Where the Spending Cutbacks Are

Macro Minute

February 07, 2023

Are households cutting back on spending, and if so, where?

Several indicators suggest that household spending started to dip at the end of 2022. In December, retail sales — which are heavily skewed toward goods — declined 1.1 percent monthly after dropping 1 percent in November. Personal consumption expenditures (PCE) — which capture both goods and services — fell 0.2 percent monthly following a 0.1 percent decline in November.

It's a little tricky to interpret the data around the holiday season. Even though both series are seasonally adjusted to control for typical spending patterns around this time of year, 2022 may have seen an earlier-than-usual pickup in holiday spending, leading to weaker monthly growth rates in November and December.

For example, October's PCE growth was quite strong at 0.8 percent. Also, the October retail sales report showed stronger monthly real (inflation-adjusted) sales growth in several holiday spending categories — such as clothing (0.9 percent); sporting goods, hobby, book and music stores (0.9 percent); and online shopping (0.9 percent) — compared to overall total growth (0.8 percent). Meanwhile, retailers may have tried to offset some of the pull ahead in demand by offering steeper discounts than usual in November and December, which would contribute to lower growth in nominal sales.

Nevertheless, if the decline in sales at the end of the year turns out to be more than a holiday blip, we could be in for a period of weaker growth, as consumption makes up about 68 percent of GDP.

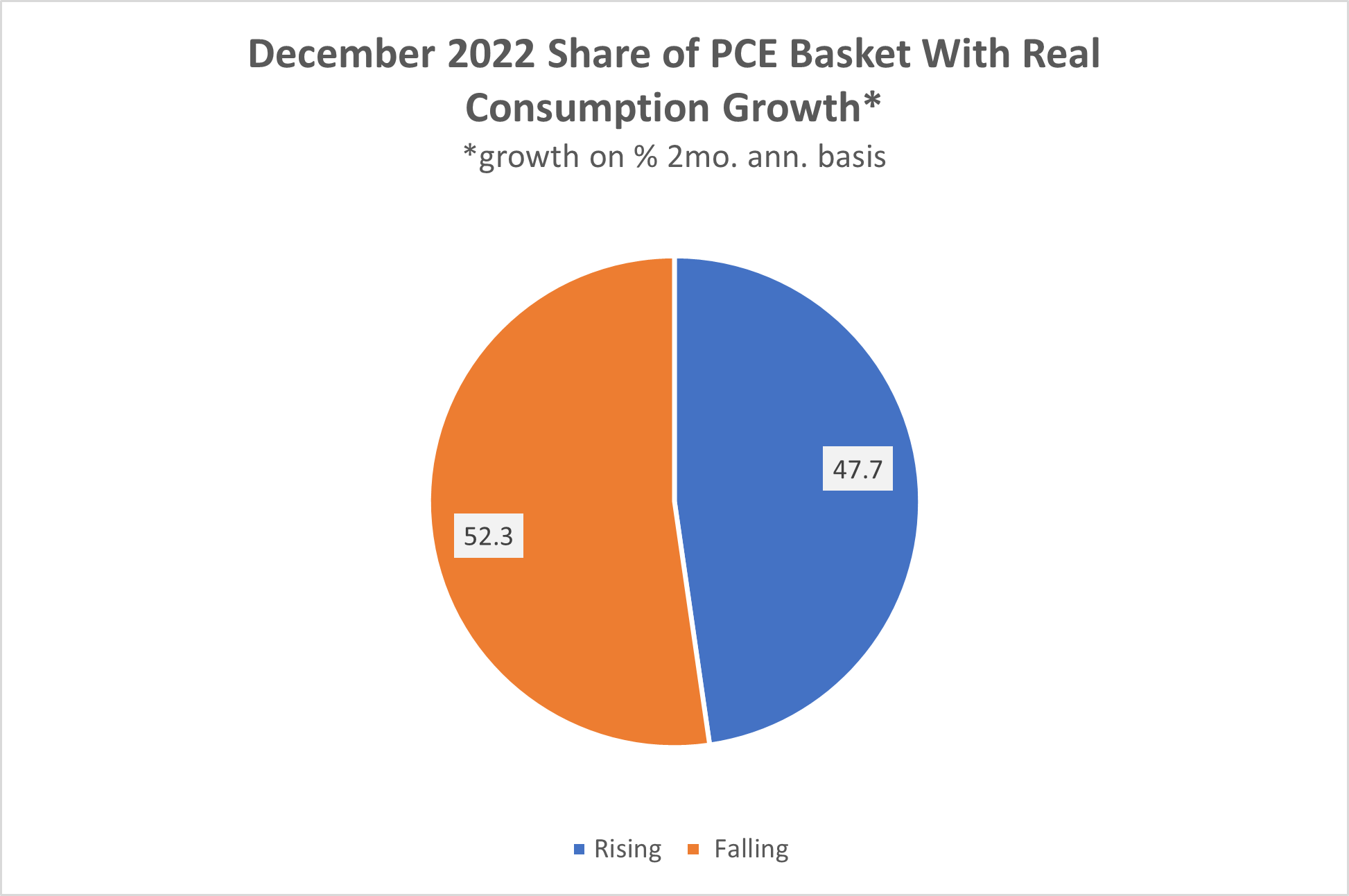

Peering under the hood of the headline spending number reveals that there are pockets where consumer spending continues to rise. Looking past October's spending jump, Figure 1 below combines data from the most recent two months when total spending dropped (November and December), showing the two-month annualized change in real PCE across major spending categories. The share of each category in the total PCE spending basket is shown in the labels next to each bar.

During this period, real spending continued to grow in several categories mostly related to services, including health care, housing, financial services and recreation. The fastest growing category captures spending on behalf of households by nonprofit institutions, which includes services like hospital care, nursing home care, and education that households consume without being explicitly charged.

In contrast, the categories that shrank in December were mostly related to goods such as motor vehicles and parts, clothing and footwear, and furniture and household durables. The declines in these categories may be related to the ongoing rotation of consumption back to services.

By adding up each category's share (Figure 2 below), we can see that 47.7 percent of the PCE consumption basket still continued to see increases in expenditure despite an overall drop in consumption during these two months. This nearly 50-50 split suggests that the consumer spending pullback hasn't broadened out across all categories quite yet.

But Figure 1 above also suggests that spending growth is now strongest in areas related to household necessities like health care and shelter. (A notable exception is the growth in recreation services during this period, though it should be noted that it makes up only 3.6 percent of total spending.) Households shifting discretionary spending toward essentials is one sign of consumers becoming more cautious. Keep following this blog for more updates on the state of household spending over the course of this year.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us