The Rising Tide of Large Ships

In 1988, a new class of container ships, the American President Lines (APL) C-10, came on the market — the first class of ships that was too large to pass through the Panama Canal. Eighteen years later, in 2006, the Panama Canal Authority began a multiyear project to expand the canal so that these and other large ships will be able to make the passage between the Atlantic and Pacific oceans.

The expansion of the Panama Canal, expected to reach completion in late 2015, heralds much-anticipated shifts in the routes that goods take to arrive at their final destinations in the United States. This is because larger ships, up to double the size of those that can transit the Panama Canal today, will be able to navigate the canal once its new locks are opened. From the growing markets of Northeast Asia, Southeast Asia, and the Indian subcontinent, the first leg of the journey for most traded goods is the long maritime trip from overseas ports to U.S. ports on the East Coast, the West Coast, and the Gulf of Mexico. In particular, container shipments to East Coast ports, which include the ports of the Fifth District, may increase, particularly with respect to goods arriving from Northeast Asia (China and Japan).

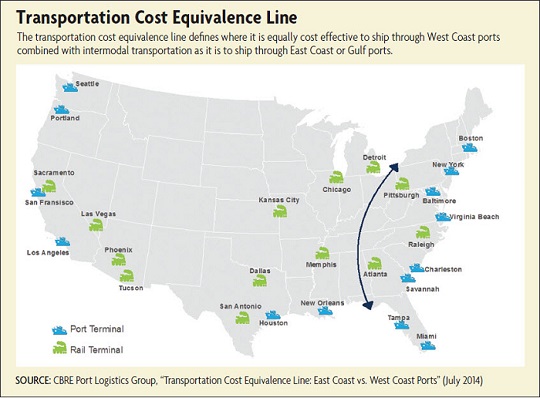

The opportunity for East Coast ports to gain from the expansion of the Panama Canal depends on many factors, not the least of which is the depth of their channels. Several East Coast ports, including Norfolk, Baltimore, and New York, have channels that are deep enough to accommodate the larger ships today; Charleston, S.C., can also handle them, though only at high tide. But the Panama Canal project will not be the only source of growth for these ports. Larger ships making their passages through the Suez Canal, the other primary route for Asian trade, are already calling at East Coast ports that can accommodate them. The expansion of the Panama Canal may accelerate this trend, but the use of big ships is already well under way.

Waterborne Trade is Growing

Merchandise trade between the United States and the rest of the world is expected to more than double between 2012 and 2040, according to estimates from the Federal Highway Administration’s Freight Analysis Framework. Over this period, imports are expected to grow at a compound average annual growth rate of 2.9 percent, while exports will grow even faster, by 3.9 percent.

With this growth will come growth in oceangoing freight. Measured by volume, the majority of U.S. trade is carried on oceangoing vessels, with the exception of trade with Canada and Mexico, which is transported mostly by truck or rail, or by water via the Great Lakes. Among U.S. major trading partners, imports from China are expected to grow faster than those of any other region of the world; nearly all trade with China is transported by water. Indeed, the push for shipping lines to use larger ships has been motivated by China’s growing trade with the United States, Europe, and other regions of the world. Because waterborne shipping is so critical to the movement of goods from China to the United States, the Panama Canal expansion will have its greatest potential effect on this aspect of U.S. international trade, primarily by increasing volume in the trade route from Northeast Asia to the East Coast.

Ships are Getting Bigger

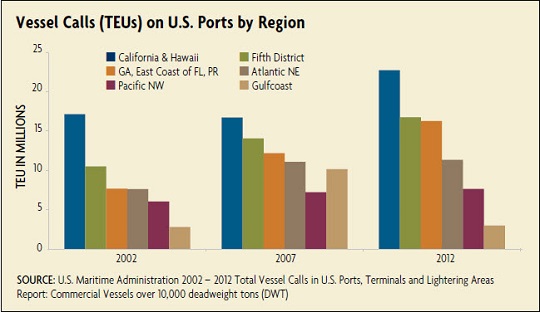

In 2011, nearly 84 percent of oceangoing commodity trade between Northeast Asia and the United States was containerized. This has not always been the case, though. Since the inception of containerized cargo transport in the mid-1950s, the use of containers and dedicated container-carrying ships has grown dramatically, with clear cost advantages for many types of cargo that had previously been shipped by breakbulk methods, requiring each item to be loaded individually. In addition to the reduced cost of handling and avoidance of potential vandalism or waste, the use of intermodal containers allows for delivery of smaller shipments directly to customers via transfer to truck or rail. (See "The Voyage to Containerization," Region Focus, Second/Third Quarter 2012.) Initially, containers were used primarily for manufactured goods, but starting in the 1980s, certain agricultural products also switched to the containerized mode of shipment. From 2002 to 2012, the number of container vessel calls at U.S. ports rose by 16.6 percent. During this time, Fifth District ports saw an increase in container vessel calls of 11.7 percent. (See chart.)

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us