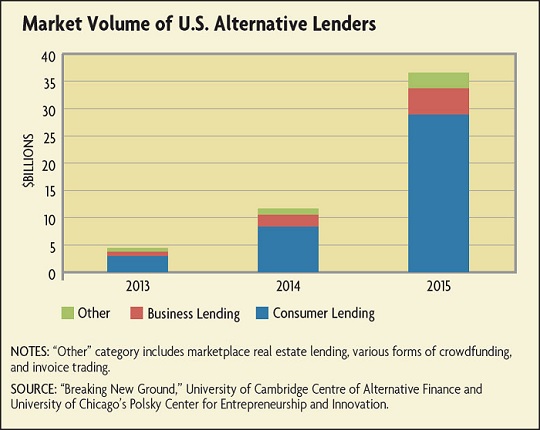

This growth has been driven by both supply and demand factors. On the demand side, consumers and small-business owners are attracted to the ease of use and variety of options offered by alternative lenders. On the supply side, these firms claim to gain a cost and speed advantage over traditional lenders by forgoing physical branches and using advanced algorithms to instantly analyze huge swaths of new consumer data. Additionally, alternative lenders present a new opportunity for investors hoping for higher returns in a low interest rate environment.

But with expansion has come questions. Do these firms enjoy an advantage over traditional firms because of new methods and technology or because they have avoided costly financial regulations and oversight? As this sector has grown and evolved, financial regulators like the Office of the Comptroller of the Currency (OCC), the Treasury Department, the Federal Deposit Insurance Corporation (FDIC), and the Fed have begun asking in earnest: What opportunities and risks do these firms present for consumers, traditional lenders, and the financial system as a whole?

A Marketplace for Loans

Alternative lenders began with a simple, and old, idea: connect savers with borrowers. The challenge lies in convincing savers to lend money to strangers when the latter know more about their likelihood of repaying than the former. Traditionally, banks have served as middlemen for these transactions. Savers make deposits that become the bank's liabilities. The deposits are federally insured, alleviating the need to worry about repayment. Banks use those deposits to fund loans, taking on the burden of assessing borrowers' risk so that savers don't have to. Banks then earn a profit on the spread between the interest they charge borrowers and the risk-free interest they pay depositors.

Many of the new online lenders connect savers and borrowers in a more direct way. Borrowers that come to Prosper or rivals like Lending Club are offered loan terms based on their credit history and other factors. Once approved to appear on the platform, these loans are listed on the site and investors can choose to invest in portions of any number of loans. Those savers earn a return based on the performance and riskiness of the loan, while the lending firm earns a fee from matching the two parties and facilitating the transaction. This peer-to-peer or marketplace lending draws on the power of the crowd, similar to funding websites like Kickstarter that pool hundreds of individual small-dollar donors to fund a big project.

Not all alternative lenders follow the same model, though. "Balance sheet" lenders like OnDeck, a leading alternative lender to small businesses, are much closer to traditional banks. They hold a significant portion of their loans on their own balance sheet and earn revenue from the performance of those loans. Investors hold stock in OnDeck rather than investing in individual loans.

While they have been billed as disruptors to banks, the similarities of some of these online platforms to traditional players somewhat belies that image. In fact, many alternative lenders depend on traditional institutions to originate their loans. Borrowers that apply for a loan from Lending Club, for example, actually receive a loan from a brick and mortar bank (WebBank in Salt Lake City, Utah, which partners with several online lenders). By having a bank originate the loan, marketplace lenders can piggyback on its charter without obtaining one of their own. The bank then sells the loan to the alternative lender after a few days, which in turn securitizes the loan for sale to its investors.

Still, online lenders have innovated on the traditional underwriting model by looking at more than just credit scores. Alternative lenders say they analyze borrowers' social media accounts, educational histories, and online commerce sales at Amazon or eBay to glean more information not captured by traditional metrics. In theory, this information leads to a more accurate risk assessment of borrowers, allowing alternative lenders to price riskier loans more profitably and lower-risk loans more competitively than traditional lenders. Additionally, since individual investors rather than the firm bear the risk of the loans, marketplace lenders can hold less capital against their loans compared to traditional banks, further reducing their operating costs and passing those savings on to borrowers.

In recent years, online lenders have attracted funding from large institutional investors. For example, in 2010, Lending Club's investor base was entirely composed of individuals. By 2015, that number had shrunk to just 20 percent, with institutional investors and individuals acting through an investment vehicle or managed account making up the rest. Low loan losses and interest rates have attracted investors seeking solid returns, according to a 2015 report on the sector by Goldman Sachs.

This increase in investor participation is in part thanks to provisions in the Jumpstart Our Business Startups Act of 2012. "More people are eligible to invest in startups now in a broader way," says E.J. Reedy, a senior fellow at the University of Chicago's Polsky Center. "At the same time, you've got consumers that are more used to dealing with online platforms and are not as tied to a traditional bank branch. And you also have advances in algorithms and other technologies to provide scoring on loan applications. All of these things coming together have allowed for this kind of surge to happen."

Filling the Gaps

By analyzing new sources of consumer data, these firms may be able to reach new consumers and businesses that have been underserved by traditional financial firms. At least, that's the hope.

But for the most part, the typical borrower at an alternative lender looks a lot like the typical borrower at a traditional bank. For example, 80 percent of Prosper's loans are to borrowers with high credit scores, according to a 2016 study by the Treasury Department. What is drawing these individuals to online lenders rather than banks? According to surveys, borrowers rate the speed and ease of use of these new lenders relative to traditional banks very highly. This is particularly true among younger borrowers, who, according to a 2015 survey by Morgan Stanley Research, were most likely to have used or heard of alternative lenders. Price seems to be another draw. Morgan Stanley found that as much as 85 percent of marketplace loans to consumers are being used to refinance some form of existing debt, suggesting that borrowers are able to get better rates refinancing their debt with these new lenders.

Indeed, many alternative lenders have built their businesses on being able to identify low-risk borrowers better than traditional lenders. SoFi began in 2011 as a platform for alumni of Stanford University's Graduate School of Business to make loans to current students of the program. Today, its main service is providing student loan refinancing options to recent graduates from any accredited university or graduate program. Loans from the Department of Education carry the same terms for all students. SoFi advertises better rates for students who are employed with a steady income and who can demonstrate good financial history.

While having additional options is certainly beneficial to creditworthy borrowers, what about those who have historically fallen through the cracks? A growing number of startups are targeting these borrowers as well. LendUp, a San Francisco-based firm, recently raised funding to provide credit cards to less creditworthy borrowers. Additionally, alternative lenders have targeted small-businesses owners who have had trouble obtaining credit from banks. Traditionally, small businesses have relied on local community banks for loans, but the number of community banks has been falling steadily for decades. (See "Who Wants to Start a Bank?" Econ Focus, First Quarter 2016.) Both small and large banks have pulled back from making smaller loans in general since they carry the same costs as larger loans but fewer profits.

"The problem is that those are the loans that most small businesses want," says Karen Mills, a senior fellow at Harvard Business School and the former administrator for the Small Business Administration under President Barack Obama.

Part of the recent tightening of credit by traditional lenders was driven by uncertainty immediately following the financial crisis of 2007-2008. But while banks slowly loosened lending standards during the recovery, the July survey of senior loan officers on bank lending practices conducted by the Federal Reserve Board of Governors shows tightening again for large- and small-business lending. In a 2014 paper on the state of small-business lending with Brayden McCarthy (now a vice president at online lending marketplace Fundera), Mills argued that this retrenchment reflects structural impediments on traditional lenders. And in addition to the costs to banks for making smaller loans, there are costs to businesses for going the traditional route.

"The theory is you sit down with your banker and go over what kind of loan you need, and that's how you get the loan that's right for you," says Mills. "The problem is that it's a very cumbersome process that requires big time commitments for the small-business owner." Moreover, a business owner may have to go through that process multiple times to get the funds they need. According to the Fed's 2015 Small Business Credit Survey, only about half of businesses that applied for a loan from a bank received all the money they applied for.

Balancing Access and Protection

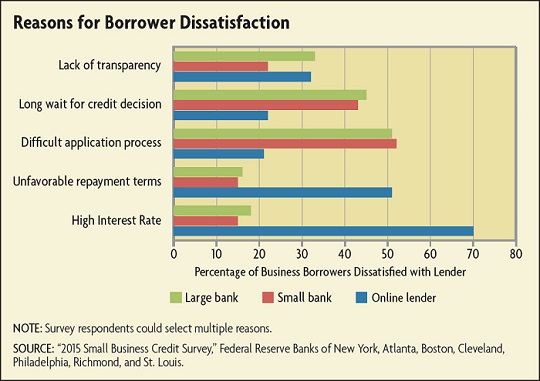

While creditworthy borrowers have enjoyed savings by refinancing debt through alternative lenders, others have been less satisfied with the rates they've received. Of the 20 percent of firms in the Fed's Small Business Credit Survey that applied for loans from online lenders, more than 70 percent were approved for some credit. But those approved firms were on the whole unsatisfied with the high interest rates and repayment terms of their loans. (See chart below.) According to the Treasury's 2016 study, rates on consumer loans from online lenders can range anywhere from 6 percent to 36 percent annually based on the borrower's credit rating, compared to about 10 percent to 12 percent annually for a bank loan or credit card. Small-business loans at online lenders ranged anywhere from 7 percent to a whopping 98 percent annually in one case.