A Small Contribution to Measuring the Lags in Monetary Policy Transmission

Economic Brief

September 2023, No. 23-30

From May 2022 to July 2023, holdings of small CDs have risen from virtually nothing to more than $900 billion. While this is a dramatic increase, it has come on the heels of a sharp increase in interest rates, and the increase in CDs did not begin until well after interest rates started rising. In this article, I provide some historical perspective for the recent increase in CDs and retail money market mutual fund (MMMF) balances. What is the typical lag between market interest rate increases and increases in CD and MMMF balances? Is the recent increase unusually large, or does history suggest there is more in store?

There has been a dramatic increase in short-term interest rates since late 2021. After keeping its fed funds rate target at the effective lower bound from March 2020 until March 2022, the Federal Open Market Committee (FOMC) has since raised the target 525 basis points. The one-year Treasury bill rate started rising in the fall of 2021 (incorporating expectations that the Fed would raise rates in the coming months) and stands at 5.39 percent as of this writing.

The Growth of CDs and MMMFs

When the Fed began raising rates, households had reduced their holdings of small time deposits (henceforth, CDs) to $45 billion, the lowest number since June 1966. In May 2022, both CD and retail money market mutual fund (MMMF) balances started to increase, and that has continued: Small CDs (those issued in amounts less than $100,000) rose from $37 billion in May 2022 to $901 billion in July 2023, and retail MMMFs rose from $928 billion to $1,527 billion over the same period.1

We focus on small CDs and retail MMMFs because they are relatively liquid assets accessible to households with moderate levels of savings, and they pay a market-determined interest rate. As those rates rise, CDs and MMMFs become more attractive relative to demand deposits that pay very little interest.2 As the FOMC changes short-term interest rates, the behavior of small CDs and retail MMMFs is interesting for two reasons:

- It provides direct information about one effect of those interest rate changes.3

- Changes in CD and MMMF holdings may signal that households are shifting their consumption plans. Although CDs and MMFs are relatively liquid assets, they are less liquid than demand deposits, and thus shifts in and out of those instruments may be associated with changing consumption plans.4

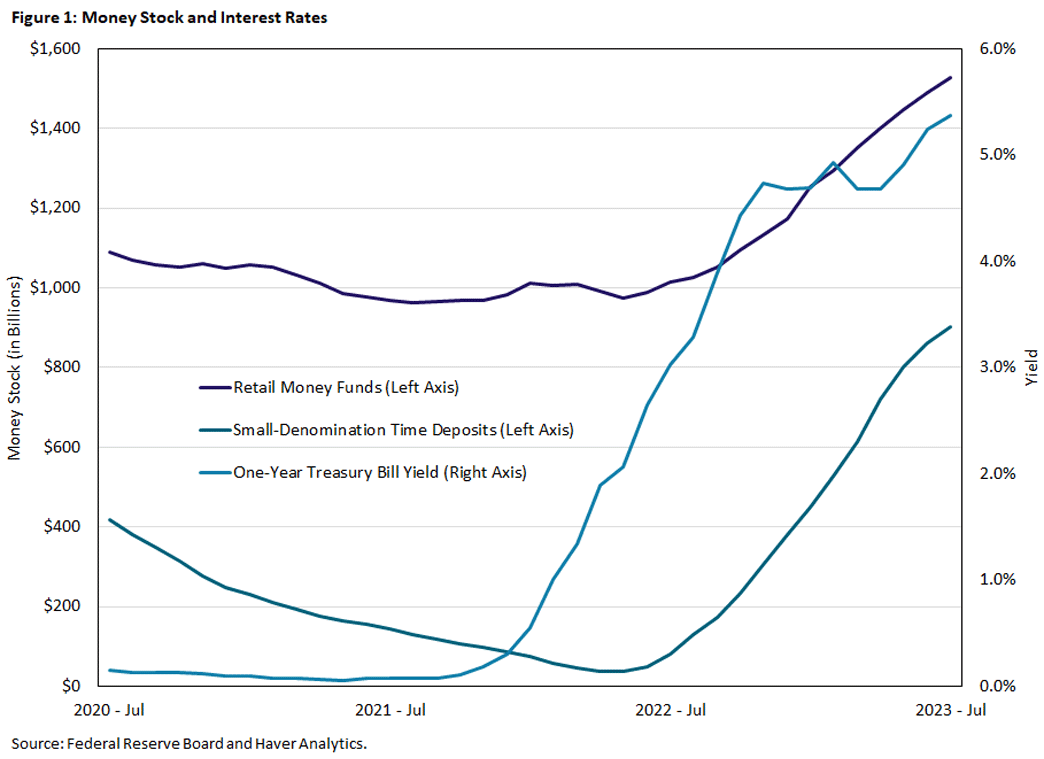

We use the one-year Treasury bill rate as a benchmark for studying CD and MMF balances. While the Treasury rate is not the rate earned on those instruments,5 it is a fairly close alternative available to households, riskier but more liquid than a CD, and riskier and less liquid than an MMMF.6 Figure 1 plots balances in CDs and MMMFs, along with the 1-year T-bill rate over the last three years.

Two aspects of the figure stand out:

- The increase in account balances began about eight months after the increase in the T-bill rate.

- Although the T-bill rate plateaued in late 2022, it began increasing again in April.

Will Account Balances Keep Rising?

Should we expect the account balances to keep increasing even beyond when the T-bill rate stops increasing? To gain some insight into this question, we examine previous episodes of interest rate increases and the associated behavior of CDs and MMMFs.

Figure 2 plots time series for the T-bill rate and the CD + MMMF share of M2 from 1983 to the present. We plot the share in M2 instead of the level of account balances because the level is heavily influenced by inflation and the growth of the real economy over this period.

Not surprisingly, the two series move broadly together, at both low and medium frequencies. Historically, the components of M2 other than CDs and MMMFs have paid very low interest rates. Thus, when market rates (represented in the figure by the T-bill rate) move up, households have an incentive to shift from non-interest-bearing accounts into CDs and MMMFs. From the figure, it appears that there is a consistent pattern of cycles in interest rates being followed with a lag by cycles in the interest-bearing share of M2. However, it also appears that the length of the lag varies from cycle to cycle.

Lagged Response of Account Balances to Interest Rates

Table 1 displays information about the six complete interest rate cycles starting in January 1983.7 (Prior to 1983, interest rates were high and extremely volatile, and the regulations governing interest bearing deposit accounts were much stricter.) Table 1 normalizes CDs + MMMFs by the level of M2 in the initial month of each cycle (the month of the rate trough), rather than by the contemporaneous level of M2 as in Figure 2. For plotting the time series, it is convenient to use the contemporaneous level, but this measure is affected by changes in M2 as well as changes in CDs + MMMFs. Normalizing each cycle by the initial M2 has the benefit of controlling for trends, while preventing within-cycle movements in M2 from affecting the measure.

| Table 1: Interest Rate Cycles | |||||||

|---|---|---|---|---|---|---|---|

| Rate Trough | Length of Rate cycle (Months) | Share Trough, Lag From Rate Trough (Months) | Share Peak, Lag From Rate Peak (Months) | Rate Increase, Trough to Peak (pp) | Share Increase, Trough to Peak, Relative to M2 in Trough Month (pp) | Rate Elasticity of Share | Peak Interest Rate |

| Jan 1983 | 17 | 5 | 4 | 3.46 | 8.5 | 2.46 | 12.08 |

| Oct 1986 | 29 | 6 | 11 | 3.85 | 15.4 | 4.00 | 9.57 |

| Apr 1993 | 20 | 12 | 36 | 3.9 | 13.3 | 3.42 | 7.14 |

| Oct 1998 | 19 | 9 | 8 | 2.21 | 6.4 | 2.88 | 6.33 |

| Jun 2003 | 37 | 18 | 19 | 4.21 | 12.1 | 2.87 | 5.22 |

| Oct 2014 | 49 | 30 | 8 | 2.6 | 3.4 | 1.31 | 2.7 |

| Sep 2021 | ≥22 | 8 | ? | ≥5.29 | ≥6.2 | ≥1.18 | ≥5.37 |

| Note: The "rate elasticity of share" is the ratio of the share increase to the rate increase. | |||||||

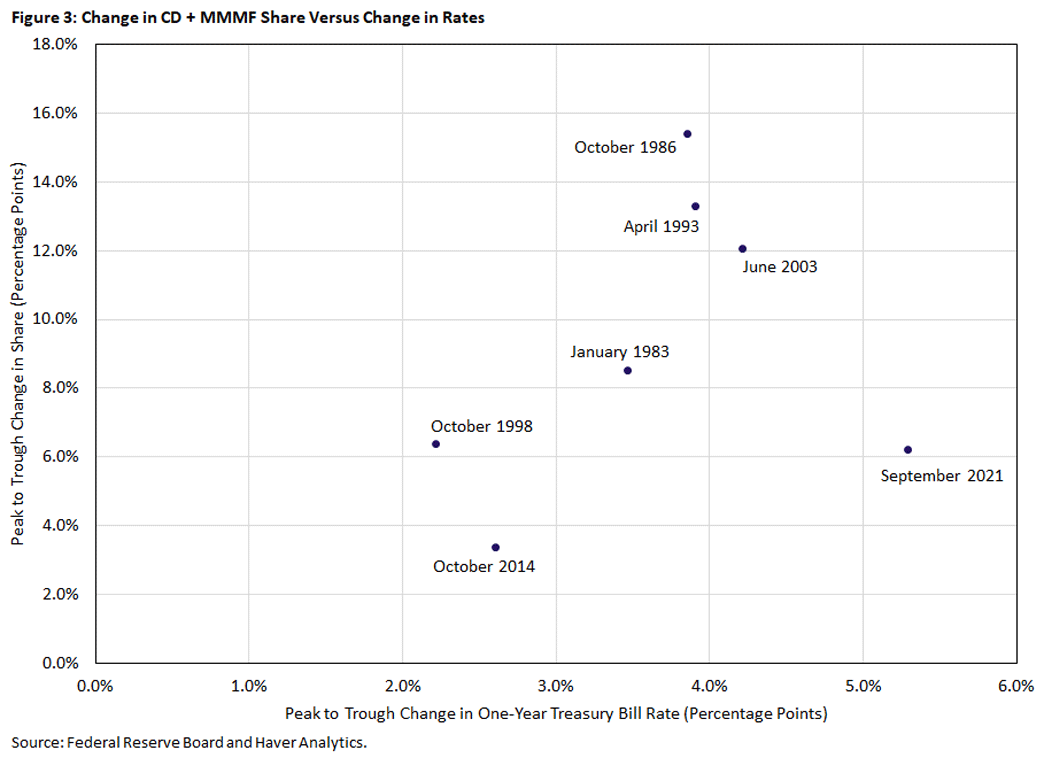

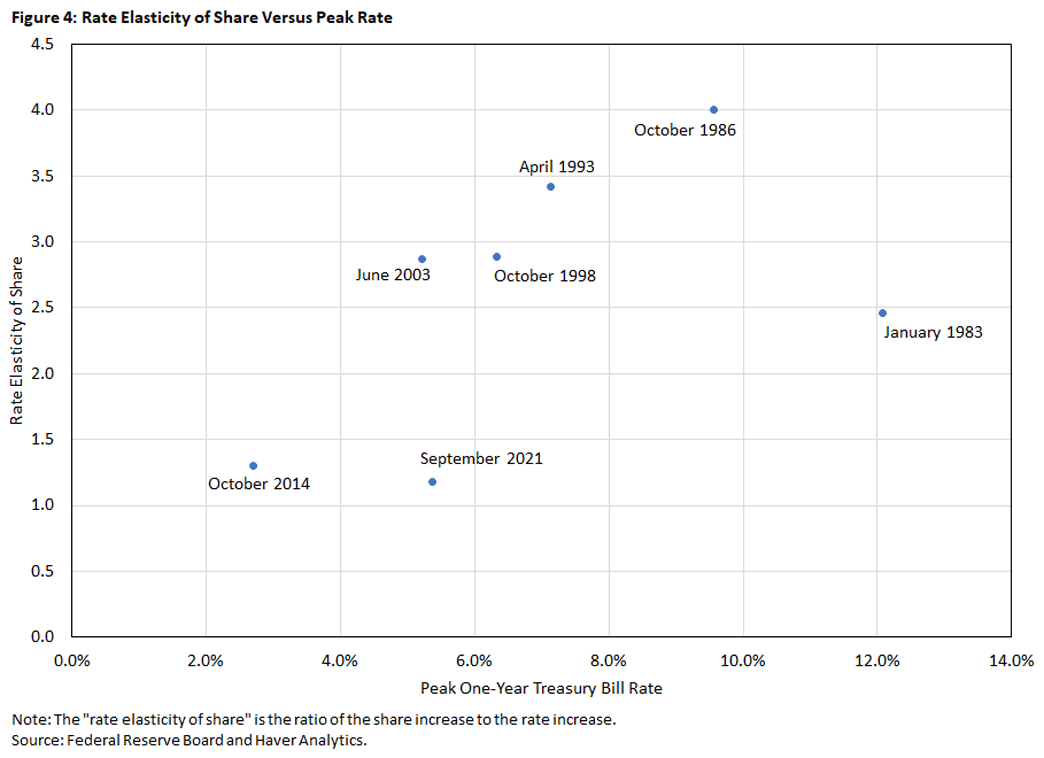

Figure 3 plots the share increase versus the rate increase for each cycle, and Figure 4 plots the interest elasticity of the share against the peak rate for each cycle. The interest rate elasticity of the share is defined as the ratio of the peak-to-trough change in the share to the peak-to-trough change in the T-bill rate.

Across the six cycles, the lag between "troughs" — the month at which rates began to increase and the month at which the share began to increase — varies from five to 30 months. Given the speed with which rates have increased, it is perhaps not surprising that the current episode had a lag of only eight months from the trough of rates to the trough of the share.

We can also measure the lag by comparing peaks. Those lags are also variable, and the lag from rate peak to share peak is typically as long as the lag from rate trough to share trough. If this pattern holds (and even if rates have already peaked), then the share will peak no sooner than March 2024. The one glaring exception — when the trough lag was much longer than the peak lag — was the previous rate cycle, starting in 2014. The initial months (even years) of that cycle had a very small increase in rates, so it seems unlikely to be a good model for the current cycle.

Size of Account Balance Increases

Finally, we can use previous episodes as a rough guide to how much more the share will increase. The average elasticity in previous episodes is 2.82. Applying that average to the current episode and assuming rates are at their peak, the share would increase another 8.7 percentage points, for a total increase of 14.9 percentage points.

Conclusion

We conclude with a brief discussion of "why" and "so what." The lagged response of CDs and MMMFs to increases in rates can reflect two factors:

- A lagged adjustment of CD and MMMF interest rates to Treasury rates

- A lagged adjustment of household behavior to CD and MMMF rates.

Presumably both factors are at work, but we do not attempt to disentangle them here.8

The lagged responses of CDs and MMMFs are interesting on their own from the standpoint of understanding household behavior. They may also be important for understanding monetary policy transmission to real economic activity, but the extent to which that is true cannot be established by the table and figures presented here. The household portfolio adjustments could be just that, without any implications for household spending behavior. At the other end of the spectrum, the adjustments could correspond one-for-one with increases in saving and therefore reductions in consumption. HANK models could be used to make progress on this topic. However, most current versions of those models9 do not distinguish between demand deposits, CDs and MMMFs, so the already-complicated environments would need to be enriched even further.

Alexander Wolman is vice president for monetary and macroeconomic research in the Research Department.

1

Note that small CDs had declined nearly to zero by May 2022, but retail MMMF holdings were still substantial. When rates are effectively zero (as they had been since March 2020), there is no reason to lock up money in a CD. However, MMMF balances are not locked up, so some households continue to effectively use MMMFs as transaction accounts even when rates are zero.

2

The relationship between CDs and MMMFs on which we focus can be viewed as the inverse of the more commonly studied money demand function.

3

As always, one must be careful about assigning causation. It seems clear that changes in fund balances are not causing changes in interest rates (especially given the lags we find), but one cannot rule out that both variables are responding to a third factor (for example, concern about future inflation). We acknowledge this concern but proceed under the assumption that the primary determinant of fund balances (appropriately normalized) is the level of nominal interest rates.

4

Of course, increases in CD and MMMF holdings could represent transfers from less-liquid assets, such as stocks.

5

We focus on the one-year T-bill rate rather than the rates paid on CDs and MMMFs because movements in the former summarize movements in the expected monetary policy interest rate over the next year. As an alternative, shorter-term T-bill rates are also attractive investments when interests rise, especially when there is substantial uncertainty about near-term rates, as there was in mid-2022. However, shorter-term rates do not reflect the broader stance of monetary policy.

6

"Risk" here refers to interest rate risk, not credit risk. A fixed-rate CD and a one-year Treasury bill are risky to the holder because market interest rates could rise after the instrument is purchased, lowering its value.

7

See the August 2023 article "A Rate Cycle Unlike Any Other" for a discussion of how the current rate cycle compares to past ones.

8

See the April 2023 article "Monetary Policy Transmission and the Size of the Money Market Fund Industry: An Update" and the references therein.

9

For example, see the 2018 paper "Monetary Policy According to HANK."

To cite this Economic Brief, please use the following format: Wolman, Alexander. (September 2023) "A Small Contribution to Measuring the Lags in Monetary Policy Transmission." Federal Reserve Bank of Richmond Economic Brief, No. 23-30.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us