Detecting Inflation Instability

Economic Brief

April 2023, No. 23-11

In a stable monetary policy regime, the share of relative price increases helps to explain monthly inflation fluctuations. We illustrate this regularity with U.S. data from January 1995 through February 2020, then we use it to evaluate whether the regime has remained stable during the pandemic period. From March 2021 to February 2022, the behavior of inflation and the share of relative price increases was inconsistent with the pre-pandemic regime. Recent data show some signs of a return to that regime.

Before COVID-19, the U.S. experienced a 25-year period of low and stable inflation. As is well known, inflation rose rather dramatically in the spring of 2021, and although it has come down from a peak, the most recent readings for PCE inflation are still well above the Federal Open Market Committee's 2 percent target.

When the recent high inflation numbers first appeared, it was widely perceived that they resulted from shocks to demand and supply for specific goods and services, as opposed to aggregate factors related to monetary policy. However, as the high inflation persisted, this interpretation seemed less and less plausible. Indeed, the Fed made a fairly dramatic adjustment to monetary policy starting in March 2022.

This episode illustrates a more general challenge facing monetary policymakers (as well as researchers and market participants): Do unusually high (or low) monthly inflation numbers reflect short-run effects of large relative price changes, or do they signal the need for an adjustment to monetary policy?1

While there are various existing approaches to inferring the "signal" in noisy monthly inflation numbers, in this article I use an approach introduced in my 2022 article on relative price changes and high inflation to assess the behavior of inflation over the last year and, more generally, over the COVID period. This approach uses the relationship between inflation and relative price changes during the stable inflation period from January 1995 to February 2020 to evaluate data from the COVID period and infer whether it is consistent with stable inflation around 2 percent.

Inflation Data

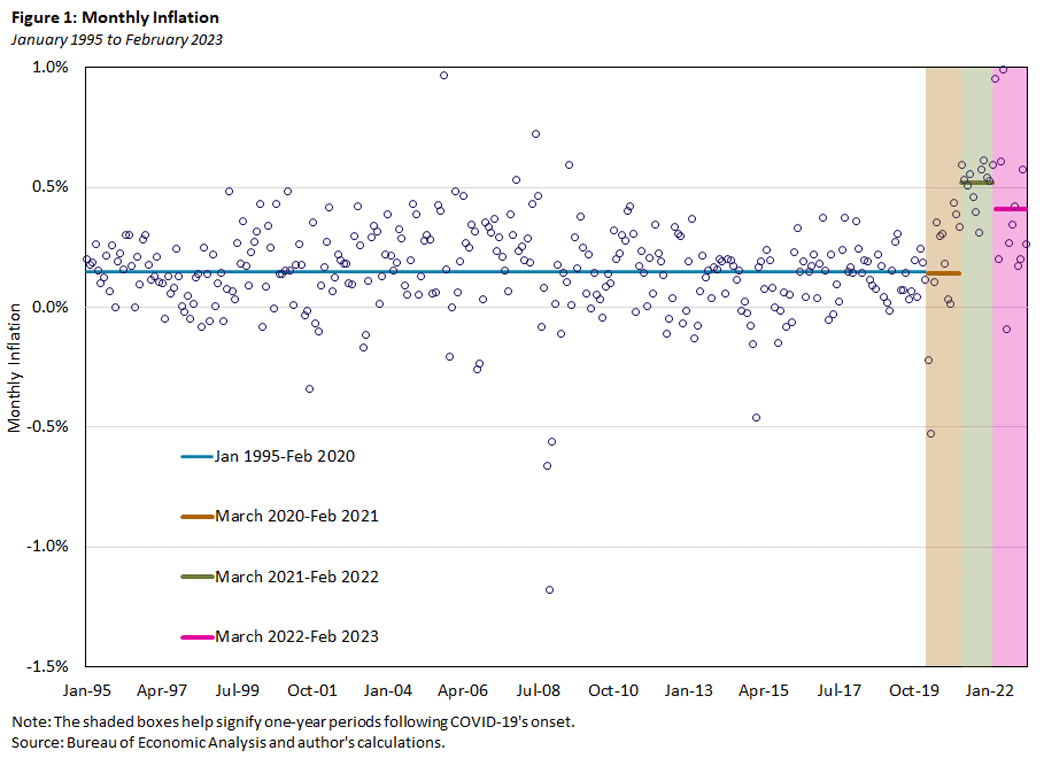

Figure 1 below plots the monthly PCE inflation rate from January 1995 to February 2023, the latest month for which data are available. The open circles are the monthly inflation rates, and the figure also displays the average inflation rates for four subperiods:

- January 1995-February 2020: Average monthly inflation was 0.15 percent, or 1.8 percent at an annual rate.

- March 2020-February 2021: Average monthly inflation was 0.14 percent, or 1.7 percent annualized.

- March 2021-February 2022: Average monthly inflation was 0.52 percent, or 6.4 percent annualized.

- March 2022-February 2023: Average monthly inflation was 0.41 percent, or 5.0 percent annualized.

The FOMC formally established a 2 percent target for PCE inflation in January 2012. Average inflation was quite close to that target from 1995 through 2019, and it remained close to the target in the early months of the pandemic. Since then, inflation has been far above target and well above any prior 12-month period since 1995. (The previous high was 4.1 percent in the 12 months ending in July 2008.)

Inferring Whether Inflation Is Stable

The inflation experience of the last two years is a particularly stark example of how difficult it can be to determine in real time whether monthly inflation numbers are generated by a stable regime in which the inflation target is maintained.

This question is often addressed implicitly by focusing on measures of core or trimmed mean inflation.2 In addition, one can in principle filter the data using factor models, such as the one proposed in the 2010 paper "Relative Goods' Prices, Pure Inflation and the Phillips Correlation."3

I take a different approach, which I introduced in my aforementioned March 2022 article "Relative Price Changes Are Unlikely to Account for Recent High Inflation." When inflation is stable, large changes to relative prices for particular consumption categories nonetheless pass through to monthly inflation. One way to summarize those large changes is by the dollar share of expenditures experiencing a relative price increase: By construction, the average relative price change is zero, so if the share of expenditures with a relative price increase is small, then the average of those relative price increases must be large, compared to the average relative price decrease.4 I use the relationship between inflation and the share of relative price increases revealed by the stable inflation period from January 1995 to February 2020 to infer whether more recent data is consistent with that same regime.

Inflation and the Share of Relative Price Increases

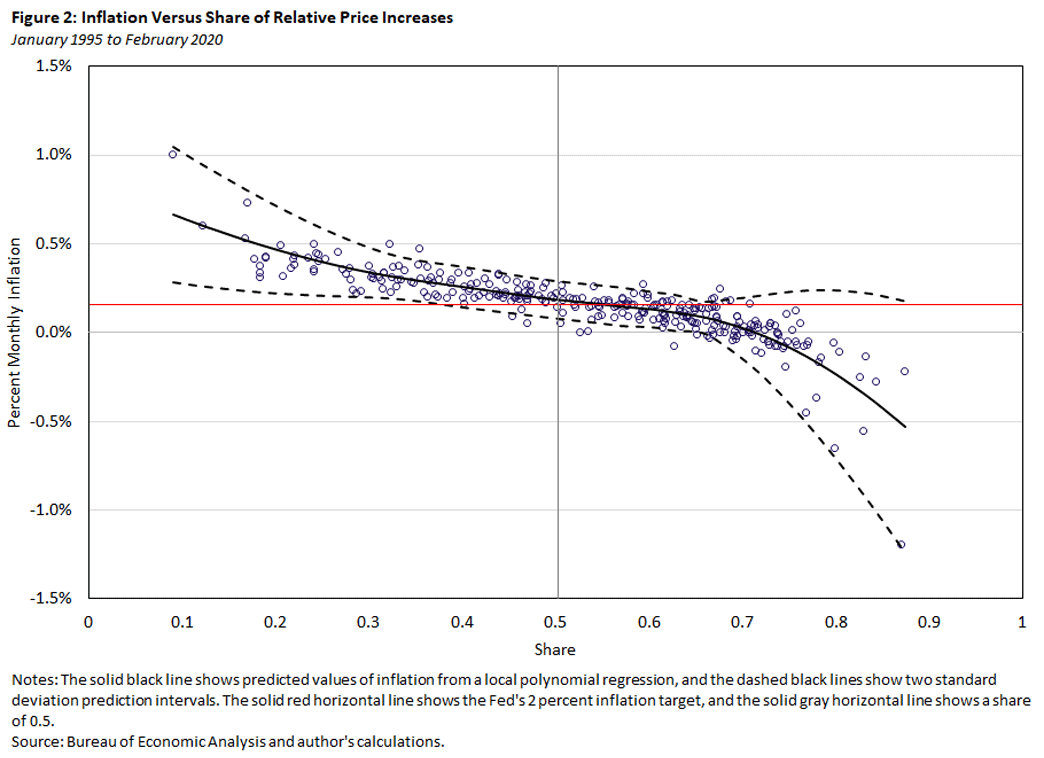

Figure 2 below plots the monthly inflation rate against the monthly share of expenditures with a relative price increase from January 1995 to February 2020. In addition, Figure 2 displays predicted values of inflation from a local polynomial regression, along with two-standard-deviation prediction intervals. The red horizontal line corresponds to the FOMC's 2 percent inflation target, and the grey vertical line indicates a share of one half. If the distribution of relative price changes is symmetric, then the share of relative price increases will be one-half. The average share over the sample in Figure 2 was 0.53.

The main takeaway from Figure 2 above is that there was a systematic negative relationship between inflation and the share of relative price increases during this period. Some intuition for this relationship was provided above, but it may also help to think about the example of an unusually large increase in gasoline prices in a month when other categories are experiencing business as usual.

Suppose the gasoline price increase is so large that gasoline is the only category experiencing a relative price increase. Then, the share of expenditures with a relative price increase would simply be the gasoline share of expenditures, about 2.5 percent. Also, because the gasoline price increase was very high, inflation would be high. This logic helps explain the points on the far left of the figure, while the opposite logic explains the points on the far right. More generally, a higher share of expenditures with a relative price increase corresponds to a lower inflation rate, in a period when inflation is generally stable.

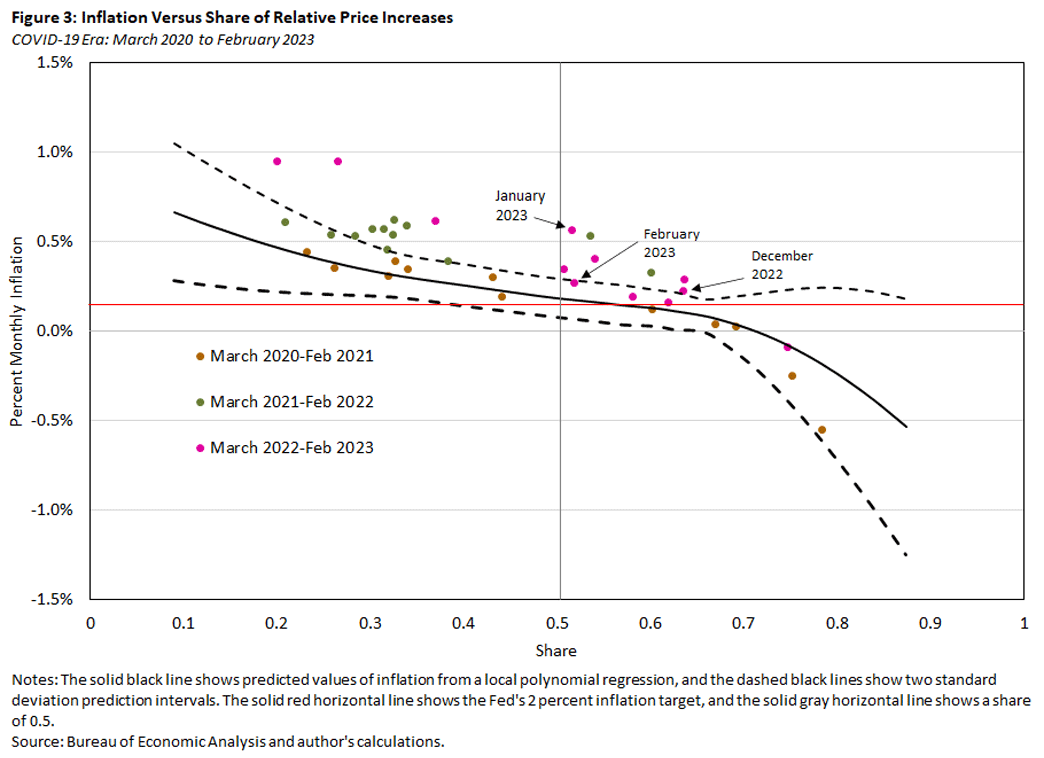

Next, we want to bring in data from the pandemic period and ask whether they have exhibited the same relationship between inflation and the share of relative price increases. Figure 3 below displays the same scatter plot as Figure 2 for the most recent three subperiods from Figure 1. Just as in Figure 1, the data are split up into three 12-month subperiods. The solid and dashed lines are the predicted values and prediction intervals from Figure 2, estimated over the pre-COVID-19 period starting in 1995.

During the first year of COVID-19, there was substantial variation in the share of relative price increases, but inflation in each month lay within the prediction interval generated by pre-COVID-19 data. We already saw in Figure 1 that average inflation did not change substantially in the first year of COVID. Figure 3 above reinforces the notion that inflation was stable by showing that the relationship between relative price changes and inflation remained stable.

The second year of the pandemic (the green dots) was virtually the exact opposite: Inflation was high, as we have already seen, but the increase cannot be explained by a small share of relative price increases together with the pre-COVID relationship. While the share of relative price increases was generally low — which would have corresponded to high inflation pre-COVID-19 — inflation was substantially higher than would have been predicted by the shares and the pre-pandemic relationship. In every month from March 2021 to February 2022, inflation was above the predicted level based on the share of relative price increases. In fact, seven of the 12 months saw inflation well above even the upper bound of the prediction interval.

The third year saw more "normal" variation in the share of relative price increases. It also displayed some signs that the pre-pandemic relationship with inflation is reemerging, but these signs are tentative: While December and February were not far from the pre-COVID-19 relationship, January was an extreme outlier, as the inflation rate was more than twice as high as in any post-1995 month with a similar share of relative price increases (0.51).

Conclusion

We've shown that, when inflation was low and stable from 1995 until the pandemic era, there was a systematic relationship between the share of relative price increases and inflation. We then used that relationship to evaluate the stability of inflation during the pandemic. The clear deterioration of that relationship certainly provides cause for concern.

However, there are important qualifications and, hence, reasons for hope that inflation may come back to target relatively quickly. First, long-term expectation measures show little sign of inflation becoming unanchored from that target. Second, within the framework presented here, even large deviations from the stable relationship of Figure 2 do not necessarily represent a fundamental unanchoring of inflation (a regime shift). From the standpoint of a typical macroeconomic model, such deviations could arise either from a regime shift or from large shocks in a continued stable environment. In the latter case, as long as monetary policy behaves (or resumes behaving) as it did during the pre-COVID-19 period, inflation will return to target when the shocks dissipate.

Ultimately, the proof will need to be in the pudding. However, even absent a rapid return of inflation to target, a reemergence of the pre-pandemic relationship between inflation and the share of relative price increases would be a powerful signal that inflation is behaving in a way consistent with the 2 percent inflation target.

Alexander L. Wolman is a vice president in the Research Department at the Federal Reserve Bank of Richmond.

1

This discussion is admittedly loose. In principle, relative price changes can be an early warning sign for inflation. Conversely, sudden large aggregate shocks can move inflation in ways that monetary policy is powerless to offset, given the institutional frameworks in most industrialized economies.

2

For more on trimmed mean inflation, see the 2005 working paper "Trimmed Mean PCE Inflation (PDF)."

3

Also see the 2021 article "International Measures of Common Inflation."

4

A category's relative price change is defined as the difference between its nominal price change and the inflation rate.

To cite this Economic Brief, please use the following format: Wolman, Alexander L. (April 2023) "Detecting Inflation Instability." Federal Reserve Bank of Richmond Economic Brief, No. 23-11.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us