Building A Pipeline Between Producer and Consumer Prices

Economic Brief

September 2022, No. 22-38

Do rapidly rising producer prices signal pain ahead for consumers? We take a fresh look at the relationship between producer and consumer price indexes. We document a correlation between upstream producer prices and the Fed's preferred measure of consumer price inflation (the personal consumption expenditure price index). Using a statistical model, we find that that levels and growth rates of producer prices have a statistically significant impact on consumer price inflation. Gaps between the two price indexes tend to normalize over time, which, given recent data, suggests that upward inflationary pressures on consumers could persist.

With prices growing in 2021 at their fastest pace in decades, inflation has become a top concern for monetary policy. At his speech at this summer's Jackson Hole conference, Federal Reserve Chair Jerome Powell said, "The Federal Open Market Committee's (FOMC) overarching focus right now is to bring inflation back down to our 2 percent goal."

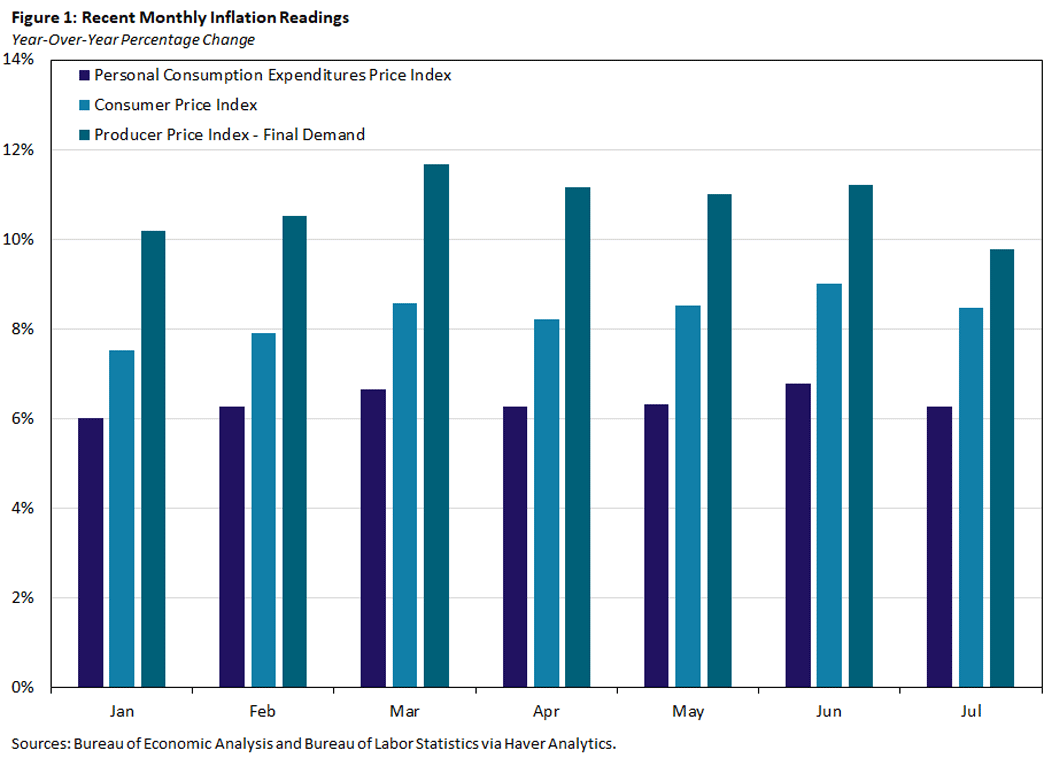

Driving this heightened vigilance, recent inflation readings have come in at levels not seen in about four decades. As of July:

- The one-month percent change in CPI remained constant after increasing 1.3 percent in June, making the year-over-year rate in July 8.5 percent.

- The personal consumption expenditures price index — which is the Fed's preferred price index — registered 6.3 percent on a year-over-year basis, more than triple the Fed's long-run average target of 2 percent.

- The producer price index (PPI) — which measures prices charged by U.S. businesses — has risen to a year-over-year rate of 9.7 percent.

Figure 1 shows recent year-over-year inflation rates for all three price indexes.

Although the Fed has formally adopted the PCE price index as the basis of its inflation target, the PPI continues to be closely watched as well. Movements in the PPI have long been viewed as reflecting pricing changes early in the pipeline, and some analysts believe that such upstream pricing changes could be an early signal of future movements in downstream consumer prices.

In practice, the relationship between the PPI and consumer price indexes has not always been clear. The 1995 study "Do Producer Prices Lead Consumer Prices? (PDF)" found only a weak relationship between changes in producer prices and subsequent changes in consumer prices, while another 1995 study, "The Commodity-Consumer Price Connection: Fact or Fable?," found that the predictive power of PPI for core CPI inflation weakened starting in the mid-1980s.

A more recent paper, the 2022 paper "On the Wedge Between the PPI and CPI Inflation Indicators," found that PPI and CPI co-moved strongly prior to 2000 but have since diverged, as globalization has driven a wedge between the baskets of goods that the two price indexes measure.

And PPI may be more informative for some sectors than others: For example, according to the USDA's Economic Research Service, industry-level PPIs for foods and feeds "have historically shown a strong correlation with the all-food and food-at-home CPIs."

In this article, we take a fresh look at the relationship between the PPI and consumer prices. While the previous research provides a strong starting point, it should be noted that the Bureau of Labor Statistics formally transitioned to a new method of calculating the PPI in 2014 that captures more parts of the U.S. economy, including services, construction, government purchases and exports. The studies cited above, meanwhile, use PPIs calculated under the old methodology.

The BLS's methodology for calculating the PPI formally captures the concept of a pricing pipeline. Known as the Final Demand-Intermediate Demand (FD-ID) system, PPI components are organized according to their stage of production, extending all the way to final demand:

- The FD portion tracks producer price inflation with respect to goods, services and construction sold as personal consumption, capital investment, government purchases and exports.

- The ID portion tracks producer prices for goods, services and construction sold to businesses as inputs to production.

For goods in particular, according to the BLS, the ID structure includes a "production flow" treatment of intermediate demand that organizes commodities into production stages "with the explicit goal of developing a forward-flow model of production and price change."

That said, extending the pricing pipeline concept from producer prices to consumer price indexes like PCE and CPI may be a stretch. For instance, the BLS gives three main reasons that PPI changes may not fully translate to changes in the CPI.

Index Composition

The composition of the set of goods and services included in each index is different. The PPI includes the entire marketed output of U.S. producers, including the prices of goods, services and construction products sold to other producers, as well as products sold for export and to government. In contrast, the CPI measures the prices of goods and services purchased for consumption by U.S. urban households, including the prices of imported goods, which are excluded from PPI.

Pricing Sources

The types of prices collected by each index are different. The PPI measures prices through revenues received by the producer. Sales and excise taxes are not reflected in the PPI, because they do not represent producer revenue. In contrast, the CPI measures prices through the out-of-pocket expenditures of consumers, which reflect sales and excise taxes.

Services Included

Several consumer services included in CPI are not included in PPI, including education services and residential rent. The PPI currently covers about 72 percent of services as measured by 2007 census revenue, and efforts to expand services coverage further are ongoing.

Linkage Between Consumer Price and PPI Growth Rates

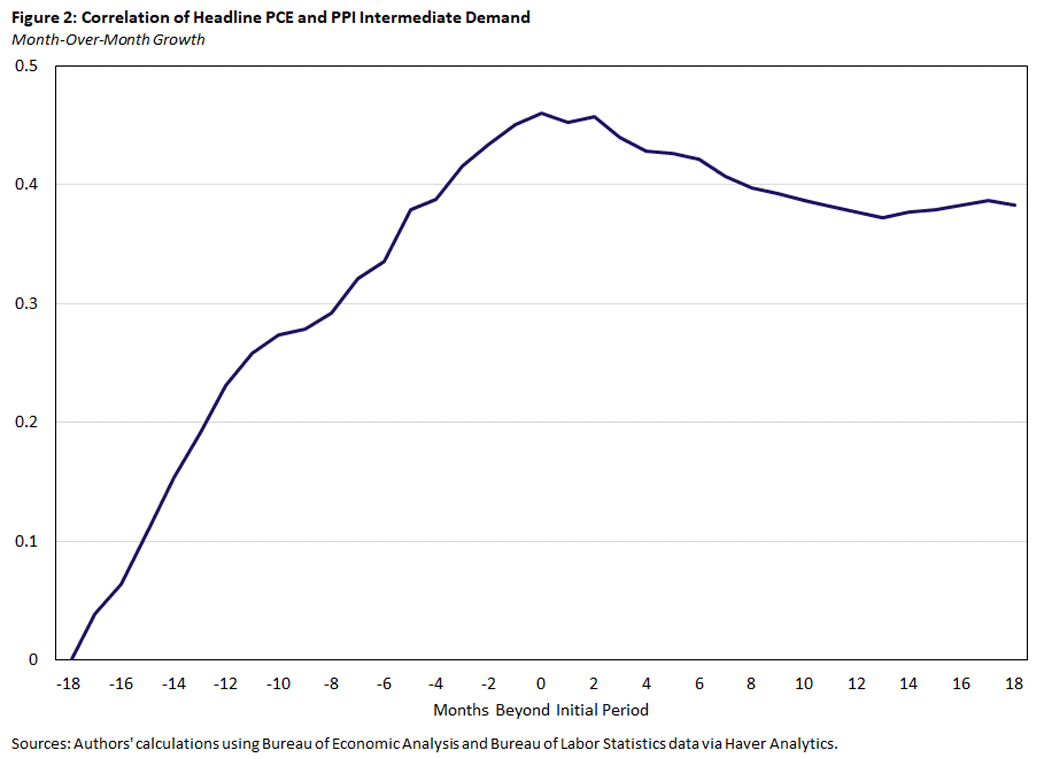

Having been duly warned to temper our expectations, we proceed in our attempt to find a linkage between consumer prices and the PPI. Because our analysis is motivated by the pricing pipeline concept, our results will focus on the longer pipeline from the PPI for (Stage 4) intermediate demand, extending to the PCE price index. Presumably, if a relationship exists across this longer pricing pipeline, there will also be relationship across the shorter segment of the pipeline that extends from the PPI for final demand to consumer prices. In the analysis that follows, when we refer to "the PPI" and "PPI inflation," we refer to the PPI for intermediate demand.

For our first exercise, we examine the correlation between past and future monthly values of month-over-month PPI inflation and month-over-month PCE inflation in the current month. Our results are shown in Figure 2, which shows that the strongest correlation is between the current month's PCE and PPI inflation readings, at about 0.46.

However, we also see a considerable positive correlation between lagged values of monthly PPI inflation and the current month's inflation. In particular, the correlations between current monthly PCE inflation and previous months' PPI inflation up to seven months back are all greater than 0.3. This is our first clue that PPI inflation contains information for future changes in the PCE price index.

Price Index Levels

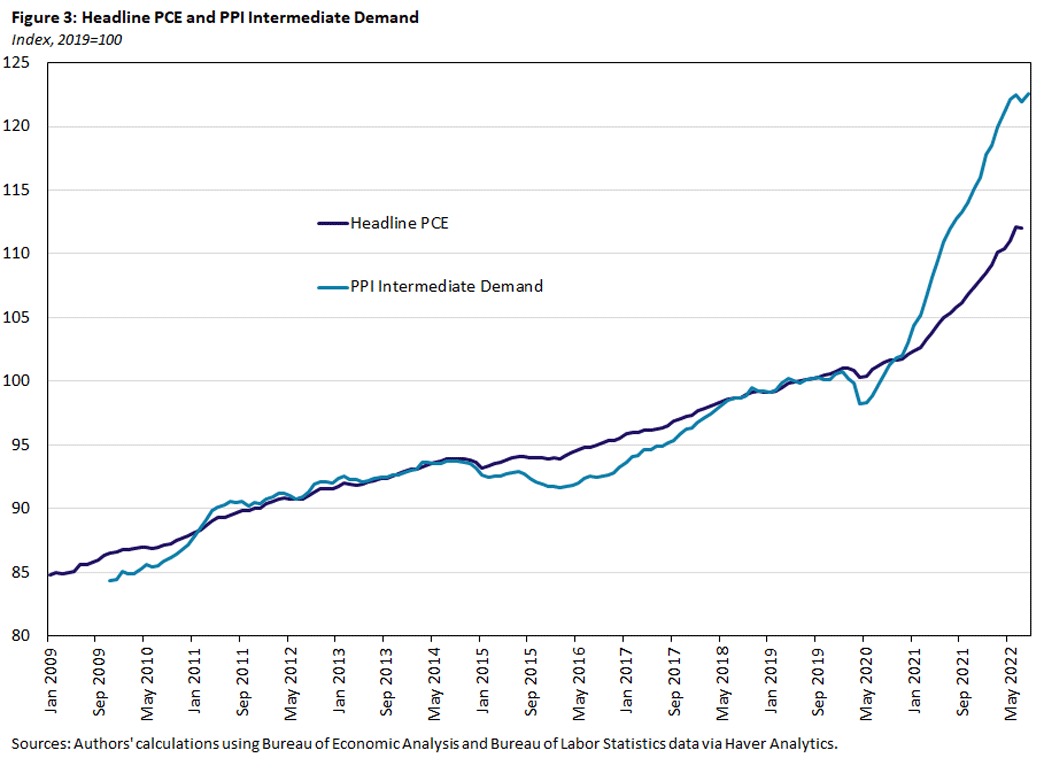

Is there also a relationship between the levels of the two price indexes? Figure 3 shows the levels of both price indexes, normalized to equal 100 in 2019.

Despite the limited window of observations, the level of PPI for intermediate demand appeared to move reasonably closely with the level of the PCE price index prior to the pandemic, albeit with greater volatility for the PPI. A gap began to emerge between the two price indexes between 2015 and 2017, but it seemed to narrow relatively quickly and, in fact, closed by the middle of 2018.

After the onset of the pandemic, the two price indexes began to diverge, with the rise in PPI-ID outpacing the rise in PCEPI, though the gap between the two appears to have stabilized in recent months. This evidence suggests some relationship may exist between the levels of both series: Gaps that open up between the two may tend to close over time.

Modeling the Relationship

In our next analysis, we apply a statistical procedure called a vector error correction model (VECM), which depicts the relationship between variables as a function of their growth rates and their levels. Additionally, the procedure can estimate short-term and long-term effects of one variable on another, as well as allow variables to have potential feedback loops for each other.

We estimated the VECM using monthly data on the PPI-ID and PCE from November 2009 through July 2022. We chose particular details of the model — such as number of lags and presence of deterministic regressors — according to their ability to parsimoniously fit the historical data.

The model finds evidence that the two price indexes do indeed move together over the long run — a relationship that economists call co-integration — with growth rates of PPI having a statistically significant impact on the growth rates of PCE prices, and vice versa. In addition, the gap between the two series matters as well: When the gap between the PPI and PCE price indexes strays beyond its usual level, the two series will adjust to normalize that gap over time.

Forecasting Next Year's Inflation

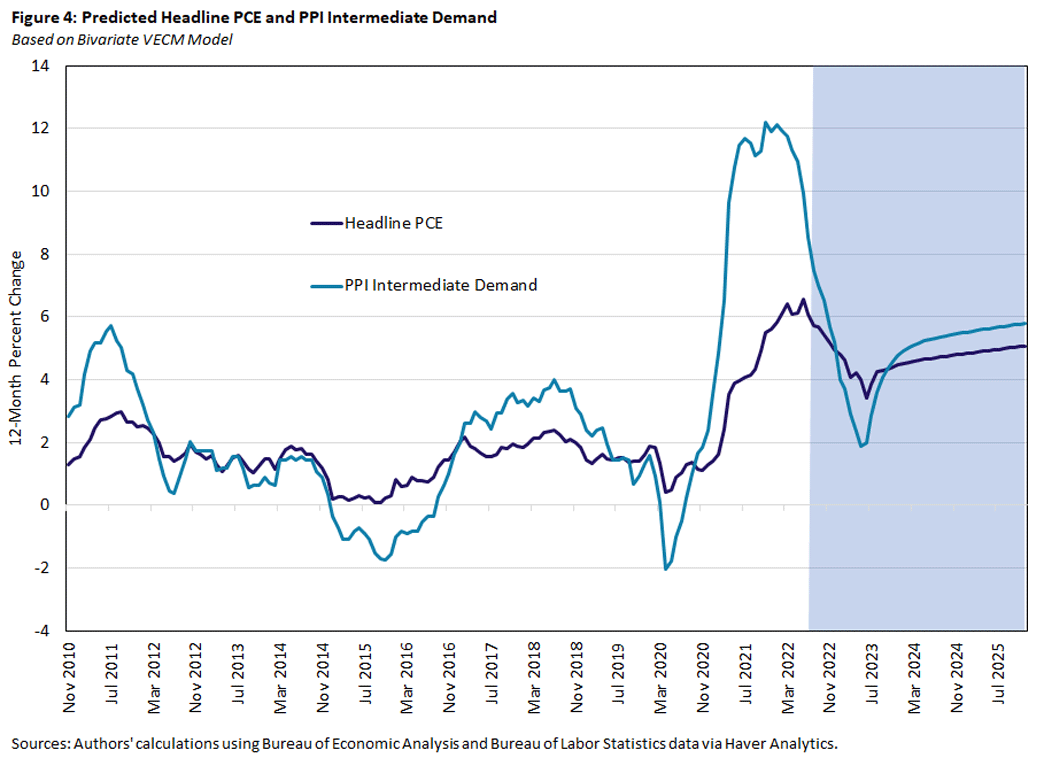

What do the latest PPI and PCE readings imply for inflation next year? We can use our simple model to forecast inflation, shown in Figure 4.

Assuming no further shocks to consumer or producer prices in the future, the model suggests PPI inflation will fall below 2 percent in the second quarter of 2023, due to high base effects from elevated inflation in spring 2022. However, after those base effects roll off the calculation, PPI inflation is projected to rise further, ending 2024 at 5.5 percent.

Qualitatively, the model's predictions for PCE inflation are similar but contain less of an adverse base effect from spring 2022. Thus, forecasted PCE inflation for next year remains above the Fed's target, ending 2023 at 4.8 percent.

Luckily for the real world, there are many factors influencing inflation that this simple two-variable model fails to capture, which may make its predictions more ominous than reality. Most importantly, the model does not consider the effects of tightening monetary policy. But what this exercise reveals is that the pricing pipeline continues to flow, and the normalization of upstream price pressures next year may be an important contributor in getting back to target inflation.

John O'Trakoun is a senior policy economist and David Ramachandran is a research associate in the Research Department at the Federal Reserve Bank of Richmond.

To cite this Economic Brief, please use the following format: O'Trakoun, John; and Ramachandran, David. (September 2022) "Building A Pipeline Between Producer and Consumer Prices." Federal Reserve Bank of Richmond Economic Brief, No. 22-38.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us