The dollar has been the global currency of choice for nearly a century, but in light of recent U.S.-led financial sanctions, some wonder whether that status will endure

Econ Focus

Second Quarter 2022

The world runs on the U.S. dollar. Apart from Europe, where the euro dominates, the majority of global trade is invoiced in dollars. The Fed estimates that foreign investors held nearly $1 trillion in cash at the end of the first quarter of 2021, roughly half of all U.S. notes in circulation. Central banks around the world hold about 59 percent of their foreign currency reserves in dollars. Much of these reserves are held as dollar-denominated debt — that is, U.S. Treasuries — rather than currency. About a third of all U.S. debt was held abroad as of 2021, and a little over 60 percent of debt issued by non-U.S. companies in a foreign currency was denominated in dollars.

The widespread adoption of the dollar as a global currency has long been thought of as a source of "exorbitant privilege" for the United States, a term coined in the 1960s by France's then Finance Minister Valéry Giscard d'Estaing. Having a large share of trade invoiced in dollars protects U.S. exporters and importers from exchange rate risk. And insatiable global demand for U.S. Treasuries enables America to service its more than $30 trillion in federal debt at favorable interest rates.

The dollar's dominance abroad also grants the United States increased leverage against other countries through financial sanctions. In response to Russia's invasion of Ukraine in February, the United States and its allies froze about half of the $630 billion of foreign reserves held by Russia's central bank and barred several major Russian banks from SWIFT (the Society for Worldwide Interbank Financial Telecommunication), an international messaging system used for interbank transfers. Because of the dollar's commanding role in international trade and finance, limiting who can access dollar banking and payment services represents a potent weapon in the U.S. arsenal.

But some worry that weaponizing the dollar in this way could diminish its role in the world economy by driving other countries to seek alternatives. Although the dollar is still the dominant global currency by a wide margin today, there is some evidence that its future could be in jeopardy.

Becoming a Hegemon

Library of Congress Prints & Photographs Division, LC-D4-19762

The U.S. dollar solidified its rise to global prominence after the Bretton Woods Conference in 1944, held at the Mount Washington Hotel in New Hampshire (seen here). The final agreement fixed the dollar to gold and tied other countries’ currencies to the dollar.

When trying to understand how the dollar became the international currency of choice, many people focus on the global financial system that was built in the aftermath of World War II. In July 1944, representatives from 44 nations met in Bretton Woods, N.H., to design a framework for rebuilding the world's economy after the war. The final agreement was that the United States would fix the value of the dollar

to gold at $35 an ounce and other countries would peg their currencies to the dollar. This system enshrined the dollar as the most important currency in the world, requiring other countries to hold dollars in reserve to maintain their exchange rate.

But the Bretton Woods system didn't last long. By the 1970s, the United States didn't have enough gold to back all the dollars held abroad at the agreed upon rate of $35 an ounce, and President Richard Nixon ended gold convertibility for the dollar. (Belgian-born Yale University economist Robert Triffin had predicted this exact problem more than a decade earlier by pointing out that supplying the dollars needed to maintain the dollar's status as the global reserve currency would eventually conflict with domestic policy priorities, a tension that became known as the Triffin dilemma.)

After the collapse of Bretton Woods, other countries were no longer obligated to fix their currencies to the dollar, and many economists anticipated that the dollar's role abroad would diminish. Instead, in the decades following the end of Bretton Woods, the dollar became even more globally dominant.

The dollar wasn't the first currency to attain global reach, though. In the 16th century, the Spanish silver dollar rose to prominence through Spain's colonial expansion. In the 17th century, Dutch florins and bills issued by the Bank of Amsterdam became the currency of choice. And by the 18th century, the pound sterling of the British Empire had become dominant — a position it would maintain into the 20th century. Each of these global currencies emerged organically without coordination as in Bretton Woods. In fact, the dollar had already begun to compete with the British pound by the mid-1920s, years before Bretton Woods solidified its place.

Global currencies arise for much the same reasons as domestic ones — they fulfill the basic functions of money. That is, they act as a medium of exchange, unit of account, and store of value. In terms of exchange, a currency can become dominant if it is cheaper to use in trade than any other currency. For instance, historically it has been true that when exchanging one currency for another, it was often cheaper to use the dollar as an intermediary because the market for dollars was much bigger. A currency becomes a global unit of account when it is widely used for trade invoicing. And safe and liquid currencies can become global stores of value.

Economists have different theories about which of these functions is most important for explaining a currency's rise, but First Deputy Managing Director of the International Monetary Fund (IMF) Gita Gopinath and Harvard University professor and former Fed Governor Jeremy Stein argue that they are all interconnected and reinforcing. In a 2021 Quarterly Journal of Economics article, they outlined a theory of how a currency can become dominant through positive feedback loops. If a currency becomes a global unit of account through its use in trade invoicing, that increases the demand to hold that currency to conduct trade, which bolsters its position as a global store of value. Similarly, if there is a lot of global demand to hold a currency as a store of value, that reduces the cost of borrowing in that currency and makes it attractive for traders in other countries to price exports in that currency to access that cheap funding market.

Privilege and Responsibility

Does the dollar's widespread use abroad confer an "exorbitant privilege" upon the United States as Giscard d'Estaing claimed? Most economists agree that it has its benefits, though not many would say they qualify as exorbitant.

The law of supply and demand implies that higher global demand for dollar-denominated Treasuries means the United States can attract buyers at lower interest rates, allowing it to borrow more cheaply. But in practice, this advantage appears slight. In a 2016 post on his Brookings Institution blog, former Fed Chair Ben Bernanke noted that the real interest rate the United States pays on its debt is the same or even slightly higher than the interest paid by other similarly creditworthy countries such as Germany and Japan.

And this benefit comes with a cost, which Pierre-Olivier Gourinchas of the University of California, Berkeley, and Hélène Rey of the London Business School call the "exorbitant duty" of the United States to provide insurance to the rest of the world. In a 2022 working paper, they argued that other countries effectively pay an insurance premium to the United States in good times, allowing it to earn an excess return on its net foreign asset position. In exchange, the United States acts as insurer during global crises. Gourinchas and Rey estimated that the United States transferred the equivalent of roughly 20 percent of U.S. GDP to the rest of the world during the 2007-2009 financial crisis.

"At the core, the international monetary system is set up for the production and distribution of safe assets," explains Matteo Maggiori, a professor of finance at Stanford University who has studied the dollar's role in the global economy. "The U.S. has been at the core of that system for the last century and enjoyed some benefits, but the rest of the world has also benefited by being able to buy the safe assets it desired."

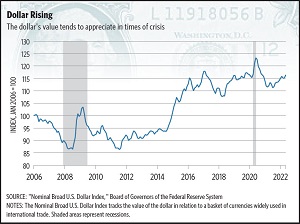

Treasuries are viewed as safe assets because the dollar tends to appreciate during times of crisis. Indeed, even amid present-day concerns about the dollar's future, it has strengthened during the recent uptick in global uncertainty, as it did in similarly turbulent times in the past.(See chart.)

This is an encouraging vote of confidence in America's future, but it can also harm the competitiveness of U.S. exporters at a time when they are already hurting. Currency depreciation can provide economic stimulus by making a country's exports more attractive. Serving as the safe asset supplier to the world means essentially giving up that advantage.

Some researchers have argued that the fact that the dollar has been stronger over time than it would have been if it were not the global currency of choice has contributed to the long-run decline of U.S. manufacturing by hurting its competitiveness with the rest of the world. Joseph Gagnon of the Peterson Institute for International Economics says that the strong demand for the dollar and dollar-denominated assets is the biggest driver of the United States' persistent trade deficit.

Another benefit of the dollar's central role in international trade and finance is the leverage it grants the United States over other countries. Since so much of global trade and finance happens through dollars, the ability to block individuals, companies, and even governments from operating in that system represents a serious threat. According to the Global Sanctions Data Base, constructed by a team of economists, the United States has gradually increased its reliance on financial sanctions over the past 70 years. But could the use of this power ultimately undermine the dollar's reputation as safe and secure?

Competition for the Crown?

One of the recent sanctions that garnered a lot of attention was the decision to bar several Russian banks from SWIFT. Many commentators referred to this as the financial "nuclear option," since it effectively cut those banks off from much of the global financial system. Because many of the transfers that use SWIFT are made in dollars, some feared this action could spark a negative backlash against the dollar. But as Richmond Fed economist Russell Wong discussed in a March Economic Brief, the dollar and SWIFT aren't directly related. SWIFT is just a messaging system open to any currency. So, while being banned from SWIFT might prompt some banks to seek alternative messaging systems, it wouldn't necessarily drive them to different currencies.

Wong compared SWIFT to Gmail as a system for sending emails, while analogizing currencies to the language those emails are written in. If Google banned some Gmail users from sending messages in English, Wong suggests that those users would be more likely to look for a different email system than to abandon English. This analogy illustrates the challenge of substituting away from the dollar: There simply isn't any comparable alternative.

"The dollar represents the entire ecosystem of payments and banking," says Wong. "It is difficult to find a close substitute that is equally deep, liquid, broad, and safe."

Most competitor currencies face limitations that the dollar does not. The euro is widely used for trade in Europe and is viewed as safe, but the fact that the eurozone does not have a unified fiscal policy limits its ability to produce enough euro-denominated safe assets to satisfy global demand. Plus, as the recent actions against Russia illustrate, switching to the euro would not necessarily offer any additional protection over the dollar, as Europe and the United States often work in partnership.

China has taken steps to internationalize the renminbi in recent years by opening its financial markets up to more foreign investors, but Maggiori says it still has a long way to go to match the openness of the U.S. market. In a recent working paper with Christopher Clayton of Yale University and Amanda Dos Santos and Jesse Schreger of Columbia University, Maggiori argued that China was slowly opening itself up to build a "reputation as a country capable of providing the global store of value."

"The road toward the renminbi becoming an international currency is a difficult one that will take some time and face its inevitable setbacks," says Maggiori.

And while the use of financial sanctions by the United States may prompt some countries to try to diversify away from the dollar, others have argued that it could actually strengthen the dollar's appeal overall. In a recent NBER working paper, Michael Dooley of the University of California, Santa Cruz and David Folkerts-Landau and Peter Garber of Deutsche Bank argued that part of the role of the provider of the world's dominant reserve currency is to police the global financial system and sanction misbehavior.

"The U.S. administration is probably betting that the controls imposed on Russia will not be perceived as arbitrary, but as proportionate retaliation on a country waging aggressive war," says Maggiori.

The Long View

While there may not be a single obvious replacement for the dollar, that doesn't mean that countries haven't been diversifying into other currencies. The dollar's share of global foreign exchange reserves fell to a 25-year low at the end of 2020, to 59 percent from 71 percent in 1999.

Serkan Arslanalp and Chima Simpson-Bell of the IMF and Barry Eichengreen of the University of California, Berkeley, referred to this development in a recent IMF working paper as "the stealth erosion of dollar dominance." The dollar isn't being replaced on bank balance sheets by another single currency like the euro or renminbi, they found. Rather, most of the shift away from dollars has been into dozens of smaller currencies. They cited a greater desire for portfolio diversification on the part of central banks as well as the falling cost of transacting in smaller currencies as factors that have contributed to this change. This has led some economists to speculate that we could be heading toward a "multipolar" world of many different competing currencies, which could have some advantages.

"Just like biodiversity makes for a more robust global ecology, a multipolar system will be more robust," says Eichengreen. "In addition, an expanding global economy needs additional international liquidity to grease the wheels of globalization, and the U.S. can't provide the requisite safe and liquid assets all by itself."

Indeed, many economists point to a new kind of Triffin dilemma as a greater risk to dollar supremacy than the use of sanctions. Just as the United States faced a crisis of confidence in its ability to back the dollars in circulation during the Bretton Woods era, economists have warned that it could face a similar challenge in the coming years to supply enough safe assets to meet global demand while simultaneously maintaining confidence in its ability to repay its debts. Having more options for safe assets to choose from in the form of different currencies could solve this problem, but not all economists agree that a multipolar system would necessarily be more stable. Competition among countries to grab the reserve currency crown could lead to coordination challenges and questions about which assets are truly safe.

Moreover, the transition from the dollar regime to its successor could be unstable. "One historical precedent is the coexistence of dollar and sterling during the interwar years," the late Harvard University macroeconomist Emmanuel Farhi told Econ Focus in a 2019 interview. "It's not a particularly happy precedent; it was a period of monetary instability. You saw frequent rebalancing of international portfolios into one reserve currency and out of another, which created a lot of volatility."

History teaches that dominant currencies change infrequently and often over long transition periods. But crises can be the catalyst for those transitions, as was the case when the British pound's centuries-long reign started to unravel after World War I. While almost no economist predicts that the dollar will be replaced soon, market confidence is fickle, and the types of crises that spark a changing of the reserve currency guard are inherently hard to predict.

READINGS

Arslanalp, Serkan, Barry Eichengreen, and Chima Simpson-Bell. "The Stealth Erosion of Dollar Dominance: Active Diversifiers and the Rise of Nontraditional Reserve Currencies." IMF Working Paper No. 22/58, March 2022.

Clayton, Christopher, Amanda Dos Santos, Matteo Maggiori, and Jesse Schreger. "Internationalizing Like China." Manuscript, March 2022.

Farhi, Emmanuel, and Matteo Maggiori. “A Model of the International Monetary System.” Quarterly Journal of Economics, February 2018, vol. 133, no. 1, pp. 295-355.

Gopinath, Gita, and Jeremy C. Stein. "Banking, Trade, and the Making of a Dominant Currency." Quarterly Journal of Economics, May 2021, vol. 136, no. 2, pp. 783-830. (Article available with subscription.)

Gourinchas, Pierre-Olivier, and Hélène Rey. "Exorbitant Privilege and Exorbitant Duty." Centre for Economic Policy Research Discussion Paper No. DP16944, January 2022. (Article available with subscription.)

Taylor, Timothy. “Some Economics of Dominant Currencies.” Conversable Economist blog, May 3, 2022.