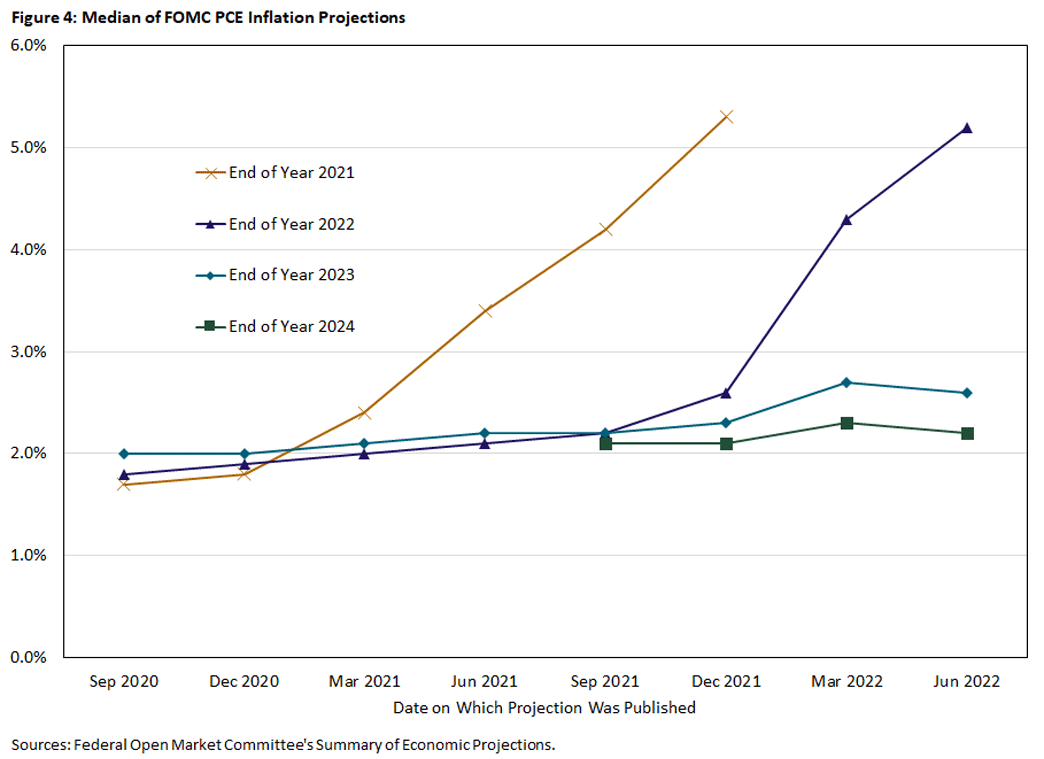

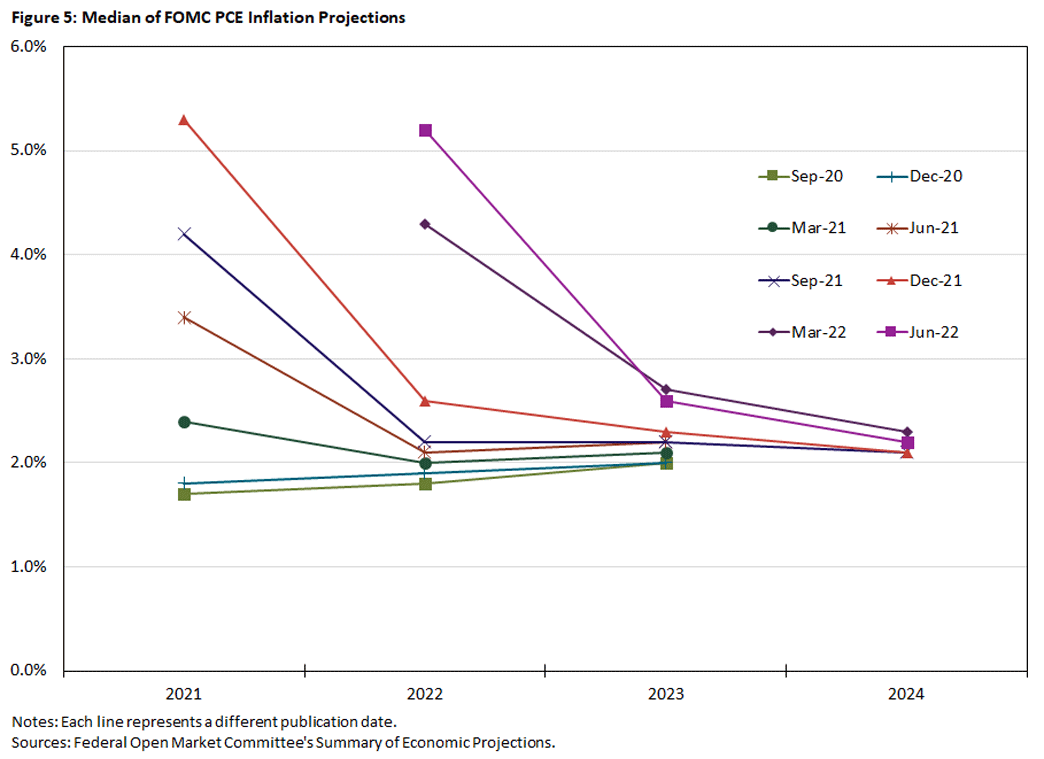

Figures 1-3 focus on interest rates and interest rate projections in isolation. But the FOMC's interest rate policy depends on its perceptions about the economy, and the behavior of inflation took center stage during this period. Figure 4 is the inflation analogue to Figure 2: The x-axis is the date of the projection, and each line represents a different year. The figure shows a large increase in the projected 2021 inflation rate over the course of 2021 and a large increase in the projected 2022 inflation rate over the first half of 2022.

Figure 5 displays the same data arranged by date of projection instead of by year. As inflation rose in 2021, the median projection showed a rapid decrease in inflation, though from the December 2021 SEP to the March 2022 SEP, the date of that decrease in inflation was pushed out from 2022 to 2023. With the most recent projection from June, the decrease in inflation anticipated to occur next year is almost identical to the decrease that was projected to occur this year when the December 2021 SEP was published.

Looking at the fed funds and inflation projections together, different interpretations are possible. A pessimist might say that the FOMC's response to inflation has not been strong enough: Actual inflation was above 5 percent in 2021, and projected inflation is above 5 percent for 2022, yet the funds rate is projected to be less than 3.5 percent at the end of 2022. One popular prescription for monetary policy — the Taylor principle — states that the interest rate target should move more than one-for-one with inflation, which is not the case for those projections.

On the other hand, the longer-run properties of the projection look quite different: Inflation is projected to be less than 3 percent in 2023 and 2024, with a funds rate above 3.5 percent. Thus, relative to pre-COVID conditions, the policy rate is ultimately projected to move more than one-for-one with inflation.

The Dog That Hasn't Barked: High Inflation but No Inflation Scare

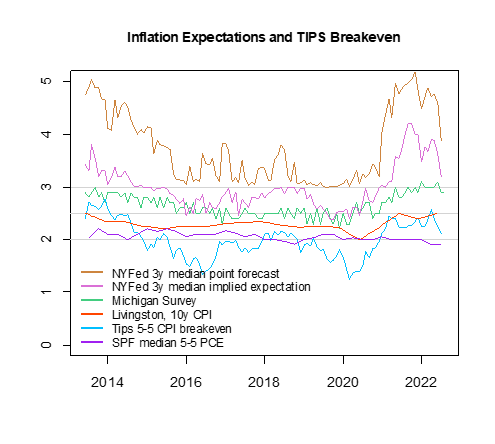

While one can give diverse interpretations to the evolution of the FOMC's median SEP projections for inflation and policy, markets and survey respondents seem to have weighed in on the optimistic side: They do expect FOMC policy to be consistent with low inflation over the long run. Figure 6 displays several survey measures of medium-run and long-run expected inflation, as well the forward breakeven inflation rate from the TIPS market.

Most of the series increased markedly in 2021, but they generally remained in their post-2013 ranges and have come down to well within those ranges in recent months. One exception is the Philadelphia Fed's Livingston survey for 10-year CPI expectation: At 2.5 percent, it's as high as it's been since 2013. However, this measure was also at 2.5 percent from December 2001 through 2008, not a period of significant inflation concerns.

The relative stability of long-term inflation expectations is almost certainly related to the Fed's stated 2 percent inflation target: The SEP has repeatedly reinforced every FOMC member's intention to achieve that target over the long run and to make substantial progress toward it over the next two years. Thought it's not pictured in Figures 4 and 5, FOMC participants' projections also include a long-run value for the inflation rate, and all FOMC participants' long-run projections for PCE inflation are 2 percent in every SEP. Anything else would be inconsistent with the FOMC's longer-run goals and monetary policy statement (PDF) that "The inflation rate over the longer run is primarily determined by monetary policy."

An Unusual Situation, or Is It?

This is an unusual situation for the U.S. economy. On one hand, actual inflation has been far above what the FOMC would have wanted — and what it predicted — for a year and a half. Many commentators described the Fed as being behind the curve on responding to high inflation.

On the other hand, there has been nothing that could be called an inflation scare, either in long-term nominal bond rates or the expectations measures in Figure 6. This is the opposite of the kind of situation the Fed encountered when it was establishing credibility for low inflation in the 1980s and 1990s. In that period, actual inflation was generally on a downward trend and stabilized around 2 percent starting in 1993. But it took several more years before long-term expectations also stabilized, and there were occasional spikes in bond rates that signaled doubts about the Fed's long-run credibility for low inflation.

While the current situation is unusual from the perspective of recent history, it fits easily into a standard modeling approach used by applied monetary economists. That approach maintains an assumption of perfect credibility for monetary policy and studies the behavior of the economy when there are fluctuations around a fixed inflation target. Depending on the nature of the shocks hitting the economy (which include shocks caused by monetary policy), there can be arbitrarily large and persistent deviations of inflation from target while long-term credibility is maintained.

One might respond that the Taylor principle is a requirement for macroeconomic stability in many of those models. However, it is not even clear that the short-run relationship described above violates the Taylor principle. If the low interest rates in 2021 represented temporary shocks rather than a fundamental shift in the Fed's implicit interest rate rule, then policy could have still been consistent with the Taylor principle.

Conclusion

In September 2020, the FOMC announced that it would likely wait to raise interest rates from the effective lower bound until inflation was at or above 2 percent and the economy had returned to a situation of maximum employment. Actual policy did follow this plan, and inflation has been very high by the standards of recent decades since the spring of 2021.

This article has shown that "effective" policy tightening began well before the actual funds rate liftoff in March 2022, where effective tightening refers to financial market expectations of policy over the next two years. In turn, market expectations reflected policymakers' own intentions, as measured by the FOMC's SEP. We related the FOMC's evolving interest rate projections to its evolving inflation projections. As actual inflation continued to surprise on the upside, in 2022 the FOMC has thus far raised its funds rate target well above what it had been projecting in 2021: According to Figure 3, in the 15 months from March 2021 to June 2022, the FOMC median interest rate projections have shifted up by approximately 350 basis points.

One can argue about whether the FOMC's response to inflation has been strong enough, but financial markets and surveys suggest that the Fed retains credibility for low inflation in the long run. We attribute this credibility in large part to the Fed's 2 percent inflation target and the fact that each quarterly SEP reinforces FOMC participants' intentions to return inflation to target.

The current situation is unusual in light of recent history but fits well into standard modeling frameworks with full credibility, where long-run stability of inflation can be consistent with large and persistent deviations of inflation from target. In reality, unlike in models, long-run credibility cannot simply be assumed. Thus far, the Fed's actions seem to have been consistent with maintaining credibility.

Alexander L. Wolman is a vice president in the Research Department of the Federal Reserve Bank of Richmond.

To cite this Economic Brief, please use the following format: Wolman, Alexander L. (September 2022) "Anticipated FOMC Policy, Inflation and Credibility." Federal Reserve Bank of Richmond Economic Brief, No. 22-37.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us