Relative Price Changes Are Unlikely to Account for Recent High Inflation

Economic Brief

March 2022, No. 22-10

March 2021 marked the first month of the ongoing high inflation episode in the U.S. Last September, I analyzed the first five months of this episode through the lens of the distribution of price changes for all PCE components. A small fraction of expenditures accounted for much of the high inflation in those months. In this Economic Brief, I provide a related analysis and incorporate a new summary statistic for the distribution of relative price changes. In the last four months, high inflation has not been concentrated in a small fraction of expenditures, deviating from the relationship we had largely seen in post-1994 data.

Last September, when I analyzed the high inflation we were experiencing relative to the past 25 years, I found that a small fraction of expenditures accounted for much of the increase. With inflation remaining high, I wanted to follow up on that analysis.

What I found is that the high inflation since October has not been concentrated in a small fraction of expenditures, deviating from what was a reliable relationship in post-1994 data between the level of inflation and the distribution of relative price changes. In addition to updating some of the previous results, I introduce a new summary statistic for the distribution of relative price changes that was especially informative about short-term fluctuations in inflation until the last several months.

Background on PCE Inflation

Before we get into the analysis and findings, some background on inflation would be helpful. (A more detailed version of this background is available in my previous analysis "How Broad-Based Is the Recent High Inflation?" from September.)

PCE inflation — the measure of inflation targeted by the Federal Reserve — is calculated from price changes for hundreds of categories of goods and services. Since 1995, PCE inflation has been stable and close to the 2 percent target the Fed established in 2012.

While inflation has been stable, there has nonetheless been large variation in the price changes of individual consumption categories. For example, inflation in February 2015 was exactly 2 percent at an annual rate, yet a quarter of consumption categories had annualized price increases of more than 4 percent, and a quarter had annualized price decreases of more than 2 percent.1

As long as inflation is close to the Fed's target, such dispersion has little relevance for monetary policy: Supply and demand factors vary across categories and over time, causing relative price changes that show up as variation in nominal price changes across categories.

However, when inflation moved significantly above 2 percent starting last March, the distribution of price changes across categories took center stage. To the extent that categories representing a small share of expenditures accounted for high inflation, there was a compelling argument that inflation would come back down when supply and demand factors affecting those categories normalized. Alternatively, if high inflation reflects higher rates of price change for all categories, it is more likely that adjustments to monetary policy would be required to reduce inflation.

Analyzing High PCE Inflation

We quantify the "breadth" of the recent high inflation using measures based on Bureau of Economic Analysis data covering more than 300 consumption categories. We begin by approximating monthly PCE inflation as a weighted average of price changes for the component categories of consumption, where the weights are the expenditure shares of each category for the month prior to the price changes.2 Although this formula does not perfectly reproduce actual PCE inflation, the approximation is generally quite close, and it facilitates the analysis below.3

For each month, we rank the consumption items from highest to lowest by percent price change, then use the corresponding expenditure shares to calculate these measures:

- The share of inflation accounted for by the 5 percent of expenditures with the highest ordered price changes

- The share of expenditures with the highest ordered price changes that accounts for 50 percent of inflation

- The share of expenditures with relative price increases (that is, with price changes greater than inflation)

If there are no relative price changes, then prices of all components grow at the same rate: the inflation rate. In this case, the highest 5 percent (50 percent) of price changes would account for 5 percent (50 percent) of inflation, and the share of expenditures with relative price increases would be zero. Thus, inflation is "pervasive."

On the other hand, if inflation is less pervasive — that is, price increases are more concentrated in certain expenditure categories — then:

- The 5 percent of expenditures with the highest ordered price changes would account for more than 5 percent of inflation.

- Less than 50 percent of expenditures with the highest ordered price changes would account for 50 percent of inflation.

The relationship between pervasive inflation and the share of expenditures with relative price increases is more subtle. Yet, that statistic had the tightest relationship to monthly inflation prior to COVID and, therefore, provides the most insight into current inflation behavior. We will explain it in detail below.

Accounting for Inflation With the Top 5 Percent of Price Changes

We report here on the first two measures: the share of inflation accounted for by the highest 5 percent of price changes, and the share of expenditures that account for 50 percent of inflation.4 The figures and table below compare these measures' recent behavior to data starting in January 1995. Inflation over that period has generally been stable, with occasional brief episodes of high inflation.

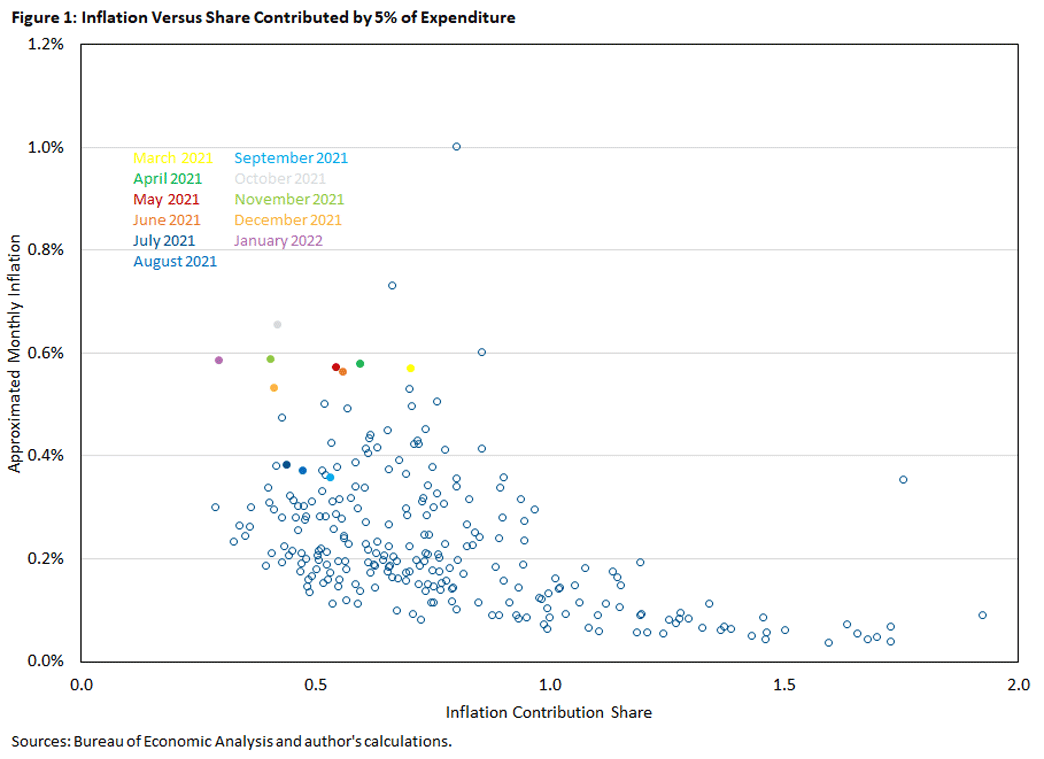

Figure 1 plots approximated monthly inflation against the share of inflation contributed by the top 5 percent of expenditures, ranked in decreasing order of price change. For example, if monthly inflation were 1 percent and the price change of the first 5 percent of expenditures was 10 percent, then the contribution on the horizontal axis would be 0.5 (that is, 0.05*10/1=0.5). The colored dots show data for the period March 2021 to January 2022.

There are three broad features to highlight from this figure.

Contribution of Top 5 Percent of Expenditures

The share of inflation contributed by the top 5 percent of expenditures has been above 0.28 each month of the sample. Recall that the smallest possible contribution is 0.05, which would imply that all price changes were the same size.

Relationship Between Contribution of Top 5 Percent and Inflation

Over the sample period prior to March 2021, there is a systematic relationship between the contribution from the top 5 percent and inflation, albeit one that is hard to characterize. For large x-axis values, inflation is low and insensitive to the contribution from the top 5 percent. This reflects the fact that, during a stable, low-inflation period, having very large shares of inflation contributed by the highest price changes can only be consistent with inflation close to zero.

On the other hand, smaller contributions from the top 5 percent (between 0.5 and 1.0) were consistent with a range of inflation rates — including the highest inflation in the sample — whereas the lowest contributions (less than 0.4) always coincided with monthly inflation less than 0.34 percent (about 4.1 percent at an annual rate). Small contributions from the top 5 percent correspond to inflation being relatively broad-based. Over the sample then, when inflation was most broad-based, it was never particularly high.

Change in Relationship

In the first seven months of the current episode (March through September), inflation and the contribution from the top 5 percent loosely obey their previous relationship. However, from October through January, this has not been the case.

Taking as given the share of inflation contributed by the top 5 percent of expenditures (price changes) in those months, the historical relationship would have predicted a substantially lower inflation rate than observed. That is, the dots for October through January lie above all other dots with similar inflation contribution shares. And from the other perspective, inflation this high has always corresponded to a greater contribution from the top 5 percent of expenditure.

Summary of Findings

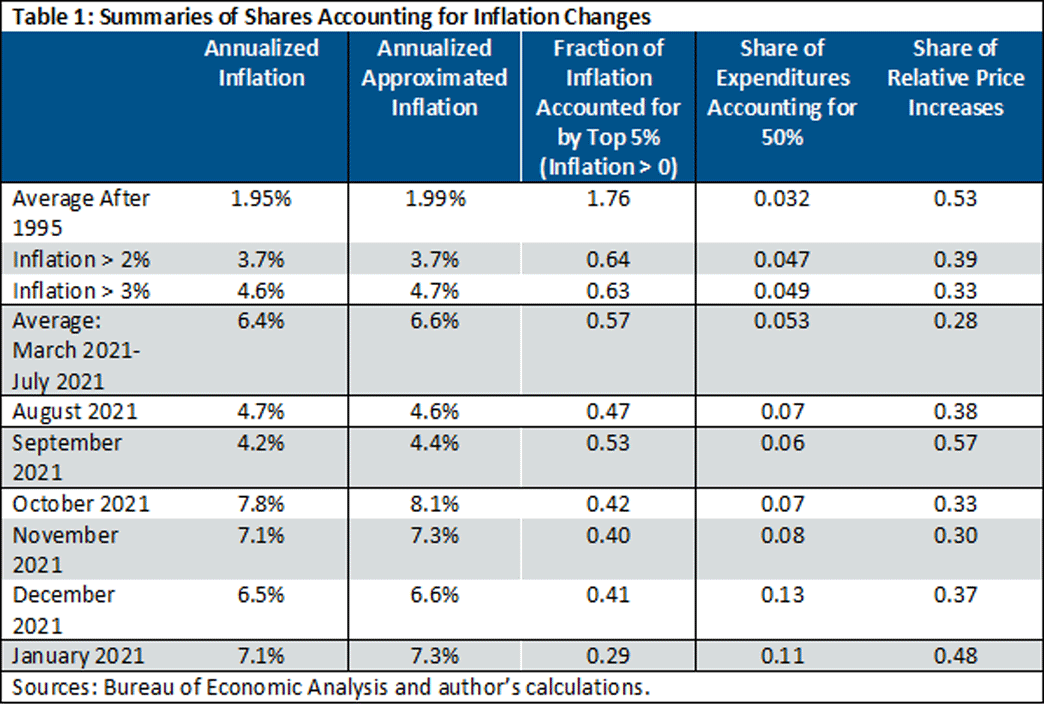

Table 1 reinforces these findings with summary statistics.

On average since 1995, the top 5 percent of price changes had a contribution fraction of 1.76, meaning it accounted for 176 percent of inflation. (The number can be above 100 percent because in a typical month there are price decreases as well as price increases.)

Restricting to months with inflation above 3 percent, the contribution drops to 0.63. Since October, however, the fraction has been below 0.43 each month — including a reading of 0.29 in January — against an average of 0.57 from March through July.

To summarize: Prior to October, in months with high inflation, the top 5 percent of price changes accounted for a higher share of inflation than in recent months.

Expenditures Accounting for 50 Percent of Inflation

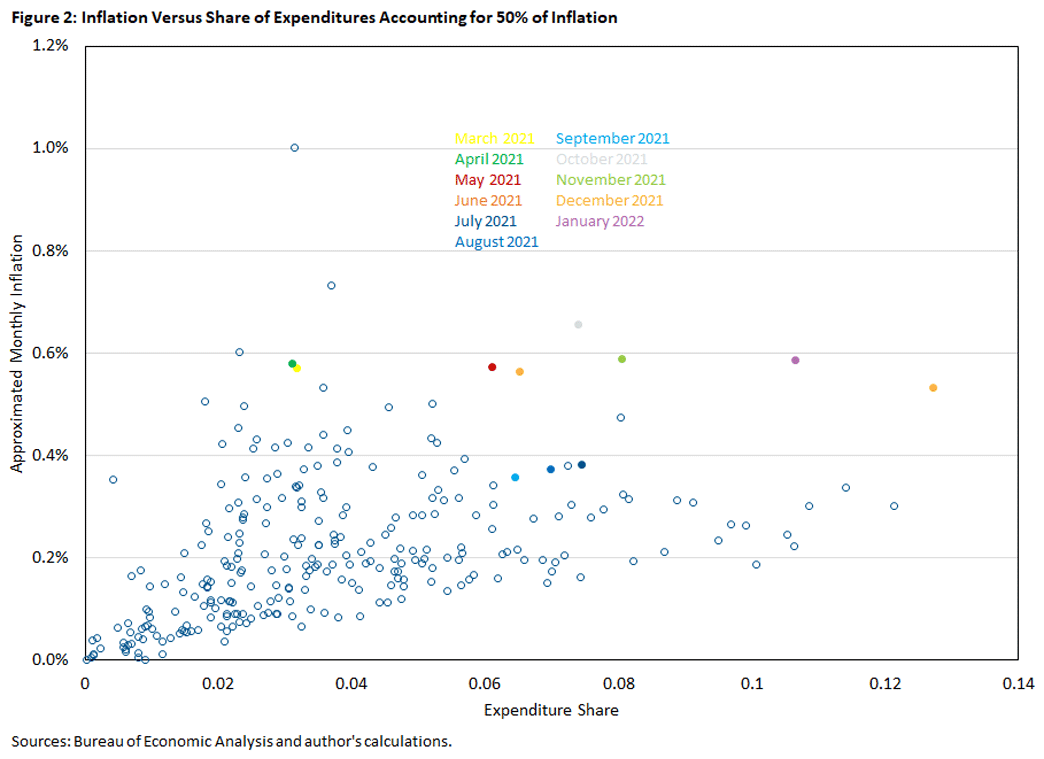

Figure 2 plots monthly approximated inflation against the share of expenditures accounting for 50 percent of inflation, with expenditure items again ranked in decreasing order of price change.

We highlight three aspects of the figure that have parallels to Figure 1.

Share Accounting for 50 Percent of Inflation

In every month, less than 13 percent of expenditures have large enough price changes (compared to inflation) to account for 50 percent of inflation. Recall that the maximum possible share is 50 percent, in the case where all price changes are identical.

Inflation and Share Accounting for 50 Percent

There is a generally positive relationship between inflation and the share of expenditures accounting for half of inflation, but again the relationship is not easy to characterize. For low contributions, the increasing relationship is intuitive: If a very small fraction of expenditures accounts for 50 percent of inflation during a period of overall low and stable inflation, then inflation must be close to zero in that month.

On the other hand, if the share of expenditures accounting for 50 percent of inflation is very high (close to 0.5), then most price changes are similar, and in a period of stable inflation, we would expect inflation to be near its mean. Over an intermediate range, this simple reasoning breaks down, and we see wide dispersion in inflation.

Change in Relationship

From March through September, inflation and the share of expenditures accounting for half of inflation did not deviate markedly from their historical relationship. But since October, there has been a clear break from that historical relationship. Inflation has been higher than one would have predicted by the high shares of expenditures accounting for half of inflation. For example, the dot representing inflation in January is far above the inflation rates that had previously been consistent with the 0.11 share of expenditures that accounted for half of inflation in January.

Table 1 contains summary statistics that reinforce these findings. The sample average expenditure share that accounts for half of inflation is 0.03, and this rises to 0.05 in months when inflation is above 3 percent. From March to July, the average was 0.05, but it has been 0.07 or above since October.

Figures 1 and 2 and Table 1 tell a consistent story: In the early months of the current high-inflation episode, inflation was roughly in line with preexisting relationships to the largest price changes. Since October, those patterns have no longer held.

Inflation and the Share of Relative Price Increases

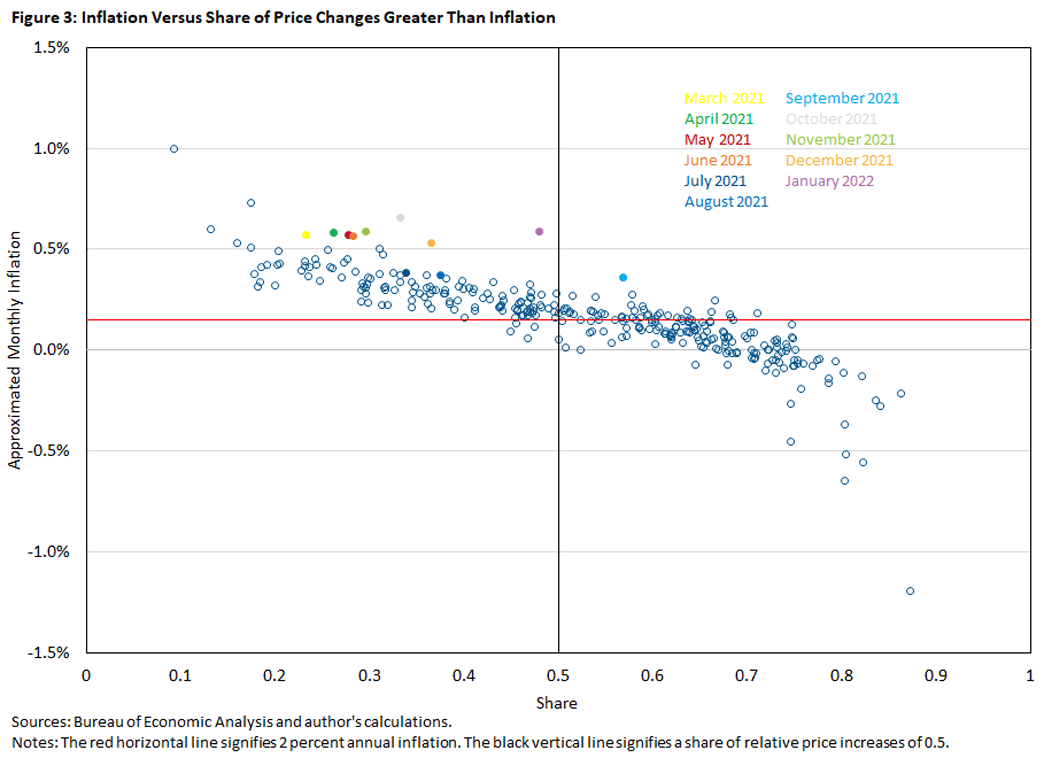

Figure 3 plots monthly approximate inflation against our third measure: the share of price changes greater than inflation, or equivalently the share of relative price increases.

To understand this measure, note that in each month (by definition) the average relative price change is zero because relative prices are measured relative to the overall price index. If the share of relative price increases is 0.5 (the black vertical line), then the distribution of relative price changes exhibits a basic form of symmetry: There are equal shares of relative price increases and decreases, and the average relative price increase is the same as the average relative price decrease.

If the share of relative price increases is different than 0.5, then the definition of relative price changes determines the ratio of the average relative price increase to the average relative price decrease. For example, suppose the share of relative price increases is 0.8, which implies the share of relative price decreases is 0.2. Then, the average relative price decrease must be four times as large as the average relative price increase.

We can now summarize the highlights from Figure 3, which are also shown in the fifth column of Table 1.

Relationship Between Monthly Inflation and Share of Relative Price Increases

Since 1995, there has been a close negative relationship between the monthly inflation rate and the share of relative price increases. At 2 percent inflation (the horizontal red line in Figure 3), the share of relative price increases has been 0.53, meaning that the average relative price increase has been slightly lower than the average relative price decrease.

Initial Months of High-Inflation Episode

In the first several months of the current high-inflation episode, the share of relative price increases was just 0.28, implying that the average relative price increase was large compared to the average relative price decrease. This is consistent with there being a small fraction of unusually large price increases. During these months, the relationship between inflation and the share of relative price increases was close to its pre-COVID pattern.

Change in Relationship

Since October, inflation and the share of relative price increases have deviated from their pre-COVID relationship. This was most notable in January, when that prior relationship would have predicted 2.5 percent annualized inflation based on the 0.48 share of relative price increases, compared to actual annualized inflation of over 7 percent.

Interpretation

There are two clear findings about the behavior of inflation in recent months:

- High inflation since October has not been driven by large price increases for a small share of expenditures.

- There has been a breakdown in the post-1995 relationship between inflation and the distribution of relative price changes.

What does the breakdown in that relationship mean? Figure 3 suggests that, from 1995 until early 2021, month-to-month inflation fluctuations were driven largely by real shocks to supply and demand for particular consumption items, against a backdrop of a stable monetary policy regime. Such shocks also seem consistent with the first few months of high inflation starting in March 2021.

The breakdown in the relationship between inflation and the share of relative price increases suggests that expansionary monetary policy may be an important factor in the "pervasive" high inflation seen since October. But expansionary monetary policy itself can have two interpretations: It can represent temporary deviations from a stable regime, or it can represent a change in the regime.

It seems clear from Federal Open Market Committee (FOMC) communication that no change in regime is intended: The FOMC has a stated target of 2 percent inflation, and the Fed's latest Summary of Economic Projections indicates that FOMC members expect to conduct policy to return inflation to that target. In addition, the behavior of inflation compensation derived from nominal and inflation-indexed long-term Treasuries suggests that financial markets do not perceive a change in regime.

While the passage of time will reveal which interpretation is correct, the actual conduct of monetary policy will be the decisive factor.

Alexander L. Wolman is a vice president in the Research Department of the Federal Reserve Bank of Richmond.

1

These calculations are based on the most disaggregated breakdown of PCE categories that is publicly available.

2

The approximation and a detailed description of the measures are provided in an online appendix to my September article "How Broad-Based Is the Recent High Inflation?" These measures are motivated by the same facts and ideas as core inflation and trimmed mean inflation. However, they come at the issue from the other direction: Instead of adjusting overall inflation by eliminating the contributions of price changes that are large or come from particular categories, our measures focus on the contributions of large price changes to overall inflation.

3

See the 1999 paper "A Comparison of the CPI and the PCE Price Index (PDF)" or my 2011 article "K-Core Inflation" for an explanation of how actual PCE inflation is calculated. The first two columns of Table 1 provide information about the quality of the approximation.

4

The first two measures are constructed only for months with positive inflation rates. Note that the second measure was included in "How Broad-Based Is the Recent High Inflation?" That essay also discussed the inflation contribution from the highest 5 percent of price changes, where that contribution was "raw," not normalized as a share of inflation. Here, we instead discuss the normalized measure.

To cite this Economic Brief, please use the following format: Wolman, Alexander L. (March 2022) "Relative Price Changes Are Unlikely to Account for Recent High Inflation." Federal Reserve Bank of Richmond Economic Brief, No. 22-10.

This article may be photocopied or reprinted in its entirety. Please credit the author, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us