A Rate Cycle Unlike Any Other

Economic Brief

August 2023, No. 23-26

Since the Federal Open Market Committee began raising the federal funds rate in March 2022, people have speculated on the trajectory of both monetary policy and the economy. By looking at previous rate cycles, this article compares historical monetary policy cycles with the current period. We find the current cycle to be unique in terms of both the speed at which interest rates rose and the movement of inflation during the series of rate hikes.

As of this writing, the Federal Open Market Committee (FOMC) is 16 months into the current rate cycle, having raised the federal funds effective rate by 500 basis points since March 2022. This is the fastest increase in the federal funds rate since the FOMC began targeting it in 1982. This article asks where policy and the economy are likely to head from their current state and reviews previous rate cycles over the post-World War II period in the context of the current situation.

What Is a Rate Cycle?

In this article, we define rate cycles as the time between troughs in the federal funds effective rate. In other words, a rate cycle begins when the FOMC begins to raise rates and ends when the FOMC stops lowering rates. It is important to analyze both the rise and fall of rates to get a better picture of the Fed's actions and motivations.

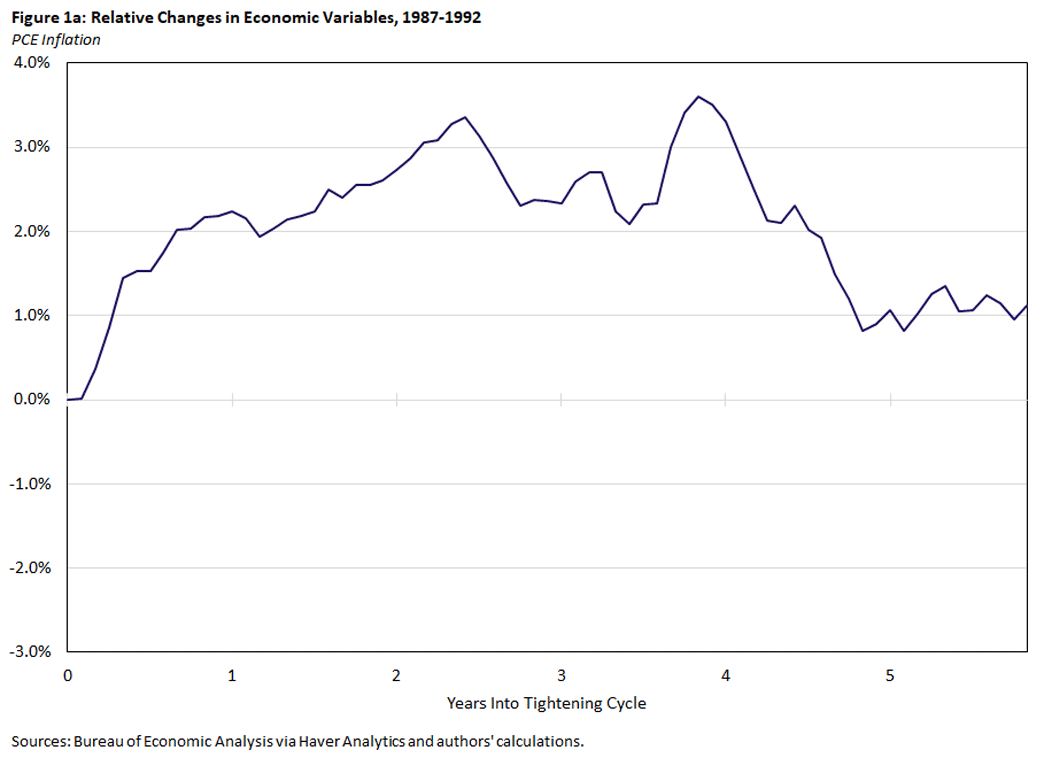

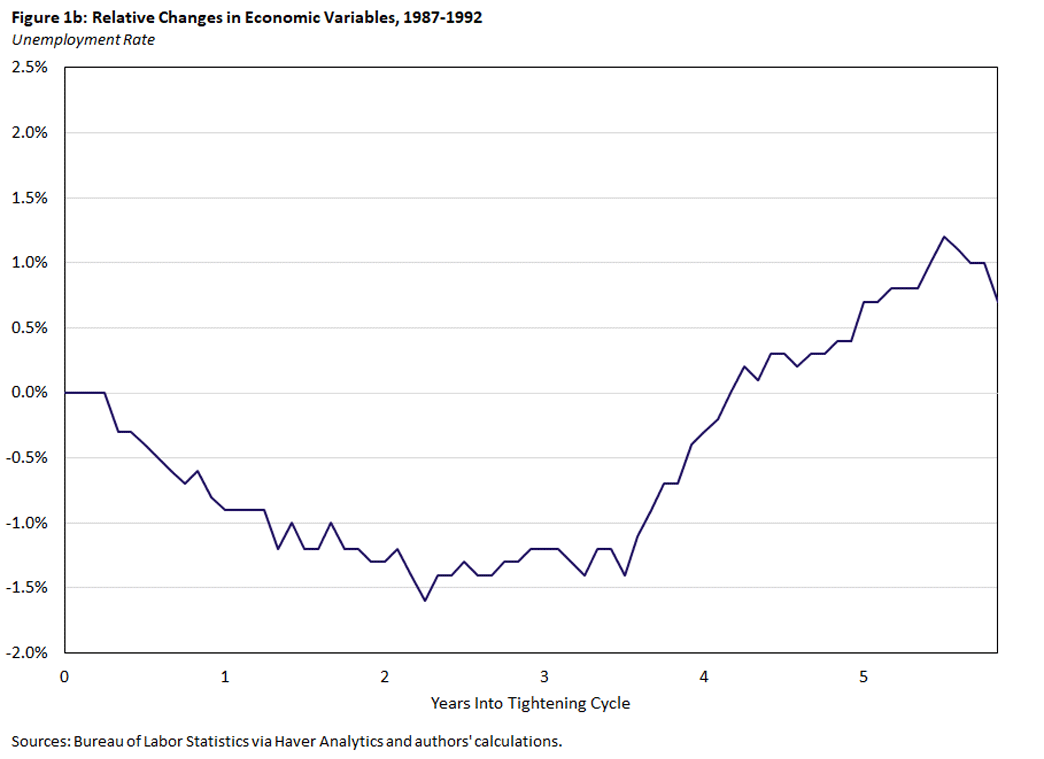

Rate Cycle: 1987-1992

High GDP growth in 1986 paired with a devaluing of the dollar in foreign exchange markets led to concern over inflation at the start of this rate cycle. In its first meeting in 1987, the FOMC (newly chaired by Alan Greenspan) began raising short-term interest rates. Over about two years, the federal funds effective rate rose from 5.9 percent to 9.8 percent. Ex-post data, though, indicates that the Fed had reacted perhaps too slowly, as PCE inflation rose from 1.6 percent to 4.7 percent over the same period.

However, the interest rate was not held high for more than a few months. With the inflationary environment as a backdrop, the FOMC began to gradually lower rates due to a stagnant unemployment rate and financial stresses originating from a savings and loan crisis where 32 percent of these institutions failed between 1986 and 1995. As the economy entered a recession in 1990 (coinciding with the first Gulf War and the attendant oil price shock), unemployment spiked, and the FOMC accelerated its rate cuts. When interest rates bottomed out in late 1992, the federal funds effective rate sat near 3.0 percent. The rise in the unemployment rate to 7.3 percent was associated with a fall in the PCE inflation rate to 2.7 percent.

In Figure 1, we chart PCE inflation and the unemployment rate over the rate cycle, with both normalized to zero at the start date. We can see that inflation continued to rise despite rate increases and only fell after the early 1990s recession and a spike in unemployment.

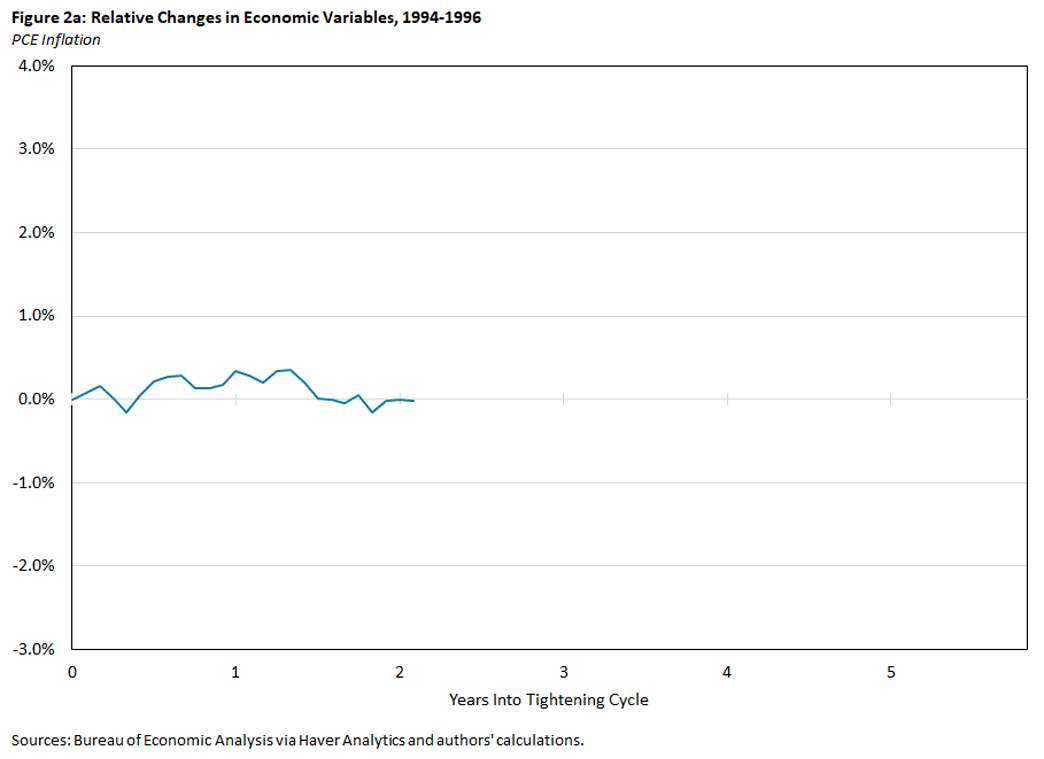

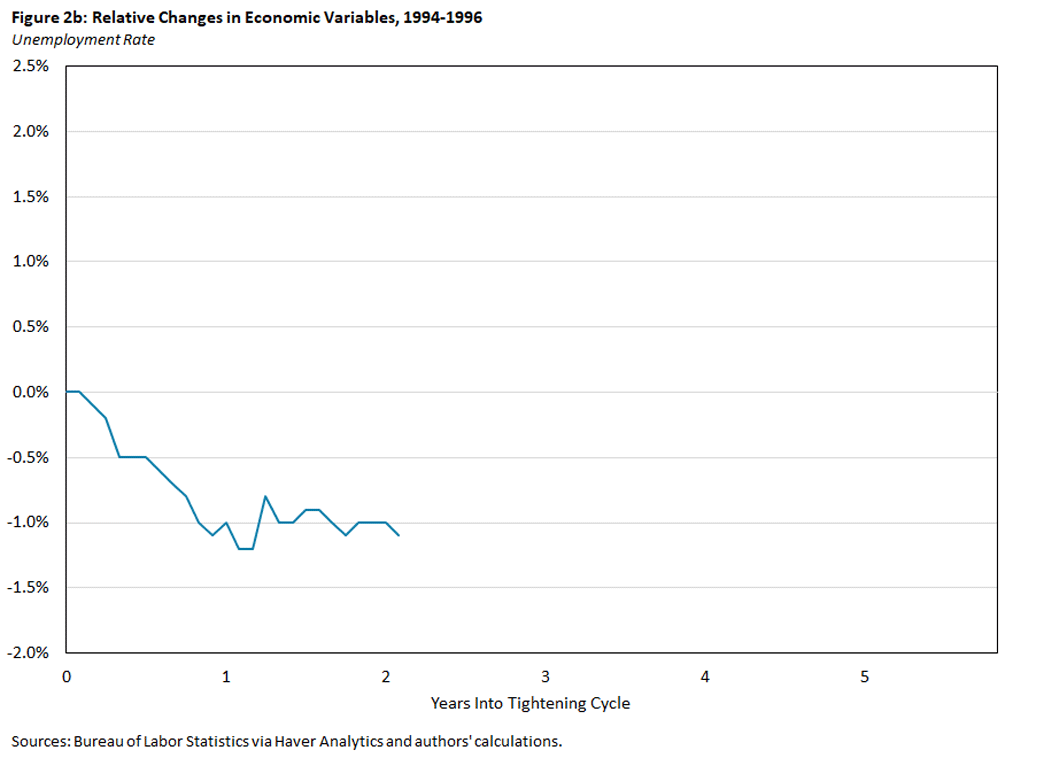

Rate Cycle: 1994-1996

Less than two years later, the FOMC once again began raising the federal funds rate target. By early 1994, the economy had been expanding for almost three years, averaging 3.5 percent GDP growth. To sustain this economic expansion while keeping inflation in check, the FOMC raised the federal funds effective rate from 3.0 percent to 6.0 percent over the course of a little more than a year. During this same period, PCE inflation measured between 2.0 percent and 2.3 percent, and the unemployment rate decreased from 6.6 percent to 5.4 percent.

Following slower GDP growth in the first half of 1995, the FOMC lowered the federal funds rate target by 75 basis points over the next year, landing around 5.3 percent in early 1996. Notably, the decision to lower rates was not fueled by a looming recession or increasing unemployment. For this reason, many look at this cycle as an example (perhaps the only example) of a "soft landing." However, since PCE inflation never rose above 2.3 percent, a more accurate description might be that the FOMC successfully "prevented takeoff" of inflation.

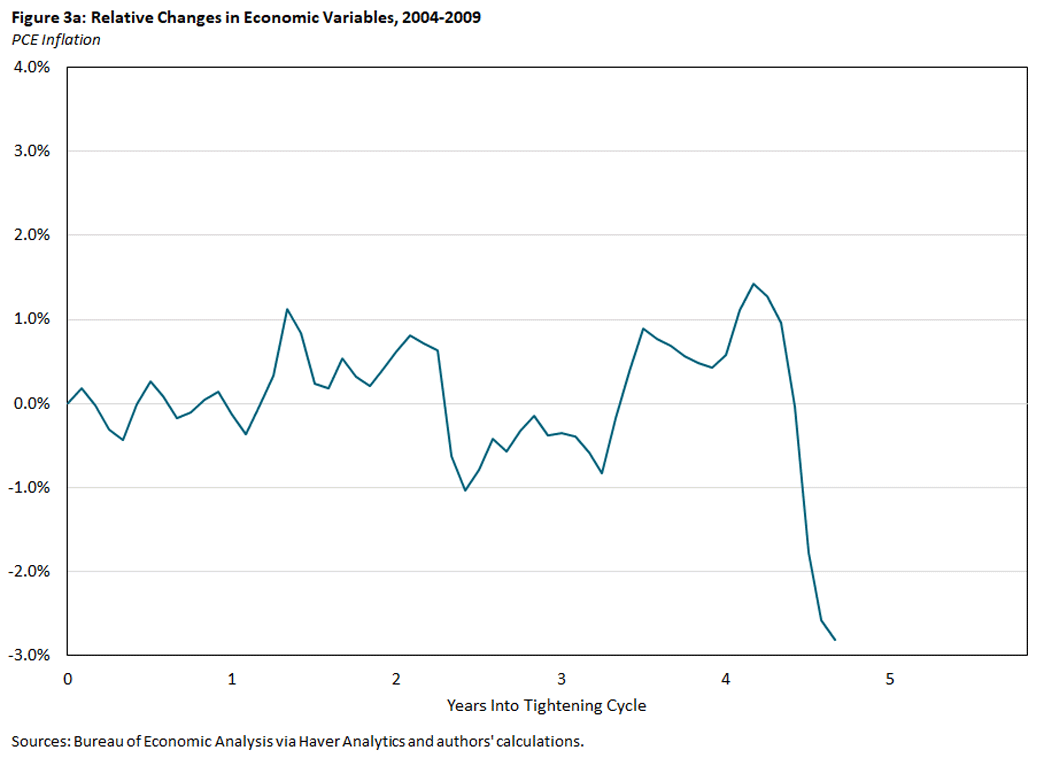

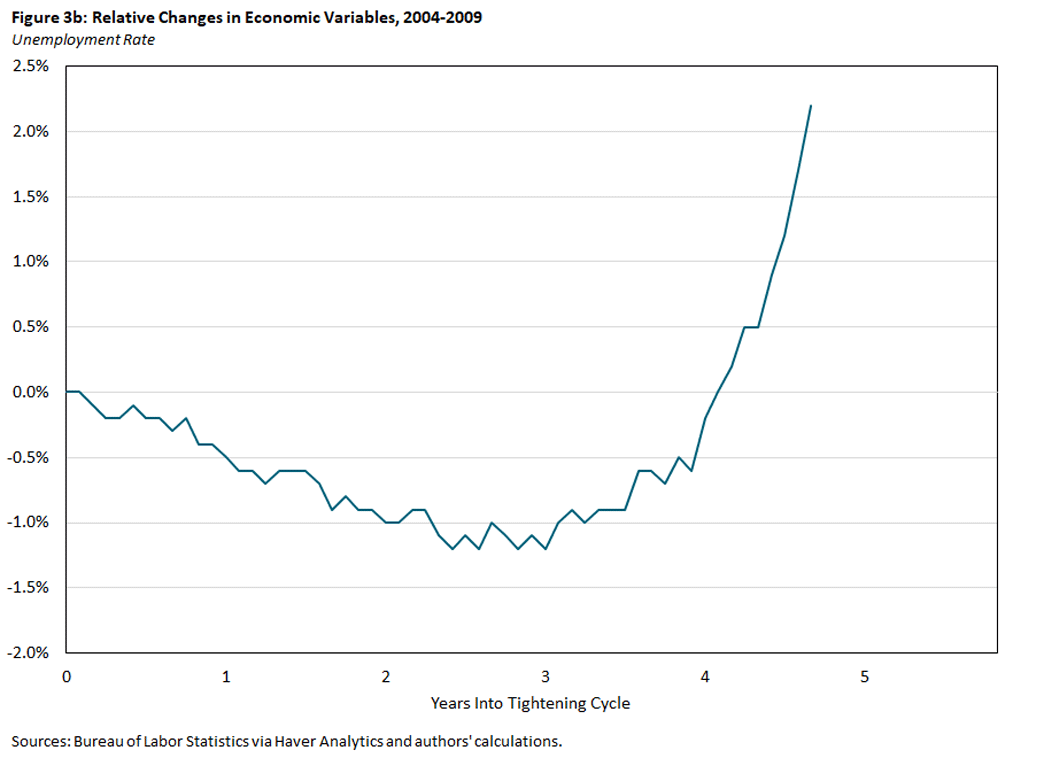

Rate Cycle: 2004-2008

In mid-2004, the federal funds effective rate sat around 1.0 percent following the dot-com crash and its associated recession in the early 2000s. With robust GDP growth in 2003 of 4.3 percent and PCE inflation at 2.9 percent in June 2004, the FOMC began raising the federal funds rate target. From June 2004 to July 2006, the federal funds effective rate increased to 5.25 percent.

Over the same period, however, PCE inflation also increased from 2.9 percent to 3.4 percent, and the unemployment rate decreased from 5.6 percent to 4.7 percent. Put another way, real activity continued at a high pace and prices rose despite the more restrictive stance of monetary policy. As in the 1987-1992 rate cycle, we interpret this episode as the Fed not responding soon enough (or perhaps not responding strongly enough) to stabilize prices. That said, in this cycle the FOMC held the federal funds effective rate at 5.25 percent for over a year, during which PCE inflation eventually dropped to 1.9 percent in August 2007.

The following month, the Fed began to cut rates in response to the financial crisis and Great Recession. The federal funds effective rate hit its lower bound of 0.15 percent in January 2009. At the same time, the PCE price index was experiencing deflation at -0.1 percent, and the unemployment rate had risen to 7.8 percent. (It would hit a peak of 10.0 percent that October.) Similar to Figure 1, Figure 3 shows the FOMC was unable to decrease inflation without the U.S. economy also experiencing a spike in unemployment.

How Is Today Different?

Following the COVID-19 pandemic, the federal funds effective rate was once again at its lower bound. In March 2022, the FOMC raised rates following a surge in PCE inflation to 6.4 percent. A little over a year later, the federal funds effective rate has increased to more than 5.0 percent. Over that same period, PCE inflation has decreased to 4.4 percent, while the unemployment rate has remained relatively unchanged, going from 3.8 percent to 3.7 percent.

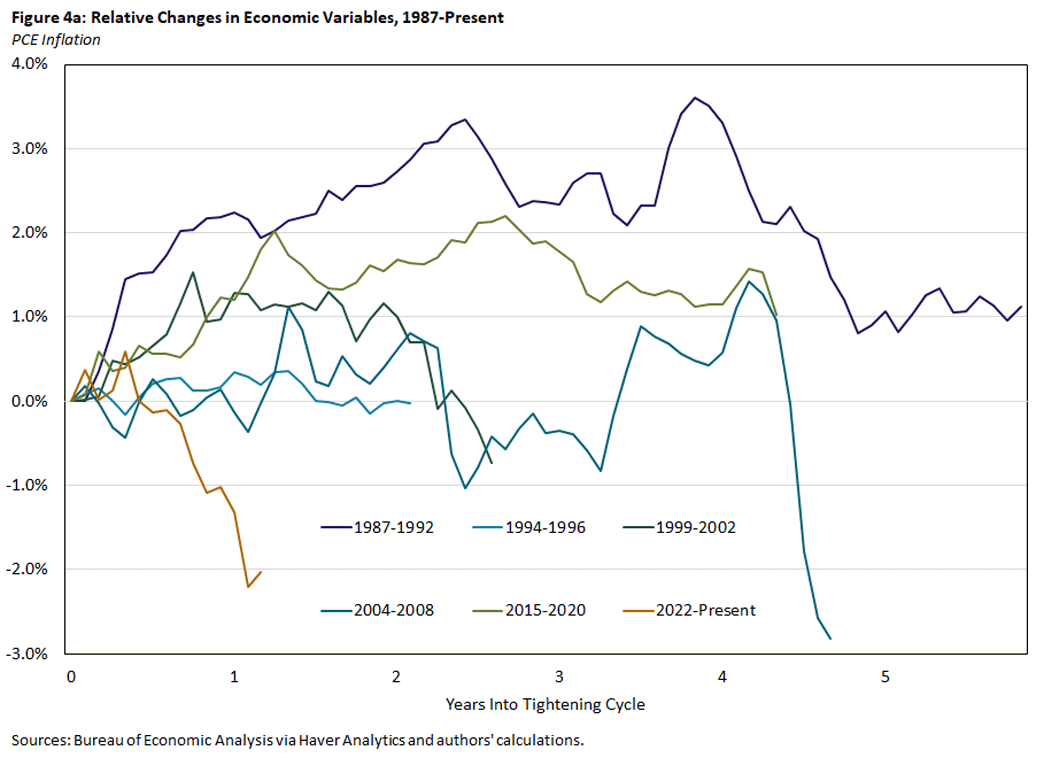

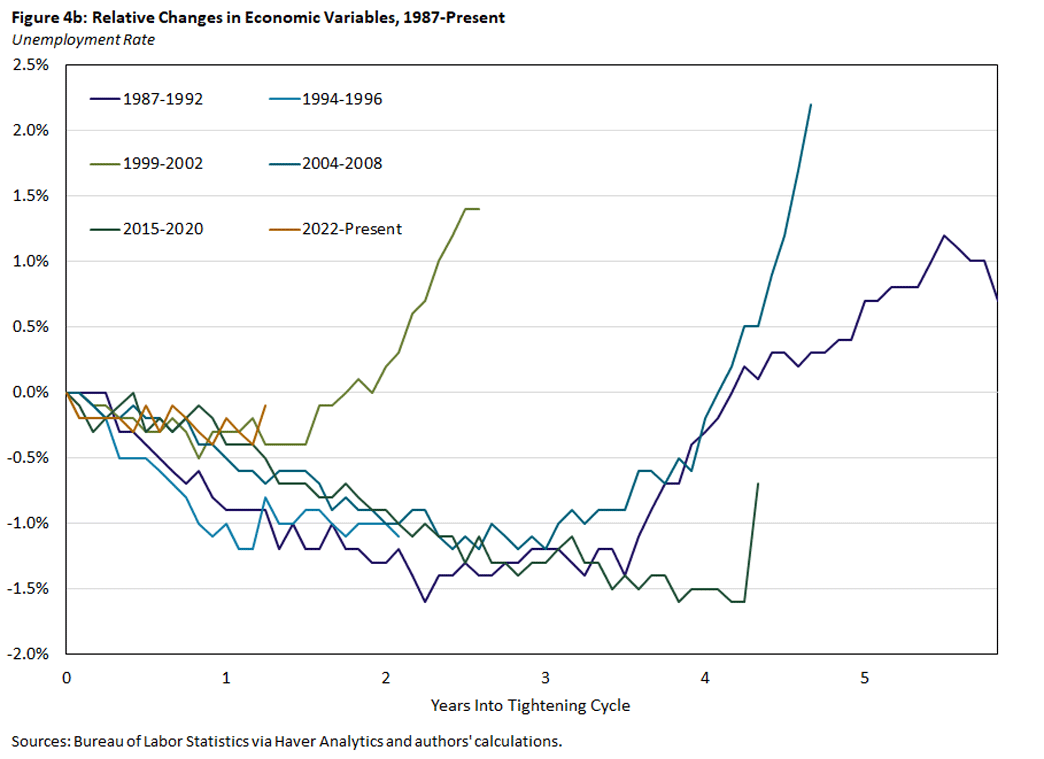

Figure 4 shows all the rate cycles since 1987. The current cycle is the first time over the entire postwar period the FOMC has made significant progress in lowering inflation without an associated increase in the unemployment rate.

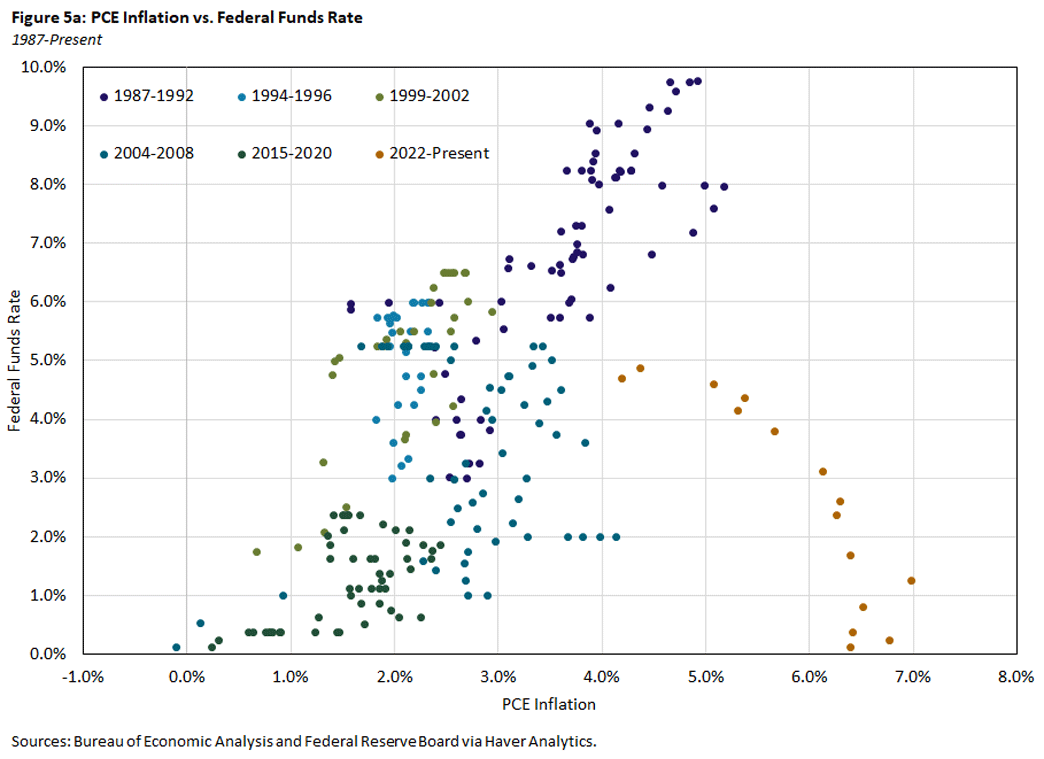

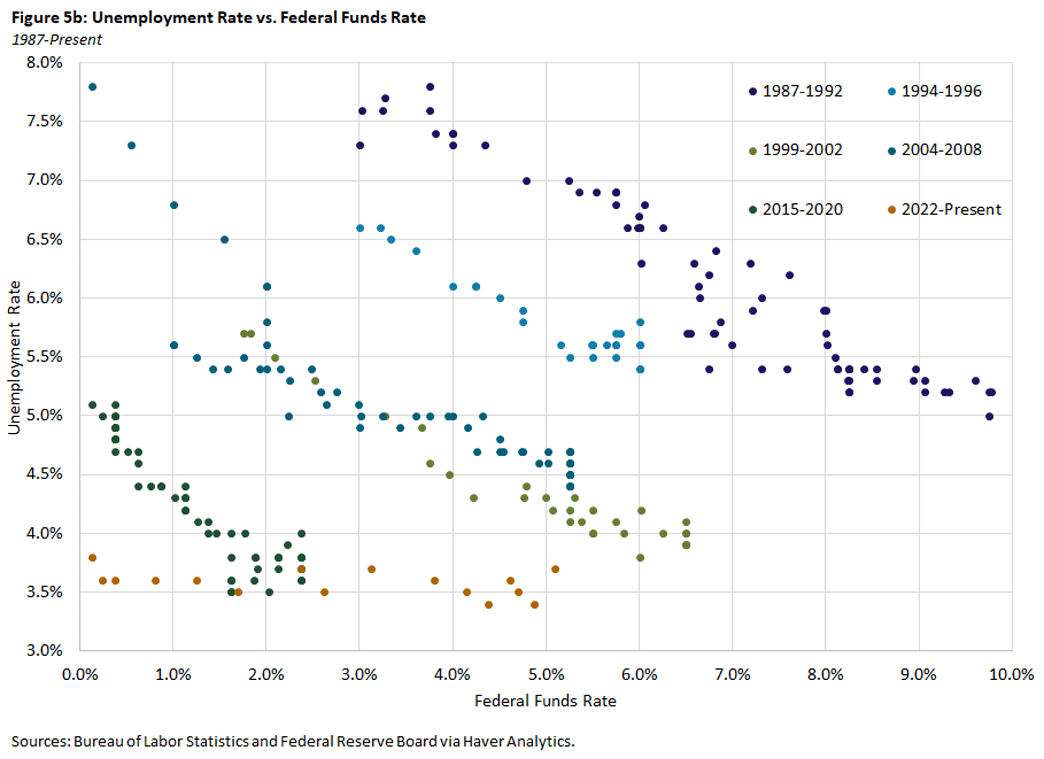

Figure 5 compares PCE inflation and unemployment with the federal funds rate during the past six rate cycles. There are a few important observations to take away from these charts.

First, with each new rate cycle, the unemployment rate has been lower and PCE inflation closer to its 2 percent target. In a sense, this is evidence that the Fed has been increasingly effective in fulfilling its dual mandate over the past several decades.

Second, the current rate episode sees us in uncharted waters. This is especially clear looking at Figure 5a, which tells us the federal funds rate had never been so low with inflation so high at a point when the Fed began increasing rates. In addition, unemployment has never been this consistently low during a rate cycle. In past cycles, the unemployment rate dropped by a percentage point or more as the economy expanded and the FOMC raised rates. However, this is unlikely to happen today when the unemployment rate is already at 3.7 percent.

Conclusion

In contrasting the current rate cycle with past episodes, it appears that the FOMC has been uniquely successful thus far in lowering inflation while leaving the unemployment rate at its lowest levels in roughly half a century. Moreover, with the recent pause at the June FOMC meeting, the built-in policy tightening over the last year may bring about further declines in inflation without a dramatic rise in the unemployment rate. This would be a first in the postwar U.S. economic experience.

The FOMC so far has had to strive to lower inflation without a recessionary shock, such as the ones in 1990 and 2008, that helped ease inflationary pressures on prices. However, with little guidance from past rate cycles, the FOMC will have to remain vigilant to avoid missing its target should the economy prove more resilient than anticipated.

Conner Mulloy was a former research assistant, Pierre-Daniel Sarte is a senior advisor and Erin Henry is a research assistant, all in the Research Department at the Federal Reserve Bank of Richmond.

To cite this Economic Brief, please use the following format: Sarte, Pierre-Daniel. (August 2023) "A Rate Cycle Unlike Any Other." Federal Reserve Bank of Richmond Economic Brief, No. 23-26.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us