Workers for the Right Wage

Macro Minute

August 3, 2021

Recently, the news has been filled with stories of employers unable to find workers. While there's disagreement over whether this is because of ongoing health concerns related to the pandemic, lack of child care while schools are out, fiscal support allowing unemployed workers to delay their job search or some other reason, many businesses have pointed to a shortage of labor as one of their top concerns over the past few months.

This is evident in business surveys. In the National Federation of Independent Business's monthly Small Business Survey, 56 percent of small businesses reported few or no qualified applicants for job openings in June, just one percentage point off the all-time high reached the prior month. And in July, the Richmond Fed's Survey of Manufacturing Activity reported that the share of firms facing a decline in qualified labor was 34 percentage points higher than the share of firms having an easier time finding workers.

But is every industry experiencing the same difficulty finding workers? And are the industries having more trouble raising wages in response?

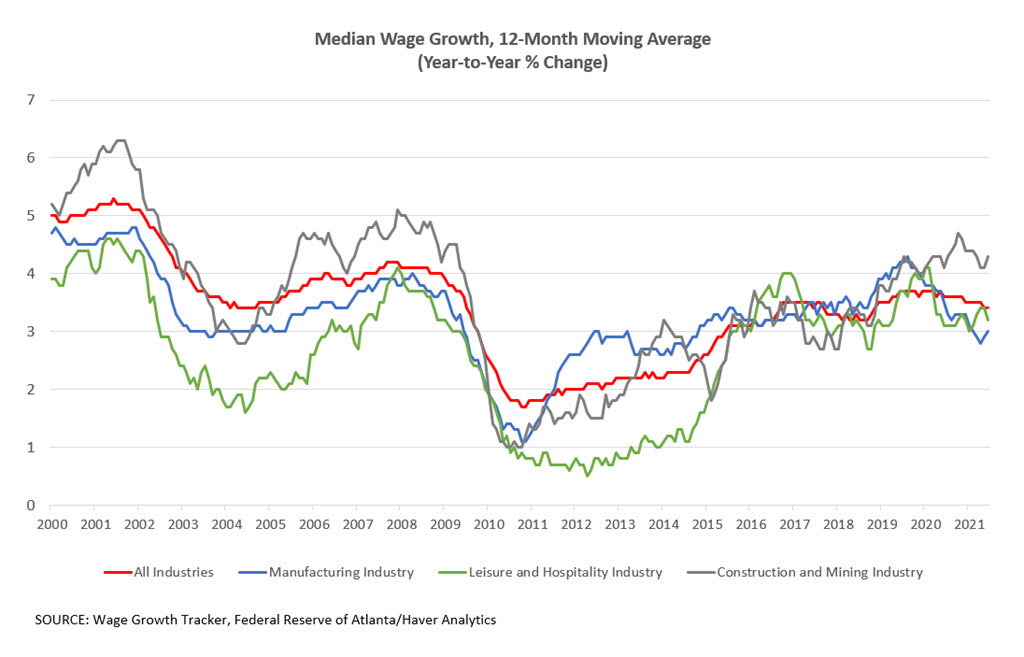

"One might guess that wages would be rising the fastest in industries that are the most desperate for workers. But ... this hasn't been true across the board."

To answer these questions, we can turn to one of the most informative surveys of labor market conditions, the Job Openings and Labor Turnover Survey (JOLTS) released monthly by the Bureau of Labor Statistics. According to the May JOLTS numbers, total job openings rose to a record 9.2 million in May 2021, with the job openings rate remaining at a record-high 6.0 percent. But hires didn't rise accordingly: May saw 5.9 million hires, similar to the February 2020 pre-pandemic level, and a hires rate of 4.1 percent.

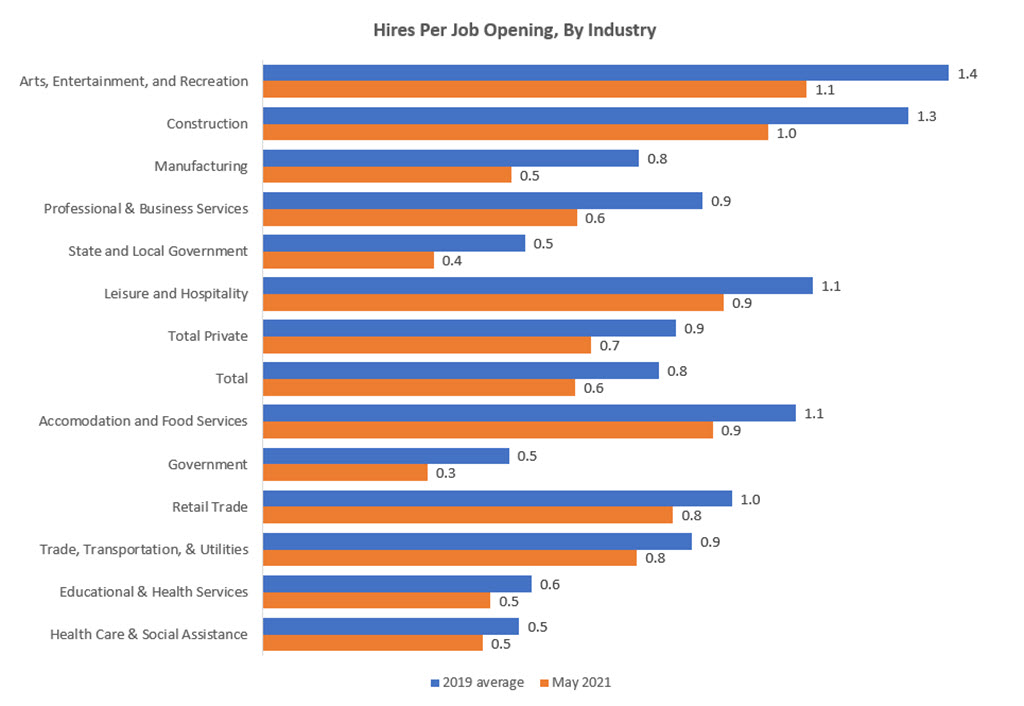

One way to measure differences across industries is the hires-per-job-opening ratio, which compares the number of hires that occur during a month to the number of open jobs remaining at the end of the month. Smaller numbers indicate difficulty hiring workers or other issues with the hiring or job posting process. To see which industries are facing more hiring challenges today compared to 2019, Figure 1 below compares the hires-per-job-opening ratio by industry in May 2021 to the pre-pandemic ratio (the 2019 average), ordered by the difference in this ratio over the two time periods. The arts, entertainment, and recreation industry is having the most difficulty hiring compared to before the pandemic, with a gap of 29.2 percentage points, followed by the construction industry with a gap of 28.9 percentage points and manufacturing with a gap of 26.2 percentage points. Though every industry appears to be having more trouble hiring today compared to before the pandemic, this appears to be less true in the health care and social assistance industry, with the ratio of hires per job opening only 7.5 percentage points lower than the pre-pandemic level.

One might guess that wages would be rising the fastest in industries that are the most desperate for workers. But Figure 2 uses data from the Atlanta Fed's Wage Growth Tracker to illustrate that this hasn't been true across the board (see chart below). For example, construction, manufacturing, and leisure and hospitality have experienced greater hiring challenges relative to the economy as a whole. But out of the three industries, only construction has seen median wages rising faster than overall median wages. In contrast, median wage growth in manufacturing and leisure and hospitality has been slower than overall median wage growth.

Does this mean further wage growth in the manufacturing and leisure and hospitality industries is on the horizon? For example, we've seen a huge amount of turnover in leisure and hospitality, and the data might be slow to reflect higher wages for the most recently hired workers. Or will we see workers in these industries start coming back in the fall, even without the lure of higher wages, as unemployment benefits expire and schools return to in-person learning? We'll know more in a few weeks' time, and the way this situation unfolds will influence how Fed policymakers view the economy's progress toward the Fed's inflation and employment goals.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us