How Broad-Based Is the Recent High Inflation?

Economic Brief

September 2021, No. 21-30

PCE inflation has been high from March through July. Much commentary has emphasized the contributions of a few extremely large price increases. This Economic Brief provides graphical descriptions of the recent contributions of large price increases to inflation. We then evaluate those recent contributions against their behavior over the last 25 years of low and stable inflation. We find that inflation has been somewhat higher than what one would have predicted based on the past relationship between the contributions of the largest price increases and inflation.

U.S. inflation has been unusually high this spring and summer. In fact, it's been 40 years since we've seen inflation like this: The annualized PCE inflation rate over the period March through July was 6.5 percent, the highest five-month rate since the period ending November 1981.

Federal Reserve policymakers and commentators alike have noted that especially large price changes for a small fraction of consumption expenditures (for example, used cars) can account for much of the recent jump in inflation. This raises the possibility that real factors affecting supply and demand for particular goods and services are in fact causing the high inflation numbers. If this is true, inflation will normalize when those real factors dissipate, reducing the need for the Fed to adjust its monetary policy.

In this Economic Brief, I quantify the extent to which large price increases for a small number of goods and services account for high current inflation. I also provide historical context by comparing current metrics to their behavior over the past 25 years of stable inflation. That comparison yields a mixed message: Large price increases have indeed accounted for an unusually high fraction of some of the recent monthly inflation rates, but price increases in July — when inflation fell but was still above the Fed's target — were relatively broad-based.

Background on PCE Inflation and Related Metrics

The Fed targets PCE inflation as its inflation measure. PCE inflation is the rate of change in the price index for personal consumption expenditures and is calculated from price changes for hundreds of categories of goods and services inflation.

Since 1995, PCE inflation has averaged 1.9 percent (near the Fed's target 2 percent average) and has been relatively stable. At an annual rate, the interquartile range for monthly inflation is between 0.7 percent and 3.3 percent.

Even with overall inflation being relatively stable for such a long period, price changes for individual consumption categories have varied considerably. For example, the monthly inflation rate in February 2015 was exactly 2 percent at an annual rate, yet a quarter of consumption categories had annualized price increases of more than 4 percent, and a quarter had annualized price decreases of more than 2 percent.1

As long as inflation is stable near the Fed's target, wide dispersion in price changes across categories has little relevance for monetary policy: Supply and demand factors vary from one category to another and from one month to another, and these factors are reflected in relative price changes that show up as variation in nominal price changes across categories.

However, when inflation moves (significantly) above or below the Fed's target, attention understandably turns to the distribution of price changes across categories. In those situations, the Fed needs to decide whether to adjust its policy. A hypothetical case in which there were equal increases in the rates of price change for every consumption item would generate more alarm bells for policy than if there were an extremely large price change for only one consumption item, with typical price changes for all other items.

Reality is more complicated. There are always some items that make disproportionate contributions to inflation, and various adjusted inflation measures have been developed for removing these items from the inflation calculation. Two well-known adjusted measures are core inflation and trimmed mean inflation:

- Core inflation excludes food and energy prices because they have historically been especially volatile.

- Trimmed mean inflation — calculated by the Dallas Fed — excludes a fixed percentile of expenditures with the highest and lowest price changes.2

The decompositions in this article are motivated by the same facts and ideas as core inflation and trimmed mean inflation. However, they come at the issue from the other direction: Instead of adjusting inflation to eliminate the contributions of large price changes, they focus on the size of those contributions.

Decomposing Inflation

We use data from the Bureau of Economic Analysis on more than 300 consumption categories to approximate PCE inflation each month. This approximation is calculated as an expenditure-share-weighted average of price changes for the component categories of consumption, where the expenditure shares are for the month prior to the price changes.3

Although this formula does not perfectly reproduce actual PCE inflation, the approximation is generally quite close, and it has the benefit of allowing for simple decompositions for our analysis.4

For each month, we rank the consumption items from highest percent price change to lowest, then use the corresponding expenditure shares to calculate two measures:

- The cumulative contribution to inflation

- The cumulative share of inflation

We plot the entire "distribution" of the cumulative contributions and cumulative shares for the March-July period as functions of the corresponding cumulative expenditure shares. The historical comparisons will instead involve two statistics:

- The contribution to inflation of the 5 percent of expenditures with the largest price increases

- The share of expenditures with highest price increases that accounts for half of the inflation rate

The Distribution of Price Changes in Recent Periods

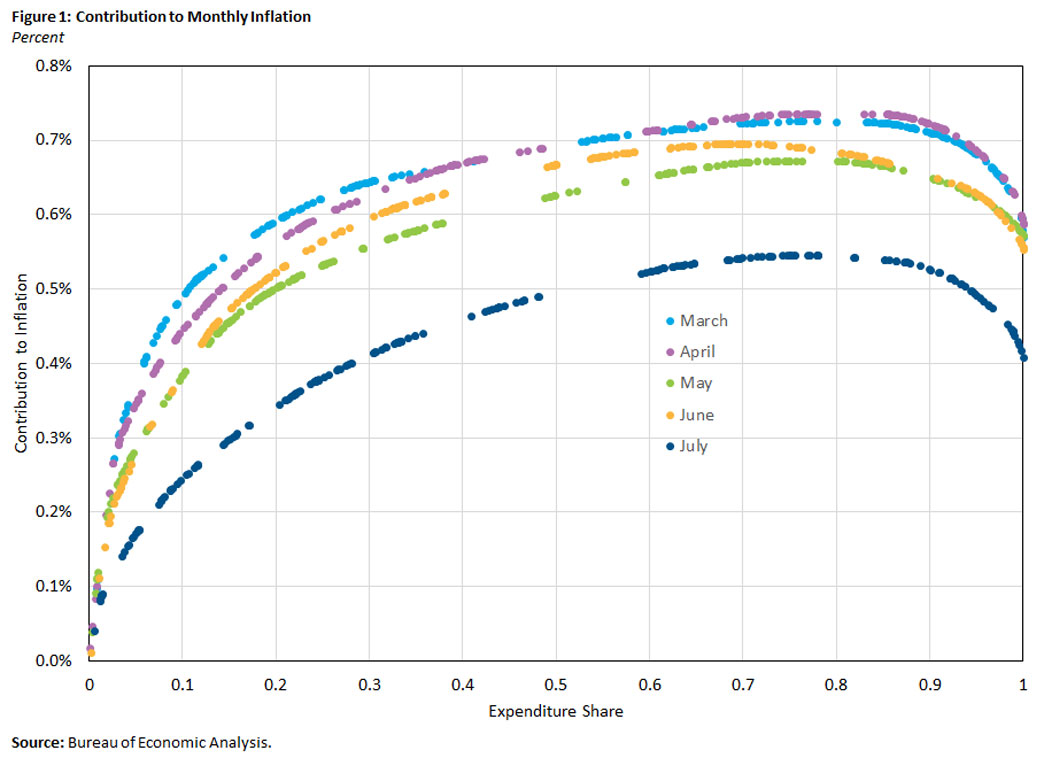

Figure 1 displays the cumulative contributions to inflation for March through July. With items ranked in decreasing order of percent price change, the horizontal axis represents the cumulative share of expenditures, and the vertical axis represents the cumulative contribution to inflation. The level of each line at expenditure share 1.0 is the monthly inflation rate: approximately 0.4 percent for July and above 0.55 percent for March through June.

Note that in each of the five months, items that account for more than 20 percent of expenditures experienced price decreases. In March, for example, this is evident from the fact that the light blue line is decreasing for expenditure shares above 0.76.

The most important aspect of Figure 1 for our purposes is the behavior of the lines close to expenditure share zero, which are the items with the largest price increases. By construction, this is the steepest part of each curve, as the slope of the curve at any point is approximately the rate of price change for the item added at that point, and items are added in decreasing order of price change.

While the slope has to be weakly decreasing in the expenditure share, its steepness near zero depends on the dispersion in price changes. In an extreme case where all price changes were identical, the line would be straight with its slope equal to the inflation rate.

Focusing on the one-tenth of expenditures with the highest price changes, we see from Figure 1 that their contribution to inflation has fallen markedly from the March through June period (when it averaged above 0.4 percent) to July (when it was less than 0.25 percent). The same qualitative behavior applies to the lower expenditures shares with higher price changes.5

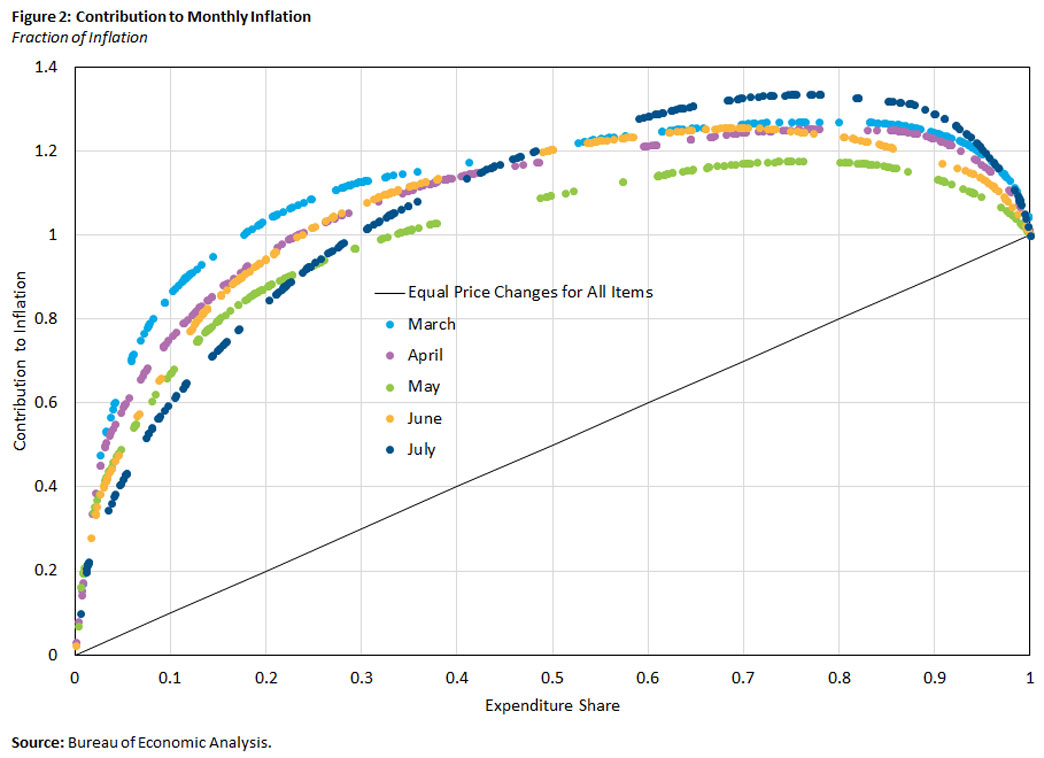

Figure 1 shows that inflation decreased in July and that the decrease was accompanied by a sharp decrease in the contributions to inflation from the largest price changes. Figure 2 uses the same data but plots the contributions to inflation as a share of that month's inflation rate, so that each line ends at 1.0 instead of at that month's inflation rate.

If rates of price change were identical across items, the line would be straight with slope 1 (the black line in the figure). The expenditure share where the line for a given month has slope 1 is the share of expenditures with a rate of price change higher than that month's inflation rate.

From Figure 2, we see that the largest price changes accounted for a smaller share of inflation in July than in the previous four months. For example, the 5 percent of expenditures with the largest price increases accounted for 42 percent of the July inflation rate, compared to between 48 percent and 60 percent of the inflation rates in March through June.

On one hand, this is consistent with the view that the high inflation readings this year have been driven by large relative price changes: As those large relative price changes became less prevalent in July, inflation also declined.

On the other hand, while inflation indeed declined in July, it was nonetheless well above the Fed's 2 percent target: The 0.4 percent rate is equivalent to a 5 percent annualized rate.

The last several months' data are not informative about whether a small fraction of large relative price changes may account for the fact that inflation was still well above target in July. For some insight into that question, we turn to a longer time series of historical data.

Time Series of Summary Statistics

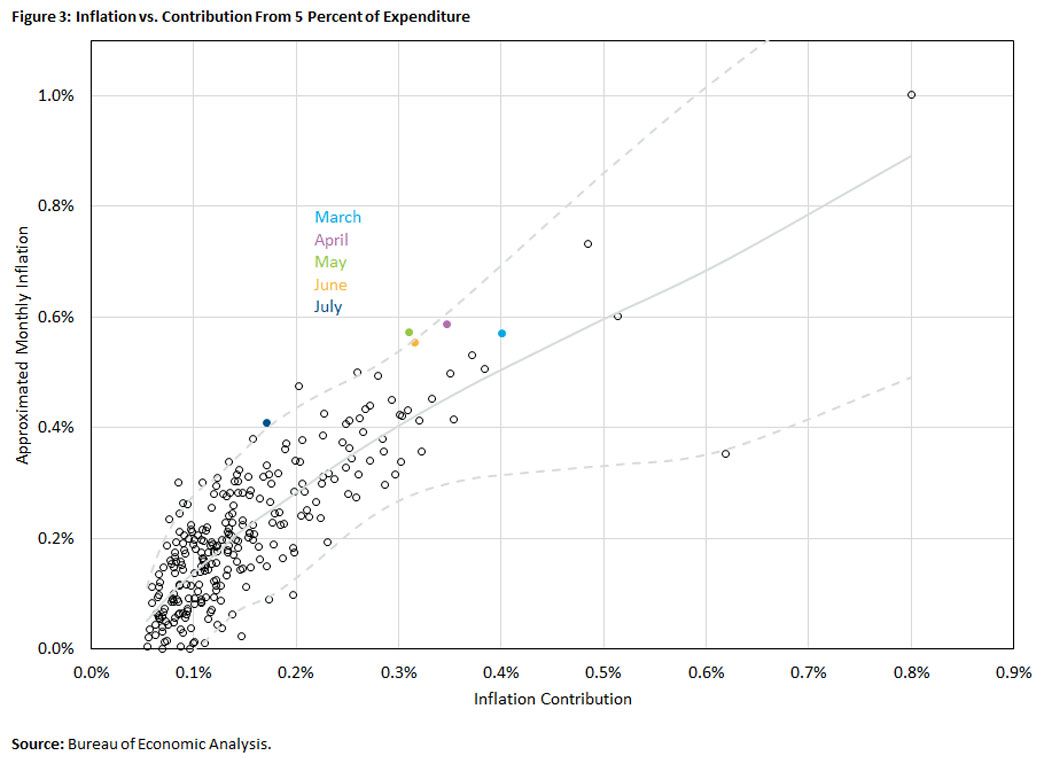

Figures 3 and 4 display scatter plots of monthly inflation and two statistics whose recent values can be read off of Figures 1 and 2, respectively:

- For Figure 3, we take the contribution to inflation of the top 5 percent of price increases from Figure 1.

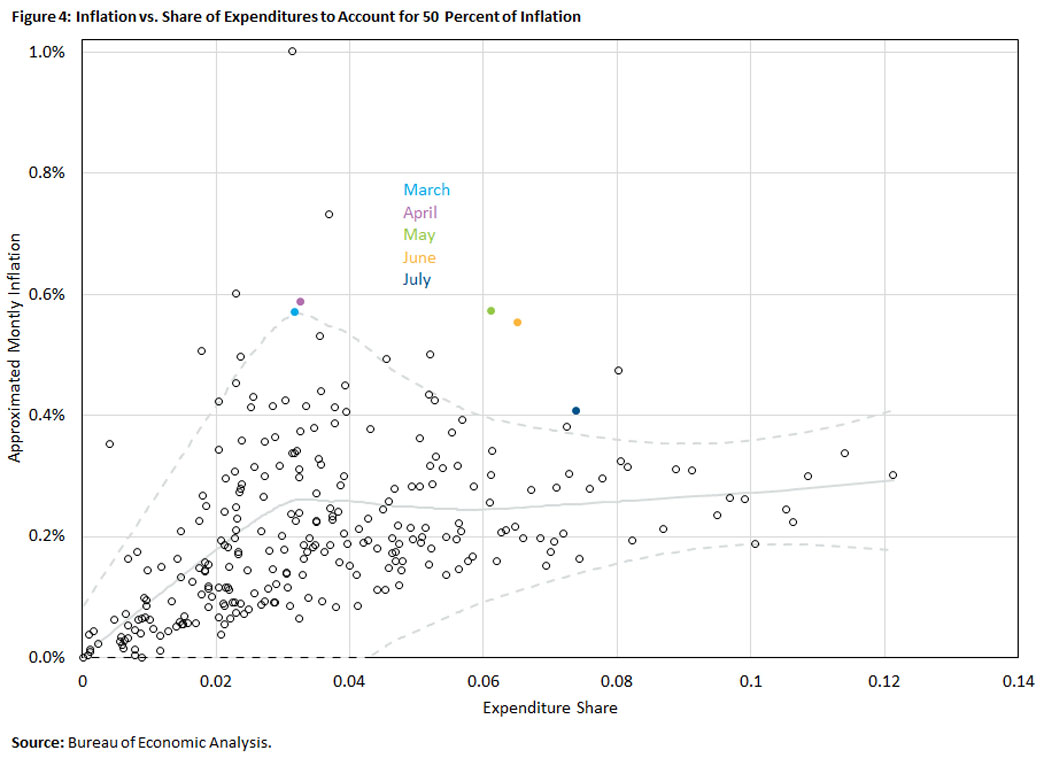

- For Figure 4, we take the share of expenditures that account for 50 percent of the monthly inflation rate from Figure 2.

The starting date for the figures is 1995 because, as discussed above, inflation has been stable around 2 percent from 1995 to the present. Each figure contains points only for months with positive inflation.6 The colored solid dots in Figures 3 and 4 denote the months from March through July. The solid gray line is a smooth curve (known as a loess curve) fit to data through February 2021, and the dashed gray lines show a 95 percent prediction interval.

The graphs serve two purposes:

- They indicate whether the recent data are unusual based solely on the contribution to inflation of large price changes.

- To the extent that there is a systematic relationship between inflation and the distributional statistics, the figures may reveal whether recent data follow the same relationship: Inflation has been stable since 1995, and we want to know if that stability appears intact.

Figure 3 plots the monthly inflation rate on the vertical axis against the contribution to inflation (measured in percent) of the 5 percent of expenditures with the largest price increases. Referring to Figure 1, this contribution is approximately 0.4 percent for March and 0.17 percent for July.

The first thing to note from Figure 3 is that the large price changes in March contributed more to inflation than in all but four other months since 1995. The contributions for April, May and June were lower, but still in the 95th percentile. In contrast, the July contribution of top price changes was more typical, within the interquartile range.

Next, note that there is a systematic positive relationship between inflation and the contribution of the top 5 percent of expenditures by price increase, with correlation of 0.84.

It is not at all surprising that inflation tends to be higher when the largest price increases are higher. What is interesting is how the recent data fits or does not fit within that established relationship. For example, March 2021 — while extreme in terms of both the level of inflation and the contribution of the largest price increases — fits well within the established relationship.

April through July are less clear: While they aren't dramatic outliers, in each case there have been no previous occurrences (after 1995) of such high monthly inflation rates with such small contributions of the largest price increases. Even though the contributions of large price increases have been substantial (apart from July) relative to other months in the sample, those contributions have been small relative to months with similarly high inflation. If inflation were to move up persistently, we would expect the points in Figure 3 to shift upwards. The fact that recent observations lie on the upper edge of the past relationship provides some tentative evidence of a more persistent upward shift in inflation.7

Figure 4 plots the monthly inflation rate on the vertical axis against the share of expenditures with highest price increases that account for half of the monthly inflation rate. Referring to Figure 2, this expenditure share is approximately 0.075 for July and 0.03 for March and April.

Interpreting Figure 4 is tricky, because months with very low inflation can easily have a tiny share of expenditures account for half of the inflation rate. However, as the expenditure share accounting for 50 percent of inflation rises above 0.05, the relationship becomes tighter.

It is notable that the monthly inflation rates lie outside that 95 percent prediction interval for May through July. That is, according to the historical relationship plotted in Figure 4, the expenditure shares accounting for 50 percent of inflation in May through July have typically been associated with lower inflation rates. In that sense, inflation in May through July has been relatively broad-based.

Conclusion

When inflation is stable, it fluctuates in part because of unusual real shocks to supply and demand for particular consumption items. Such shocks represent the leading explanation for the high monthly inflation rates since March of this year. In this Economic Brief, we quantified the accounting contributions to inflation of items with the largest price changes and investigated how these contributions compare to the period since 1995 over which inflation has been low and stable.

The contributions to inflation of the highest price increases were indeed large from March through June of this year, when monthly inflation rates were especially high. Monthly inflation fell in July, but to a level that was still above the Fed's 2 percent inflation target. And in July, large price increases no longer played an outsized role in accounting for inflation.

If a similar pattern appears in the coming months, it would represent tentative evidence that the increase in inflation is a more persistent phenomenon that reflects monetary factors and will not dissipate without an adjustment to monetary policy. This sort of evidence can complement more traditional methods of inferring the stance of monetary policy, such as estimates of the gap between the policy interest rate and the natural rate of interest.

Alexander L. Wolman is a vice president in the Research Department of the Federal Reserve Bank of Richmond.

1

These calculations are based on the narrowest publicly available breakdown of PCE categories, with sample starting in February 1995. The results are qualitatively robust to higher levels of aggregation.

2

In my 2011 paper "K-Core Inflation," I propose an alternative trimmed mean which removes items based on the size of their relative price change rather than their location in the distribution.

3

For the equations used to approximate PCE inflation, cumulative contribution to monthly inflation and cumulative share of monthly inflation, please see our appendix.

4

My 2011 paper "K-Core Inflation" and Todd Clark's 1999 paper "A Comparison of the CPI and the PCE Price Index (PDF)" provide explanations of how actual PCE inflation is calculated.

5

Consistent with the headlines, much of the sharp change in July relative to earlier months is accounted for by used cars. They represent approximately 1.6 percent of expenditures, and their price index fell 0.2 percent in July after increasing 7 percent per month, on average, from March through June.

6

While we could calculate the statistics for months with deflation, the interpretation would be different, and the comparisons with recent months would be complicated and not particularly interesting.

7

Note that the Dallas Fed trimmed mean PCE inflation rate has also moved up in recent months: The annualized monthly rate was 3.2 percent in July and has averaged 2.7 percent since March.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us