Are Firms Factoring Increasing Inflation Into Their Prices?

Economic Brief

March 2022, No. 22-08

While inflation is low and stable, business leaders are well justified in paying little attention to aggregate inflation measures when making their own pricing decisions. In this article, we introduce a new set of quarterly questions in a business survey that help to ascertain the extent to which firms pay more attention to inflation measures as inflation rises. We find that, from July 2021 to January 2022, business leaders not only report paying more attention to aggregate inflation measures, but also report incorporating those measures into their own pricing decisions.

"Price stability is that state in which expected changes in the general price level do not effectively alter business or household decisions." — Alan Greenspan

Inflation expectations play a central role in theories of inflation and monetary policy. In particular, the more inflation expectations become reactive to actual inflation readings, the harder it is for the monetary authority to stabilize inflation without provoking a recession.1 For the past few decades, business leaders would have been well justified in ignoring aggregate inflation measures when making pricing decisions, given that those measures have been low and stable relative to other factors affecting firms' costs. However, the recent increased inflation may have led firms to factor inflation into their own pricing decisions.

We infer firms' attention and reactiveness to current inflation numbers from a regional survey on firm expectations. To do this, we introduce a survey-based measure for studying the relationship between aggregate inflation measures and firms' expectations for their own costs and prices. We have conducted three waves of the quarterly survey: July 2021, October 2021 and January 2022.

Taken together, these waves suggest that CEOs and other business leaders are increasingly incorporating aggregate measures of inflation (such as CPI or PCE) into their decision-making and price/cost expectations. Although aggregate inflation measures are still not paramount in firms' price setting, the share of firms that report taking inflation into account when setting prices has been rising steadily.

Fifth District Surveys of Business Activity

The Federal Reserve Bank of Richmond has surveyed CEOs and other business leaders across the Fifth Federal Reserve District for almost 30 years.2 The survey includes around 200-250 responses per month. The survey panel underweights the smallest firms and — due to the history of the survey as well as the broad relevance of manufacturing to the Fifth District economy — manufacturing firms make up about one-third of responses even though they make up a much smaller share of establishments in both the Fifth District and the nation.3

In addition to questions about variables such as demand, employment and prices, respondents are often asked a set of ad hoc questions. Here, we focus on a set of questions asked during the waves mentioned above. These questions covered the extent to which respondents pay attention to aggregate inflation measures and how much they account for those measures when projecting costs and setting prices.

The Importance of Aggregate Measures of Inflation

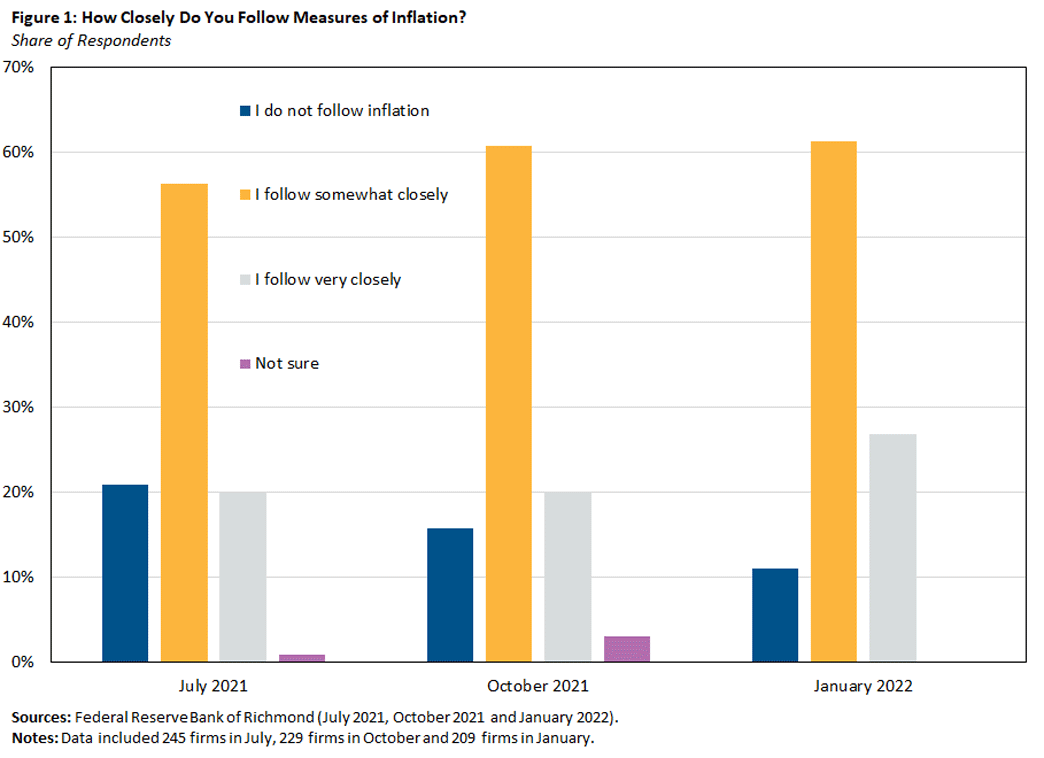

The first question gauges how closely participants follow aggregate inflation measures. We found that the share of firms that follow inflation went up notably over the six months, as seen in Figure 1.

In July, 21 percent of respondents reported not following inflation measures at all. By January, that share was down to 11 percent. At the same time, the share of respondents who reported following inflation measures very closely went up from 20 percent to nearly 30 percent.

Therefore, while it is still true that many firms do not follow inflation very closely,4 the shift in these numbers suggests that firms might be paying more attention after months of the highest aggregate inflation numbers in decades.

Incorporating Inflation Measures Into Pricing

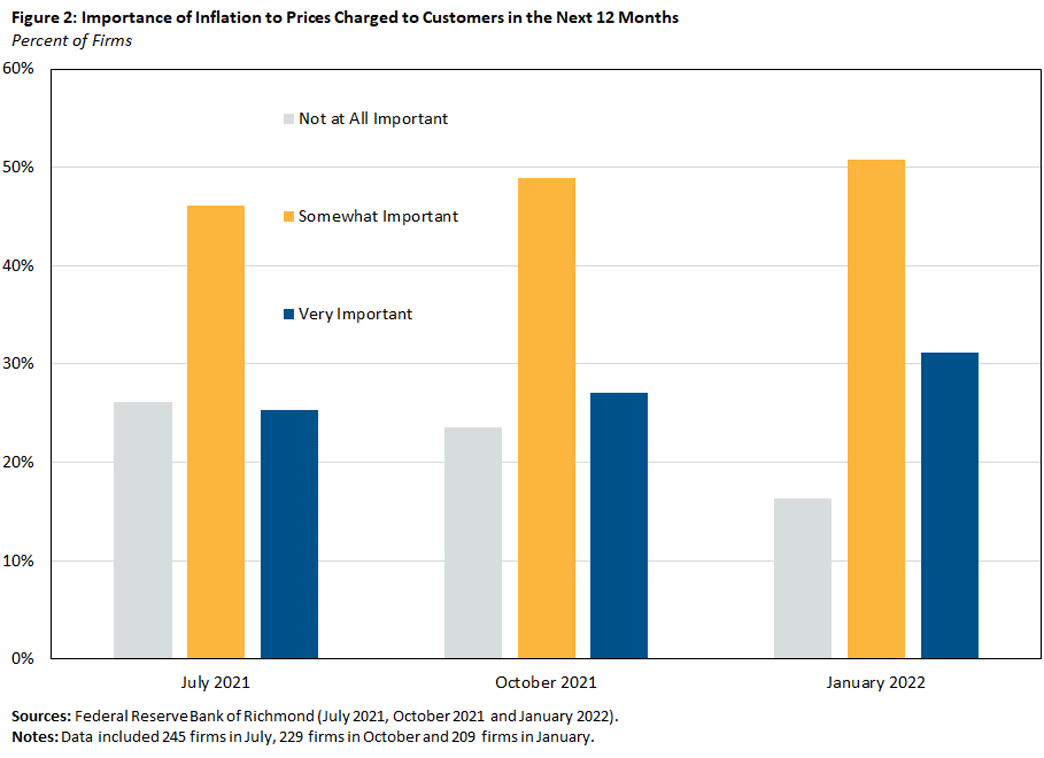

We then inquired whether firms were factoring measures of inflation into their own pricing decisions. When we asked how important inflation was when setting the prices they charge, we found that the share of firms who responded "somewhat" or "very" important rose from July to January, as seen in Figure 2.

Only 26 percent of firms in July and 27 percent of firms in October reported that aggregate inflation measures were "very important" when setting expectations about prices that they will charge. That number rose to 31 percent in January. And by January, only 16 percent of firms said that aggregate measures of inflation were "not at all important" in their price setting, down from 26 percent in July.

Conclusion

This analysis uses a new approach in an old survey to gauge the importance of aggregate inflation measures for firms' thinking about their own price growth. CEOs' historic inattention to inflation and inflation targets has, somewhat paradoxically, created a benign environment for monetary policy, where price-setting was little affected by inflation outcomes. This inattention to inflation was rational to the extent that prices were stable, generating a virtuous feedback loop where stable inflation engenders stable pricing decisions.

To the extent that inflation stays high, CEOs will naturally pay more attention to aggregate inflation measures, thus raising the stakes for the FOMC's communication with price-setters, perhaps even once the high inflation has abated. The readings from our survey suggest that some of that may be happening over the course of the last six months.

We thank Jason Kosakow for assistance in survey design and implementation.

Felipe Schwartzman is a senior economist and Sonya Ravindranath Waddell is a vice president and economist in the Research Department of the Federal Reserve Bank of Richmond.

1

Inflation expectations play a central role in economic models of those decisions through, for example, an expectations-augmented Philips curve (as seen in the 1968 address "The Role of Monetary Policy (PDF)"), sticky price models (summarized, for example, in the 2003 book "Interest and Prices" ) and imperfect information models (for example, the 2002 paper "Sticky Information versus Sticky Prices: A Proposal to Replace the New Keynesian Phillips Curve" and the 2021 paper "Dynamic Rational Inattention and the Phillips Curve"). A common theme among many macroeconomic models is that inflation expectations are central to understanding the link between the nominal and real sides of the economy and therefore play a fundamental role in determining the nature of optimal monetary policy. On how inflation expectations can become "deanchored" and reactive to inflation data, see the 2021 working paper "Anchored Inflation Expectations." On what this implies to monetary policy, see the 2021 working paper "Monetary Policy and Anchored Expectations: An Endogenous Gain Learning Model."

2

The Fifth District is comprised of the District of Columbia, Maryland, North Carolina, South Carolina, Virginia and most of West Virginia.

3

Additional information about the Richmond Fed's business surveys can be found in our methodology document (PDF).

4

See, for example, the 2021 working papers "The Inflation Expectations of U.S. Firms: Evidence From a New Survey" and "Unit Cost Expectations and Uncertainty: Firms' Perspectives on Inflation."

To cite this Economic Brief, please use the following format: Schwartzman, Felipe; and Ravindranath Waddell, Sonya. (March 2022) "Are Firms Factoring Increasing Inflation Into Their Prices?" Federal Reserve Bank of Richmond Economic Brief, No. 22-08.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us