The Effects of Expiring Stay-at-Home Orders and the Shape of the Recovery

Special Report

May 26, 2020

Does the expiration of state stay-at-home orders — issued in response to the COVID-19 pandemic — facilitate economic recovery in a substantial way? What is the likely shape of the recovery? Are we seeing any indication of a sharp, quick rebound in economic activity (a so-called V-shaped recovery)?

To seek insight into these questions, we use data from two different sources. First, we use data from Homebase, which tracks local businesses and the hourly employees of these businesses around the United States. We have described these data in more detail in previous posts.1 Second, we use data from the Community Mobility Reports by Google. The data are based on users who have opted-in for Google to track their location history. The data provide mobility trends on a daily basis for various types of destinations: Grocery and Pharmacy, Parks, Transit Stations, Retail and Recreation (such as shopping malls), Residential, and Workplace. The mobility index for each destination is a combination of two factors: the number of visits and the length of stays.2

Overall, we find evidence that economic activity is starting to recover, and that the expiration of stay-at-home orders have a positive effect on the recovery speed, especially for those sectors most impacted by the lockdown orders. Currently, it seems like the United States is experiencing either a V- or a U-shaped recovery.

The Economic Effect of Lifting the Lockdown Measures

We classify states in two categories: those for which the stay-at-home order has expired and those for which the order is still in place. The number of states for which the stay-at-home order has already expired is 23. Such states include Alabama, Colorado, Florida, Montana, South Carolina, and West Virginia. In these states, stay-at-home orders have been replaced with new guidelines that aim to minimize the infection risk. For example, restaurants are required to operate at a half or a third of normal capacity, and social distancing is required inside establishments such as gyms and places of worship. For a second group of states (a total of 19), the order has yet to expire or there is currently no expiration date. For example, the order for Illinois and Delaware expires May 31, for Virginia it expires on June 6, and California has no set date for the expiration of its order. The rest of the states never issued a stay-at-home order and thus, for simplicity, we exclude them from the analysis.

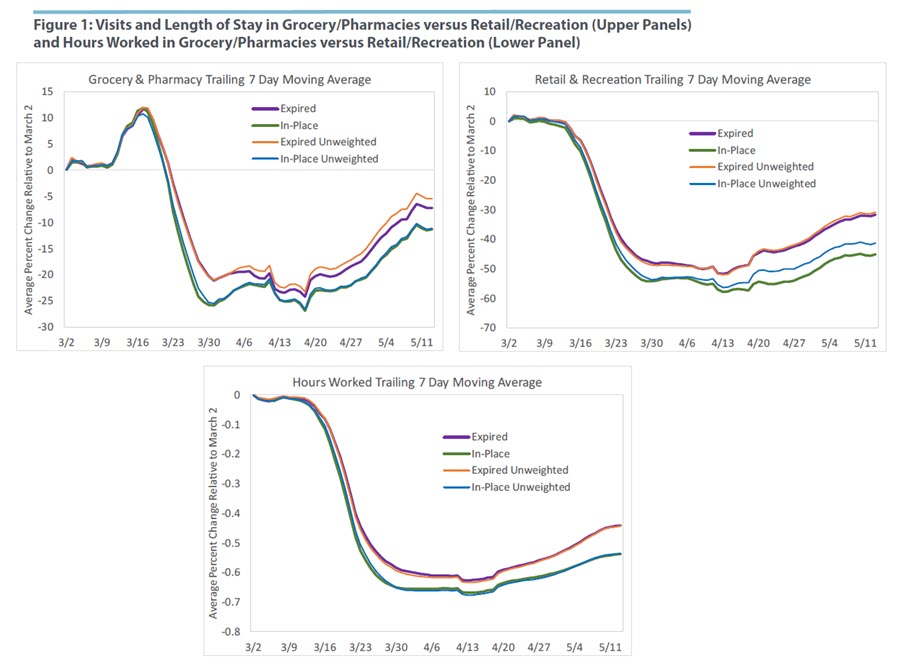

Figure 1 shows visits/length of stay in grocery and pharmacies (upper left panel), visits/length of stay in retail and recreation (right upper panel), and hours worked (lower panel) for the group of states with expired orders and the group of states with orders still in place. For each state, we compute the difference in each variable relative to March 2 (we also do a seven-day trailing moving average for each series to smooth out day effects). Each figure presents the group average of these relative variables across states, weighted by state population (solid line) as well as unweighted (dashed line). The figures show that both states with expired orders and states with orders still in place are experiencing a recovery of economic activity. This suggests that either consumers' sentiment is improving or perhaps people are starting to experience "quarantine fatigue."

In states with expired orders, visits to grocery and pharmacies rise at the same pace as in states with orders still in effect (with the exception of a upward level shift in visits around April 18). The effect of lifting the lockdown is more visible for visits to retail and recreation. Until mid-April, the gap in visits was relatively small and constant. After mid-April, the gap widens. The difference is more pronounced in the weighted case, implying that some small states with orders still in effect are experiencing high growth in the index. Similarly, the hours worked by hourly employees' series is increasing slightly faster for states with expired orders relative to states with orders still in effect.

One rationalization of this difference is the distinction in how the two types of establishments were treated during lockdown. Grocery and pharmacies are typically considered essential businesses and thus remained open during the lockdown period. Retail and recreation stores (e.g., gyms, hair salons, shopping malls) were mostly not considered essential businesses, and thus many were ordered to close during the lockdown. As states open up, a larger share of businesses in retail and recreation open their doors relative to businesses in grocery and pharmacies, as these were mostly already open, naturally attracting a higher inflow of consumers. This may explain the faster recovery observed in retail and recreation for those states that opened up the economy relative to those yet to open, relative to the difference in recovery observed among the two groups of states in grocery and pharmacies.

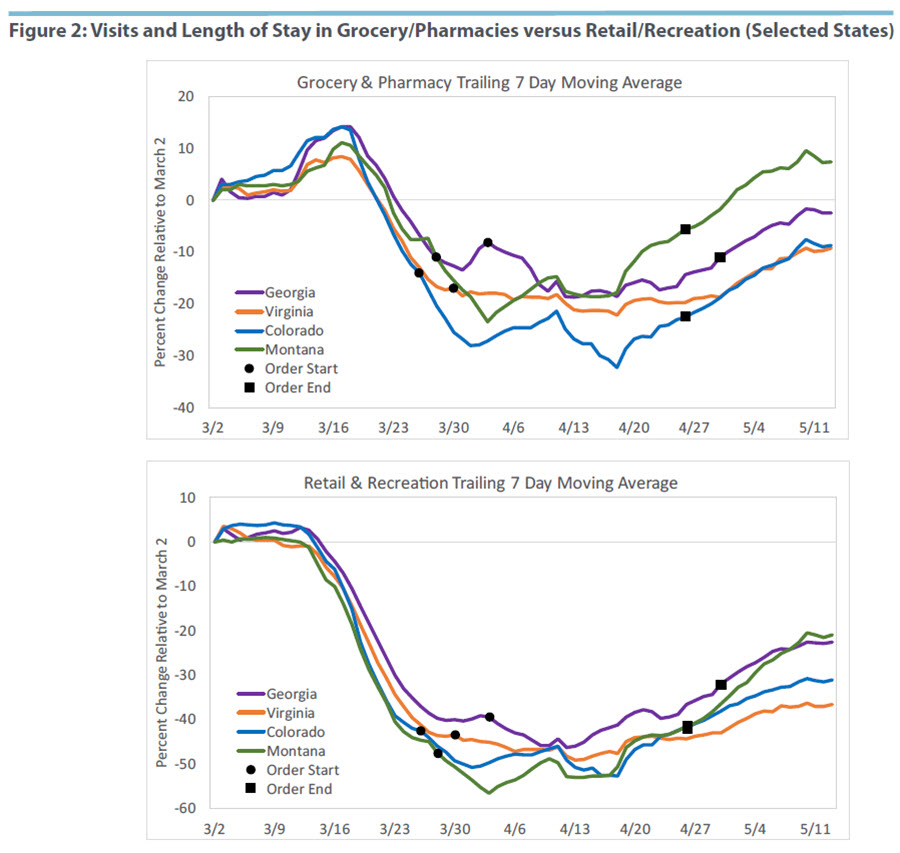

Figure 2 plots visits/length of stay at grocery and pharmacies (upper panel) and retail and recreation (lower panel) for selected states. As in Figure 1, we compute the difference in each variable relative to March 2, and then we compute a seven-day trailing moving average. We pick three states for which the stay-at-home order has expired as well as one state, Virginia, for which the stay-at-home order has not yet expired. Moreover, for each state, we mark the date that the order started (circles) as well as the expiration date (squares). Some states show remarkable signs of economic recovery. For example, the number of visits to grocery and pharmacies in Montana on May 5 is higher than before the pandemic.

For all states, the recovery started before the expiration date. This suggests that news about lifting the policy may have acted as a positive signal for consumers and businesses. Consumers and businesses may have inferred that the risk of infection is low, thus reacting with increased participation in economic activity before the formal lifting of the stay-at-home order.

The Shape of the Economic Recovery

The COVID-19 pandemic resulted in one of the sharpest economic contractions in recorded history. The shape of the recovery (i.e., the time it takes for economic activity to go back to normal) is a question of active debate. In a V-shaped recovery, the economy returns to normal quickly. In a U-shaped recovery, the economy recovers at a slower pace. In an L-shaped recovery, the economy never fully recovers from the shock and stays permanently lower than the pre-crisis trend.

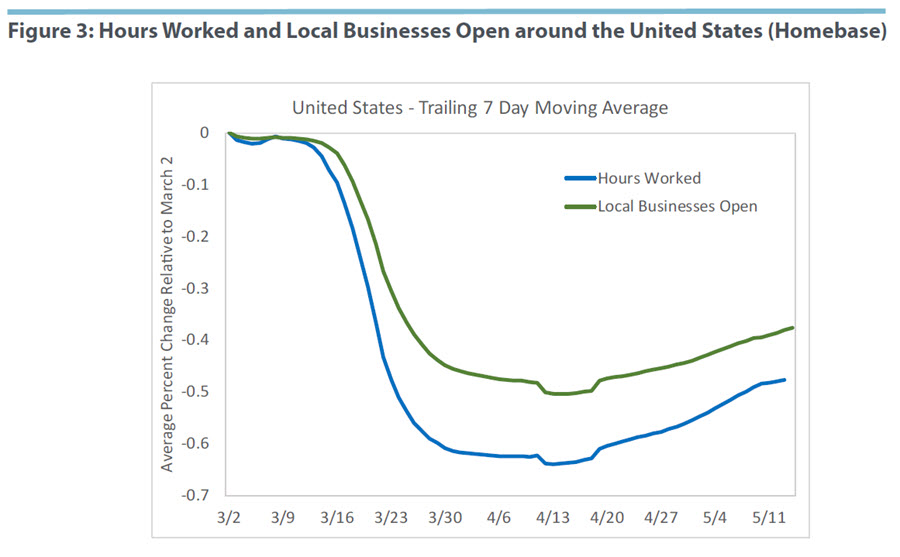

Figure 3 shows the population-weighted average change in hours worked and number of businesses open across the United States. (For each state, we follow the same approach as in Figure 1.) Both series reached the trough around April 15 and have been increasing during the last month. Relative to the trough, hours worked have increased by around 13 percentage points and the number of local businesses open increased by around 10 percentage points. Currently, it seems like the United States is experiencing either a V- or U-shaped recovery. At this pace, it will take four to five more months to reach the pre-COVID-19 levels of economic activity.

But there are valid reasons to expect a stronger rebound. First, as previously discussed, some states still have stay-at-home orders in place. Second, provided that there is no setback in terms of infection rates, consumers and workers may feel increasingly confident in the safety of economic activities and thus feel more willing to participate.

Marios Karabarbounis is an economist and Nicholas Trachter is a senior economist in the Research Department of the Federal Reserve Bank of Richmond.

2

Google does not elaborate on how exactly this index is constructed, perhaps because it is used for an online product provided by Google (called Popular Times). Once Google constructs the daily index for each destination, it compares it to a baseline index based on the median for the mobility index, for the same day of the week, during the five-week period from Jan. 3, 2020 to Feb. 6, 2020. Homebase follows a similar approach.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.