More on Mismatch

Macro Minute

November 9, 2021

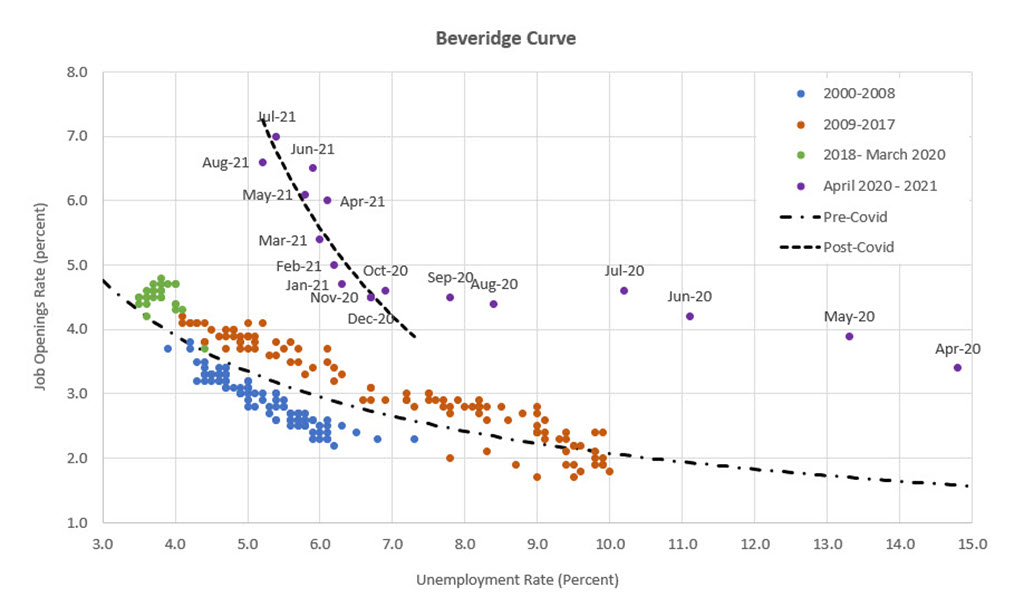

One of the most striking features of the post-COVID-19 labor market is the outward shift in the Beveridge curve, which is the inverse relationship between the unemployment rate and the job openings rate.

"As the economy has continued to recover, labor demand has grown much faster than labor supply."

When workers are in high demand, there tend to be more job openings and lower unemployment, and vice versa. However, as discussed in a recent Economic Brief by Richmond Fed economist Thomas Lubik, in the COVID-19 era this relationship has shifted outward. (See Figure 1 below.) While there is still a negative relationship between the job openings and unemployment rates, these days it takes a lot more job openings to get to the same unemployment rate.

This shift suggests the job market may be grappling with a high degree of labor market mismatch. Employers could be posting more open positions in part because the applicants they're getting, if any, aren't the right fit for the job. Meanwhile, workers may be increasingly selective about which jobs they return to and more selective about what salary they'll accept. Whether the Beveridge curve returns to its pre-pandemic pattern remains an open question that will be key for shaping how a post-COVID-19 economy at maximum employment should look.

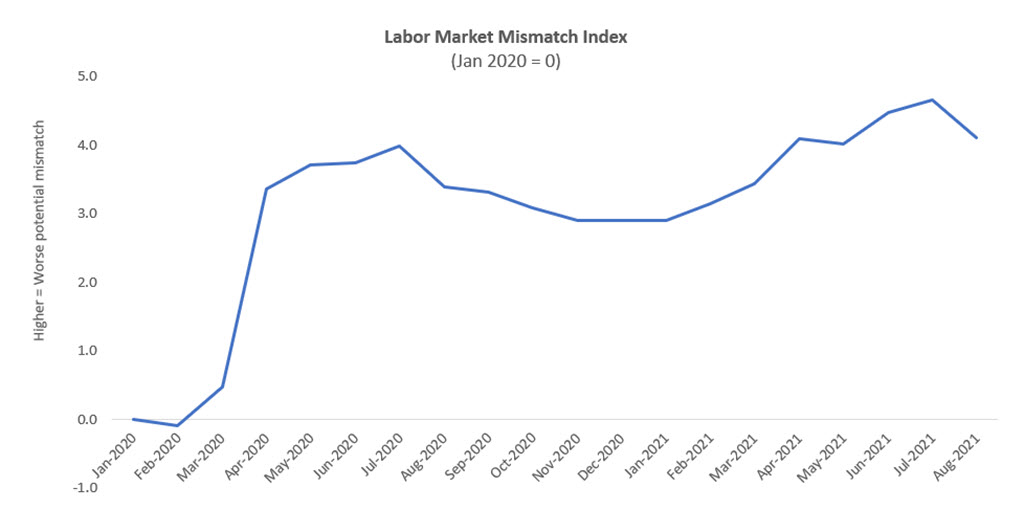

Motivated by the observation that jumps in the Beveridge curve could correspond to labor mismatch issues, we calculated a labor mismatch index based on how far the curve is from its pre-pandemic pattern. This index is the difference between the current job openings rate and the job openings rate implied by the pre-pandemic Beveridge curve (i.e., a version of the dashed line in Figure 1, estimated on data from January 2009 through December 2019). We normalized the index in January 2020 to zero, creating the graph in Figure 2 below.

April 2020 saw a huge collapse in labor demand as many workers in high-contact service sector industries were laid off. Consequently, the unemployment and job openings rates were dislodged significantly from their usual pre-pandemic Beveridge curve relationship, and the situation worsened through July. Subsequently, with the gradual reopening of the economy and loosening restrictions, unemployment declined and the post-pandemic curve retraced some of the distance back to normal, with the index recovering from 4 in July 2020 to 2.9 by December 2020.

Since the start of 2021, however, the efficiency with which workers are matched with employers has worsened. As the economy has continued to recover, labor demand has grown much faster than labor supply. This has led to growth in the job openings rate that has not been accompanied by the kind of improvement in the unemployment rate that the pre-pandemic Beveridge curve would imply. As of August 2021, the curve is further away from the pre-pandemic curve than it was in July 2020, according to Figure 2.

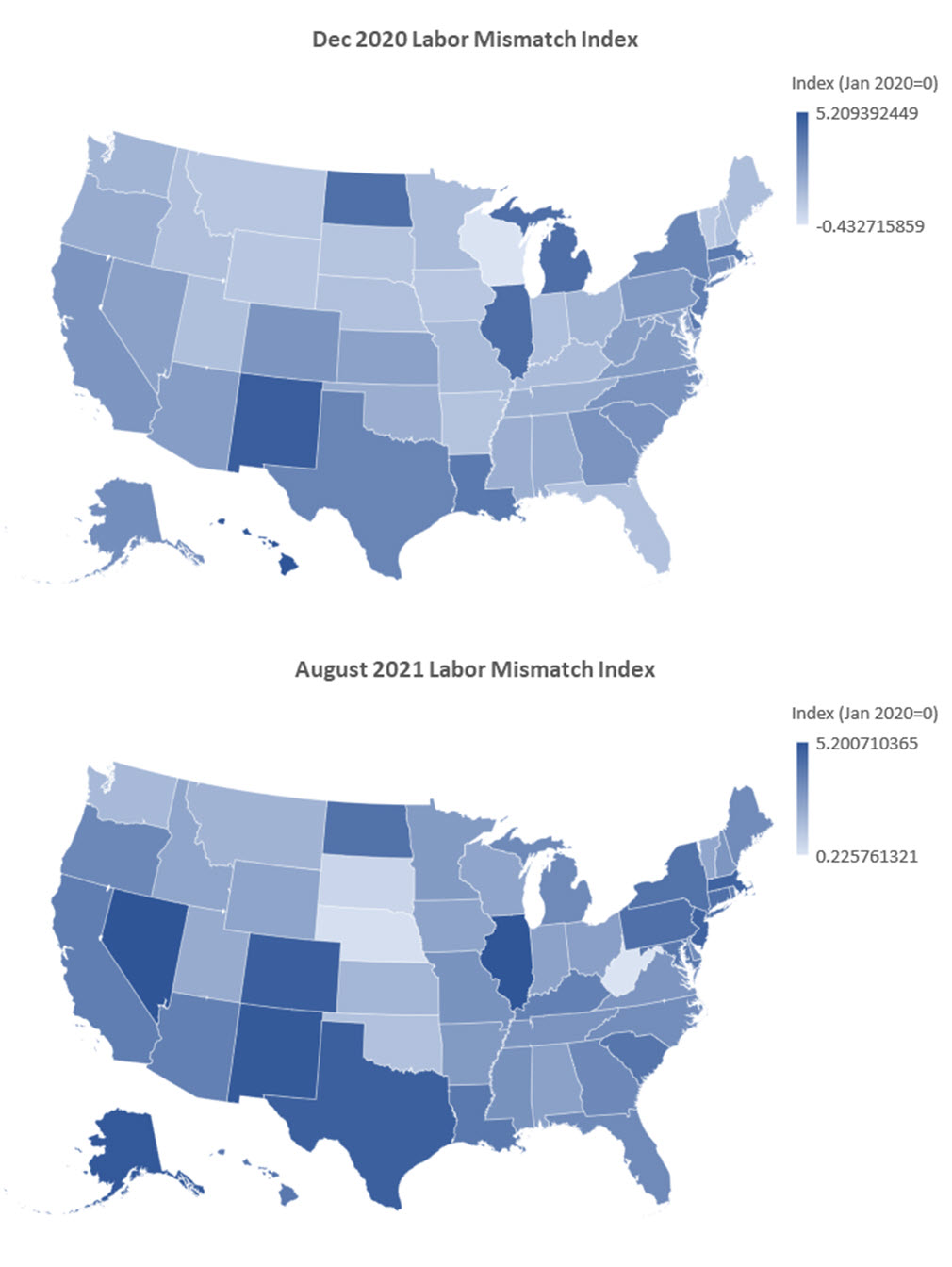

We calculated the mismatch index using recently published state-level data from the Bureau of Labor Statistics (BLS). As the BLS notes, these state-level estimates are volatile, so the results presented here may differ from actual labor market conditions in each state due to sampling error, seasonality or other sources of measurement error. Nevertheless, we found evidence supporting many anecdotal accounts, such as those in the Fed's October 2021 Beige Book, that the usual process of matching workers to jobs is under pressure.

Figure 3 below compares the level of the labor market mismatch index in December 2020 and August 2021. Despite worsening matching efficiency for the entire country, labor mismatch in some states has normalized more than others. For example, West Virginia improved 2 points, Hawaii improved 1.3 points, Michigan improved 0.8 points and Nebraska improved 0.5 points.

However, the maps suggest mismatches are becoming more geographically widespread. Eight states had scores improve between December 2020 and August 2021, compared to 43 states including the District of Columbia, where scores worsened. This brings the risk that ongoing pressures, such as rising wages and skills shortages, will persist for a longer duration.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us