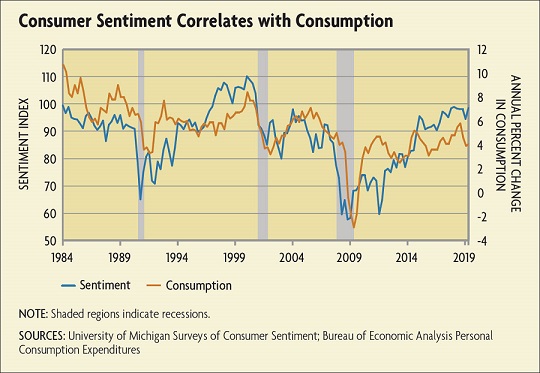

Talking Ourselves into a Recession

{kind=link}

{kind=link}

{kind=link}

But as economists are fond of saying, correlation does not necessarily mean causation. Identifying causal links between mood and the market is tricky. That's because there may be some other factor influencing changes in both.

"You have to find things that are correlated with sentiment but not with economic fundamentals," says Jess Benhabib of New York University.

In a 2019 article, Benhabib and his co-author Mark Spiegel of the San Francisco Fed identified presidential election results as a clean way to measure the effects of changes in sentiment. They reasoned that voters who backed the winning candidate would be more optimistic about the future than voters who chose the loser. To proxy for voter party affiliation, they used the party affiliation of each state's congressional representatives. After controlling for other variations between states, Benhabib and Spiegel found that economic activity increased in states with more representatives from the same party as the winning presidential candidate.

Another study used data from an Australian consumer sentiment survey that also asked respondents about their voting intentions. Like Benhabib and Spiegel, the authors of that study found that election results had an effect on consumer sentiment that spilled over into consumption behavior. Voters who backed the winner were more likely to go out and make big purchases, like buying a car, than voters who backed the losing candidate.

Of course, it is possible that election results have a direct effect on the economy as well, which would make it unsuitable for isolating the causal effects of sentiment. Benhabib and Spiegel cite evidence that election results don't appear to be related to changes in local economic outcomes based on political support. But it is hard to fully disentangle the effects. Still, Benhabib argues that recent recessions provide additional evidence of the direct role that sentiment plays in driving economic activity.

"When you look back in history, there are downturns in the economy where it is hard to identify a fundamental shock as the cause," he says.

Beliefs and Business Cycles

One downturn that seems hard to explain without sentiment is the 1990-1991 recession. Real business cycle theory, which became the de facto way of understanding movements in the overall economy in the 1980s, argues that recessions are caused by shocks to fundamental factors in the economy, such as productivity. Writing in the American Economic Review in 1993, Robert Hall of Stanford University looked for such a shock to explain the 1990-1991 recession but couldn't find one.

Our Related Research

"Survey Data and Subjective Beliefs in Business Cycle Models." Working Paper No. 19-14, September 3, 2019.

"Sentiment Analysis of the Fifth District Manufacturing and Service Surveys," Economic Quarterly, Third Quarter 2019.

"Learning About Consumer Uncertainty from Qualitative Surveys: As Uncertain As Ever," Working Paper No. 15-09, August 2015.

"Rather, there seems to have been a cascading of negative responses during that time, perhaps set off by Iraq's invasion of Kuwait and the resulting oil-price spike in August 1990," Hall wrote. "Consumers responded to the negative forces as they would to a permanent decrease in their resources."

Olivier Blanchard, now at the Peterson Institute for International Economics, came to similar conclusions at the time. "In contrast to its predecessors, this recession does not have an obvious proximate cause," he wrote in a 1993 article.

Roger Farmer of the University of Warwick in England has spent much of his career developing explanations for how changes in sentiment can drive shifts in the business cycle. In his models, there are many different configurations in which the economy could settle, and changes in sentiment — particularly peoples' feelings about the stock market — drive the economy toward one equilibrium rather than another. For example, when stock market values are high for extended periods, people feel wealthier and more optimistic about the future. This leads them to spend and invest more, fueling a boom in the economy. But when people begin to feel less confident about the future, their doubts can become a self-fulfilling market crash.

"That's not to say fundamental events aren't important," Farmer says. "It's possible that changes in sentiment are the result of people looking ahead and seeing a bad event down the road. They foresee a change in fundamentals, and then the market crashes as a result of what they foresee. But if you accept that explanation, then you have to explain how the collapse of Lehman Brothers in 2008 was a response to some new information that the economy was going to be very bad in the next decade."

Benhabib agrees, arguing that if the Great Recession of 2007-2009 were simply the result of a fundamental shock, the economy should have adjusted quickly and settled into a new equilibrium. Something else must be contributing to the length and severity of downturns, and for researchers like Farmer and Benhabib, that something else is sentiment.

There are even examples of times when a burst of optimism seems to have shortened recessions that economists expected to be much worse. In his book, Shiller described how many economists and policymakers expected a severe economic downturn after the Sept. 11, 2001, terrorist attacks. The U.S. economy was already in the midst of a recession that had begun in March of that year following the dot-com stock market crash. Shiller wrote that there were "widespread fears that the recession in the U.S. economy would be prolonged because people would choose to stay at home owing to their fear of another such attack."

Instead, the recession ended just two months later, making it one of the shortest in American history. Shiller attributed this sharp turnaround in part to a change in national sentiment. He argued that the public resolved to defy the attackers by carrying on with life as normal.

Episodes like the 1990-1991 recession, the post-9/11 recovery, and the Great Recession are suggestive of the power of sentiment to shift the economy.

"Pessimistic expectations can generate recessions," says Benhabib. "Optimistic expectations can generate booms."

A Biased View

Another way of defining sentiment is as irrational biases or beliefs that color peoples' expectations for the future. Some people may be inherently optimistic or pessimistic, and this bias affects their economic decisions.

In a 2019 working paper, Anmol Bhandari of the University of Minnesota, Jaroslav Borovička of New York University and the Minneapolis Fed, and Paul Ho of the Richmond Fed found evidence of these types of biases in survey data on consumer sentiment. Households consistently overestimated future unemployment and inflation, and these pessimistic biases became even more pronounced during recessions. Bhandari, Borovička, and Ho found that this variation in pessimism accounts for a large fraction of business cycle fluctuations, particularly changes in employment.

They also found that an increase in pessimism causes people to behave as if they expect negative productivity shocks in the future. Pessimistic households consume less and save more. Pessimistic firms expect lower productivity and higher costs, leading them to demand fewer workers, which contributes to higher unemployment.

Like the models developed by Benhabib and Farmer, the work of Bhandari, Borovička, and Ho shows how changes in sentiment can ripple through the economy as a shock. Their research also shows that even if changes in sentiment don't initiate movements in the economy, they can amplify them. In another 2019 paper, George-Marios Angeletos and Chen Lian of the Massachusetts Institute of Technology called this feedback mechanism a "confidence multiplier," a reference to the Keynesian idea of spending multipliers.

"As output and real returns fall, consumers and firms become pessimistic about the future, which in turn feeds into a further drop in aggregate spending and output, a further drop in confidence, and so on," Angeletos and Lian wrote.

Through a Glass Darkly

Just as people may not always make decisions that are fully rational, consumers and business leaders don't have full information about what is happening across the economy at any given time. Thus, another way that sentiment can influence the economy is by shaping how people fill in the blanks of incomplete information.

"I would classify businesses as being overly optimistic when they think they will sell more of their product than they would think if they knew the entire state of the economy," says Kristoffer Nimark of Cornell University. "Their belief isn't driven by irrational behavior; it's driven by the fact that they have only a partial idea of what's going on."

In his research, Nimark observed that in order for changes in sentiment to drive changes in the whole economy, many people would need to become either more optimistic or more pessimistic at the same time.

"It can't be the case that a few individuals are randomly more optimistic or less optimistic than everyone else," he says. Something needs to coordinate peoples' beliefs about the economy, and according to Nimark, the news media plays that role.

In Nimark's models, people make rational decisions based on the information they have, but their information about the economy is incomplete. Households and businesses might know about conditions in the fields they work in, but they know little about other sectors of the economy. Because people have limited time to gather information about the rest of the economy, they outsource this task to the news media. But even if the media reports the news accurately, Nimark argues that its coverage of the economy, too, is incomplete.

"The news media focuses on sectors where the most interesting or newsworthy things are happening," he says. In a 2014 article, he refers to the saying in journalism that "dog bites man" is not news but "man bites dog" is. The news media has a natural incentive to cover sectors of the economy that are experiencing the most dramatic fluctuations, even if those sectors are not necessarily representative of the economy as a whole. This can give households and businesses that receive these news reports a skewed perception of economic conditions, contributing to what Nimark calls "man-bites-dog business cycles."

In more recent work with Ryan Chahrour of Boston College and Stefan Pitschner of Uppsala University, Nimark applied this model to the Great Recession. They found that roughly three-quarters of news coverage about the economy in 2009 was devoted to stories about the car industry and the financial sector, which were undergoing the biggest upheavals at the time.

"If you actually look at what was going on in other sectors at the same time, things were not that bad," says Nimark. "But since everyone received the information from the news that the car industry and financial sectors were doing very badly, everyone became more pessimistic."

In effect, the news coordinated peoples' beliefs about the overall economy. Even if businesses knew that conditions were not as bad in their sector, they couldn't assume that others in the economy knew that because that information wasn't being reported. According to Chahrour, Pitschner, and Nimark's calculations, the existence of news media generates fluctuations in economic output that are more than four times as large as predicted by a model with no news media.

"You need news media, or something like it, to present a partial picture of the economy in order to generate the strong recession we saw in 2009," says Nimark.

Reaching Hearts and Minds

Trying to disentangle the ways in which sentiment interacts with the economy is a bit like trying to answer the age-old question about the chicken and the egg.

Economists may never really know the answer. But there is enough research to suggest that sentiment does play a role in shaping the business cycle, whether it is acting as a type of nonfundamental shock, through peoples' irrational biases, or in reaction to incomplete information. The question facing policymakers is what to do about it.

Benhabib says that statements from policymakers to manage expectations could be helpful for avoiding a sentiment-driven slump.

"Of course, such statements have to be credible in order to work," Benhabib says.

Nimark echoes this idea. Just spreading good news that isn't true isn't going to turn the economy around.

"What I think policymakers could do is monitor what gets reported in the news and compare that to what they think is the real state of the economy," he says. "Central banks spend a lot of time monitoring different sectors of the economy. If they notice that what is getting attention in the media is unrepresentative of what's really going on, then it might be worthwhile emphasizing that in publications and speeches."

Since the Great Recession, the Fed has vastly increased the amount of information it provides on the economy in the form of press conferences, speeches, and forecasts in an effort to make both its policy decisions and its assessment of economic conditions more transparent.

"We need to recognize communication as a monetary policy transmission channel," Richmond Fed President Tom Barkin said in a May 2019 speech. When confidence is waning, he said, "it's our job as policymakers to try to support it."

Readings

Benhabib, Jess, and Mark M. Spiegel. "Sentiments and Economic Activity: Evidence from U.S. States." The Economic Journal, February 2019, vol. 129, no. 618, pp. 715-733. (Article available with subscription.)

Bhandari, Anmol, Jaroslav Borovička, and Paul Ho. "Survey Data and Subjective Beliefs in Business Cycle Models." Federal Reserve Bank of Richmond Working Paper No. 19-14, Sept. 3, 2019.

Chahrour, Ryan, Kristoffer Nimark, and Stefan Pitschner. "Sectoral Media Focus and Aggregate Fluctuations." Manuscript, Oct. 22, 2019.

Farmer, Roger E. A. "Animal Spirits, Financial Crises and Persistent Unemployment." The Economic Journal, May 2013, vol. 123, no. 568, pp. 317-340. (Article available with subscription.)

Shiller, Robert J. Narrative Economics: How Stories Go Viral and Drive Major Economic Events. Princeton, N.J.: Princeton University Press, 2019.