What Makes Supply Chains More Resilient to Economic Shocks?

Economic Brief

November 2022, No. 22-46

The recent supply chain disruptions caused by COVID-19 lockdowns highlighted the importance of understanding supply chain resilience, which is the extent to which supply chains can resist, adapt to and recover from a sudden economic shock. We analyze the various COVID-19 lockdowns across India to understand which supply chains were more resilient to the lockdown disruptions. Firms that bought more complex products and that transacted with fewer and more important suppliers proved to be more resilient by maintaining buyer-supplier relationships through the lockdowns and exhibiting smaller declines in input value purchases.

Firms tend to specialize in producing different goods and trade them both within and across borders, which improves efficiency in production. However, dependencies on acquiring key inputs can also propagate and amplify economic disruptions. Understanding the consequences of supply chain linkages between firms gained new attention in the past few years, following disruptions like COVID-19 lockdowns, which created supply shortages worldwide and contributed to recent inflationary pressures.

A recent working paper by three of the authors of this article — "Supply Chain Resilience: Evidence from Indian Firms" by Gaurav Khanna, Nicolas Morales and Nitya Pandalai-Nayar — focuses on understanding what features make supply chains more resilient to sudden economic shocks. Supply chain resilience is broadly defined as the ability of a supply chain to resist, adapt to, and recover from a negative economic disruption. Identifying the features associated with higher resilience is key when thinking about which supply chains are more at risk to future economic shocks.

The Case of India: Using COVID-19 Lockdowns to Measure Supply Chain Disruption

To tackle this issue, two main components are needed:

- Detailed information on the transactions between firms to evaluate how the relationships between buyers and suppliers change over time

- A large economic shock that disrupts supply chains to varying degrees to compare how supply chains with different characteristics respond to such shock

We focus on India and consider COVID-19 lockdowns in March 2020 across districts as our large supply chain disruption. Throughout the paper, we use the term "supply chain" to refer to the relationship between firms and their suppliers.

We obtain data on the universe of firm-to-firm transactions within a large Indian state.1 Our data include all transactions between January 2018 and December 2020 between Indian firms, as long as either the buying or selling firm (or both) are located in the state.2 These unique data allow us to construct the full network of buyers and suppliers, compute the value of each transaction and construct our measures of supply chain resilience.

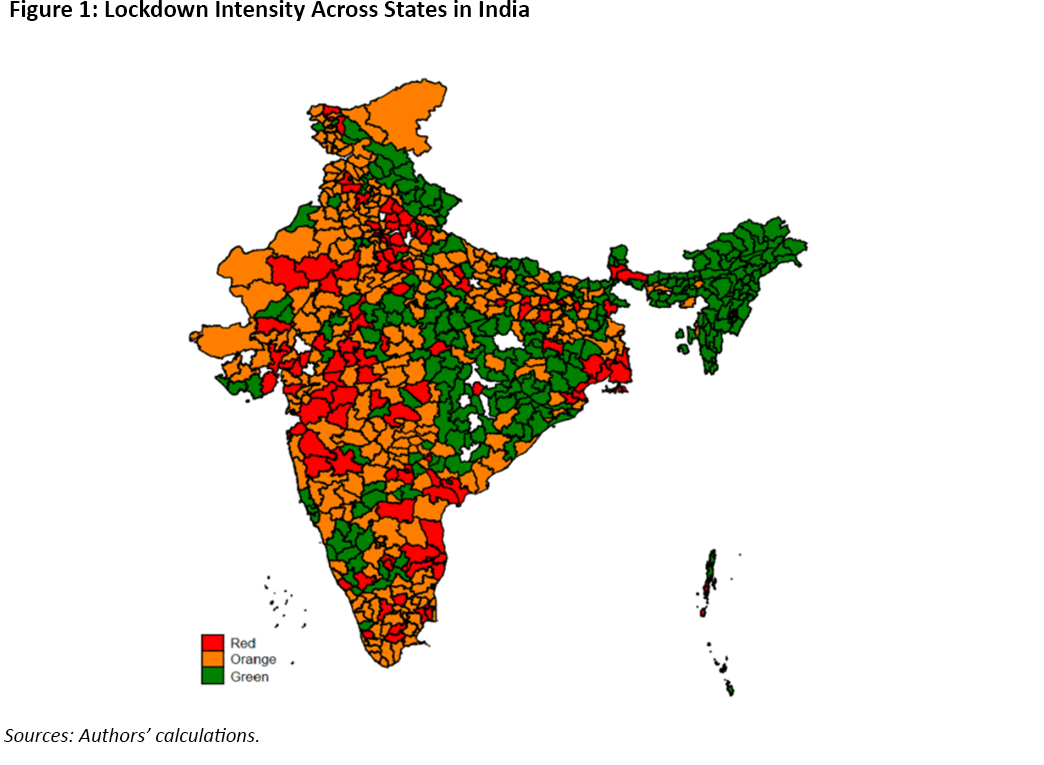

In March 2020, India announced sudden and strict nationwide COVID-19 lockdown policies. India's COVID-19 cases at the time were low, so the lockdowns were put in place mainly to prevent disease spread. The lockdowns were implemented at the district level and classified each district as red, orange or green based on COVID-19 incidence, as shown in Figure 1. Red-zone districts experienced the strictest lockdowns, as public transit, spas, barbers and malls were required to shut down, and large auto and pharmaceutical distributors in these districts reduced or temporarily stopped operations. Green-zone districts, on the other hand, saw significantly fewer and less stringent restrictions.

These differing lockdown intensities allow us to compare firms within the same industry and location, where some firms had suppliers in high lockdown areas while other firms had suppliers in mild lockdown areas. This comparison allows us to analyze the extent to which the lockdown shock created disruptions between firms and their suppliers.

We construct a measure of firm exposure to the lockdown policies based on supplier location. To do so, we use our data to identify suppliers' locations prior to the lockdowns. We then assign a score to each supplier depending on the lockdown policy imposed in their district: A supplier in a red district receives a score of three, while a supplier in a green district receives a score of one.

Finally, we aggregate suppliers for each firm to compute the supplier exposure to lockdowns. Firms that purchased goods from suppliers located in red areas will have higher supplier exposure risk than firms that purchased goods from suppliers located in green areas.

We measure supply chain resilience in three ways. First, we look at how firms decrease the value of their input purchases following the lockdowns. Input value can be thought of as a proxy for firm-level production. Second, we compute the separation rates of firms from their suppliers and evaluate how likely buyer-supplier relationships survive the shock. Finally, we look at how easily firms can switch suppliers if those relationships get broken. To do so, we calculate the "net separation rate," where we subtract the supplier entry rate from the supplier separation rate. This measure captures how many net suppliers firms gain or lose after the shock.

Lockdown Impact on Supply Chain Resilience

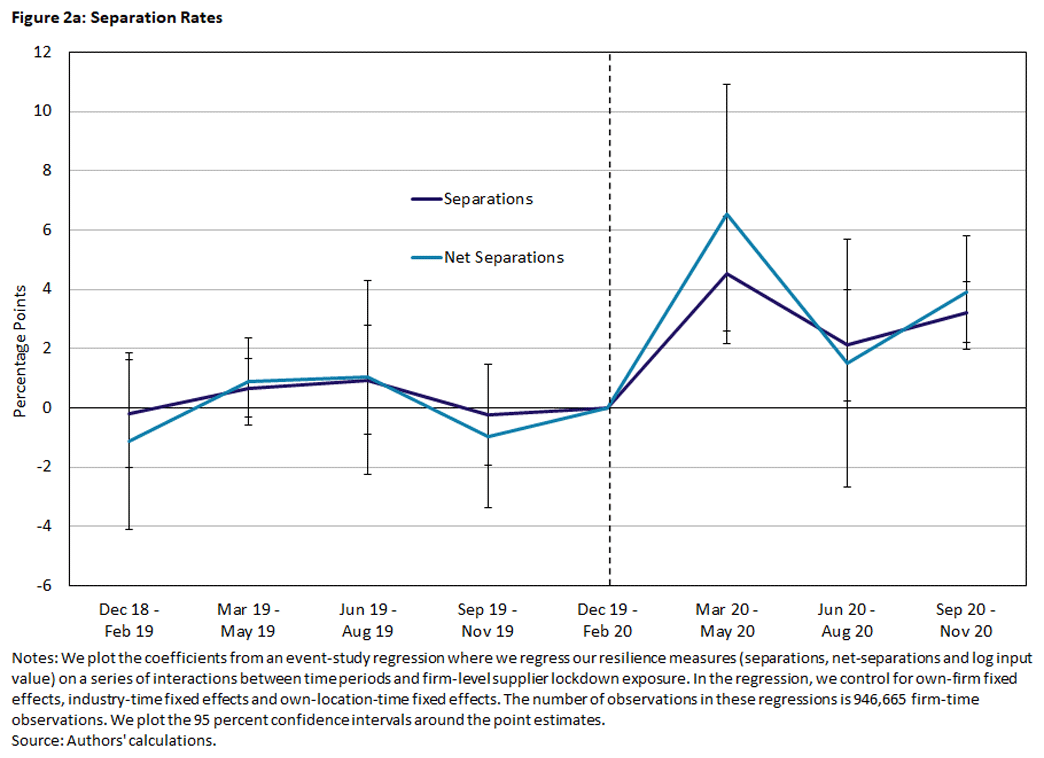

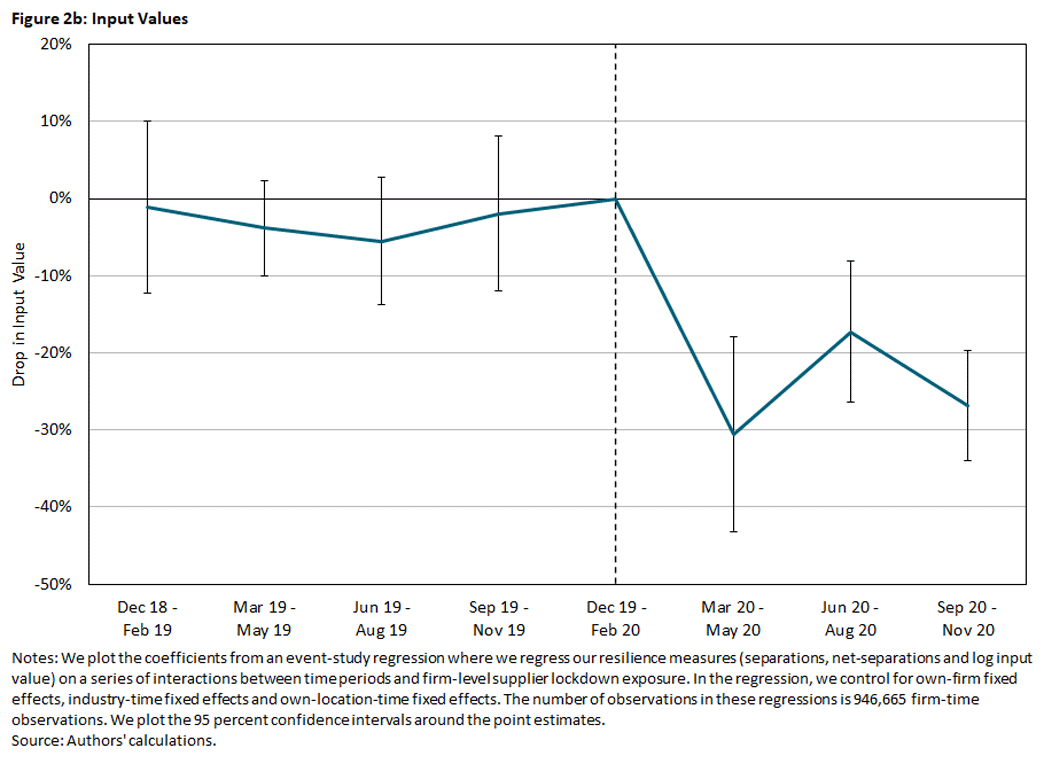

Figures 2a and 2b plot the difference in resilience outcomes (separations, net separations and input values) between firms with average supplier exposure to lockdowns and firms with supplier exposure one standard deviation greater than average. Intuitively, they measure the differential outcomes between firms with suppliers in high lockdown areas and similar firms with suppliers in average lockdown areas.

In Figure 2a, we plot the percentage point (pp) difference in separation rates and net separation rates between high-exposed and low-exposed firms. Focusing on separations, we see that from March to May in 2020, firms with high supplier exposure to lockdowns experienced a 4.1 pp higher separation rate than firms with average supplier exposure. The propensity to break links with suppliers is persistent throughout 2020. Similarly, for net separations, highly exposed firms experienced a 6.5 pp higher net separation rate.

In Figure 2b, we shift our attention to inputs. Firms with high supplier exposure to lockdowns experienced a 30 percent decline in the value of inputs purchased during the same period relative to firms with average supplier exposure. The decline in inputs is also quite persistent throughout 2020, where firms that were highly exposed to lockdowns through their suppliers never fully recover.

These figures corroborate that the shock we study — a firm's suppliers being subject to harsh lockdown policies — indeed affected the resilience of the buyer-supplier relationship by decreasing the total value of inputs purchased by highly exposed firms, making buyer-supplier relationships more likely to break and making it harder for firms to find new suppliers.

What Features Are Associated With More Resilient Supply Chains?

We proceed to examine characteristics associated with resilience. This is important because identifying which supply chains are more at risk is needed to create contingency policies and to lighten or prevent negative impacts from shocks. While there are many dimensions for comparing supply chains and evaluating their differences in resilience, we focus on five main indicators:

Product Complexity

How complex are the products a firm purchases? We define firms to have high-complexity supply chains if they buy products that require many different inputs to be produced.

Product Concentration

Are firms' purchases concentrated in many or few distinct products? Firms are considered to have high product concentration if most of their input purchases go into a single product. A higher number means more concentration, while a smaller number implies a diversified demand across many distinct products.

Supplier Concentration

Are firms dependent on a small number of suppliers? We measure how concentrated firm input purchases are, with a higher number implying higher dependence on a single supplier.

Supplier Importance

How important are firms' suppliers? We measure the average supplier importance through the supplier outdegree, which measures how big suppliers are, how many customers they have and how important suppliers are for their customers.

Supplier Availability

How available are the products firms generally purchase? For each product, we look at how many suppliers are in the market. A high value of this measure implies that firms tend to buy products that have many available suppliers in the market.

Evaluating Supply Chain Resilience Characteristics

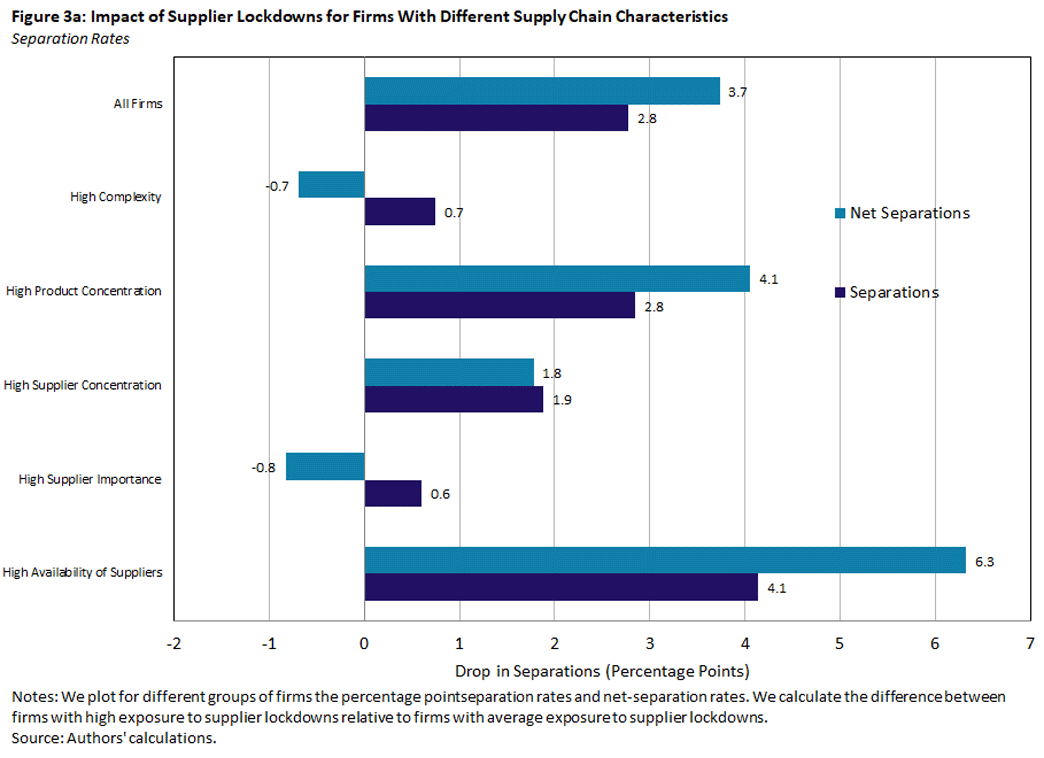

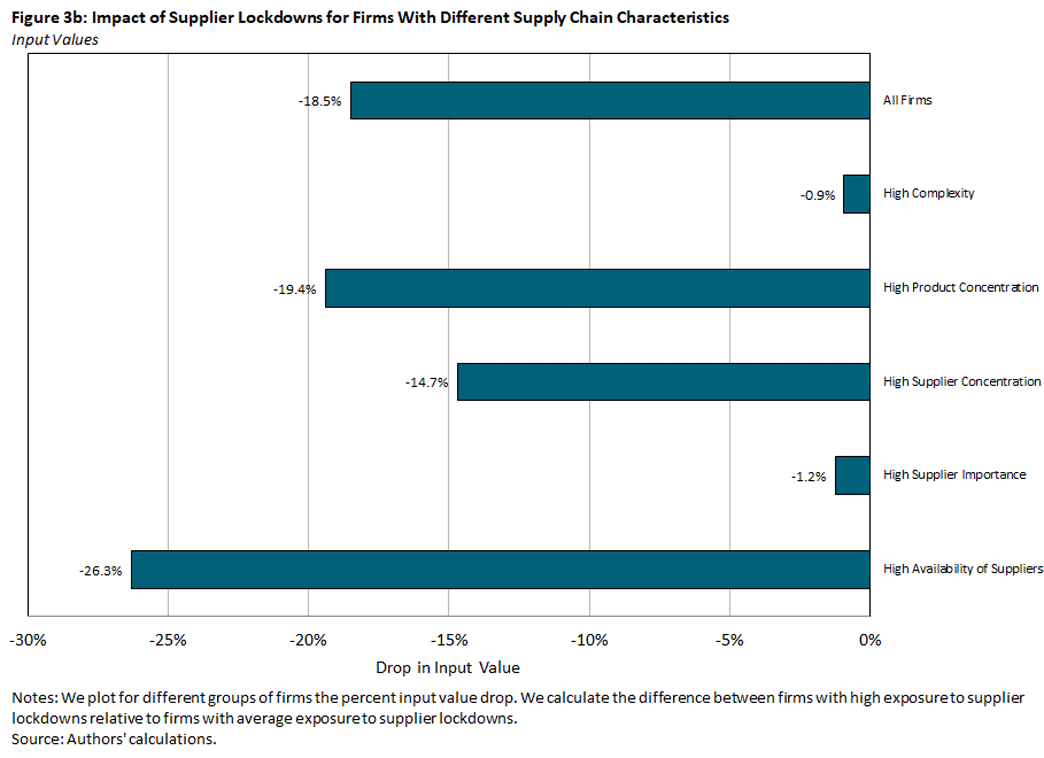

In Figures 3a and 3b, we present the change in input values in response to the lockdown shock for firms with high-exposed suppliers relative to average-exposed suppliers, as well as show results for separations and net separations, which are consistent. We present the results for different groups of firms with high levels of each of the five characteristics mentioned above.3

In the top row of each figure, we present the baseline results for all firms. Firms one standard deviation above the mean in terms of supplier-lockdown risk had 18.5 percent lower input purchases than firms with average supplier-lockdown risk in the period between March 2020 and August 2020.

In the second line of each figure, we look at firms with the highest levels of input complexity, where we see that the impact of the lockdowns was much milder. These firms decreased input values by only 0.9 percent relative to firms with average supplier exposure. Also, firms with high product concentration had a 19.4 percent input value decline, higher than the average. This means that firms with more complex supply chains and low product concentration or with high-complexity inputs were more resilient to the shock.

One possible interpretation is that firms that depend on high-complexity, hard-to-find inputs invest in fostering relationships with their suppliers and build contingency plans for shocks. When the lockdowns were imposed, these firms benefited from the built-in resilience, maintained the relationships with their suppliers and minimized input declines.

Firms with high levels of supplier concentration had lower input losses than the average, exhibiting an input drop of 14.7 percent (compared to 18.5 percent for all firms). This indicates that firms dependent on a single supplier were more likely to maintain the relationship with that supplier after the shock, making their supply chains more resilient. Firms with suppliers that were more important —because they were bigger, had more customers and are more vital for their customers — had minimal input losses due to the lockdowns, only showing a 1.2 percent input drop. More important suppliers are more resilient themselves, making the supply chain more likely to withstand the shock and minimize production decreases.

Finally, we examine the differences for firms that buy widely available products. We find that such firms experience larger input purchase drops due to the lockdowns, indicating that their supply chains were less resilient to the shock. This suggests that firms that tend to buy products for which there are many suppliers have less incentive to invest in strong relationships with their buyers, which makes them less resilient to sudden shocks.

How Did Supply Chains Readjust After the Shock?

We finish our analysis by looking at how supply chains reformed after the lockdown shock. We find that firms that were highly exposed to lockdowns from their suppliers concentrate their purchases in larger and better-connected suppliers. Firms that used to buy inputs from faraway suppliers begin to buy from closer suppliers, and they increase the share of purchases from suppliers in their same state. Overall, we find that firms seem to adjust their supplier composition to mitigate risks and increase their resilience.

Conclusion

In sum, we investigate the features associated with more resilient supply chains. We look at the COVID-19 lockdowns in India as a large shock that disrupted supply chains to varying degrees. Firms with more complex supply chains proved to be more resilient to the shock by having lower input decreases and maintaining relationships with their suppliers. Firms that transacted with fewer and more important suppliers also fared better, as the buyer-supplier relationships were less likely to break following the lockdowns.

On the other hand, firms that bought products with many available suppliers in the market experienced more separations and larger input decreases, as they likely invested less in maintaining relationships with their suppliers prior to the shock. This evidence from Indian firms provides insights into important policy questions regarding firms' preparation for and mitigation of future supply chain shocks.

Claire Conzelmann is a research associate and Nicolas Morales is an economist in the Research Department of the Federal Reserve Bank of Richmond. Gaurav Khanna is an assistant professor of economics at the University of California-San Diego. Nitya Pandalai-Nayar is an assistant professor at the University of Texas-Austin.

1

For confidentiality reasons, we cannot name the Indian state we are working with, but the state has a fairly diversified production structure, roughly 50 percent urbanization rates and high levels of population density.

2

The data are generated by compiling records of e-way bills, as firms need to issue one of these bills and pay a value-added tax when they transport goods to another firm. These data consist mostly of manufacturing goods and cover the universe of transactions of transported goods valued over $700.

3

We define a firm to have a "high value" of the characteristic whenever it is above the 75th percentile of the distribution in terms of that characteristic.

To cite this Economic Brief, please use the following format: Conzelmann, Claire; Khanna, Gaurav; Morales, Nicolas; and Pandalai-Nayar, Nitya. (November 2022) "What Makes Supply Chains More Resilient to Economic Shocks?" Federal Reserve Bank of Richmond Economic Brief, No. 22-46.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us