What Are Leading Indicators Telling Us About Economic Growth?

Macro Minute

May 31, 2022

For decades, economists have been hunting high and low for particular combinations of data — known as leading indicators — that can signal the future direction of the overall economy. That search has yielded numerous candidates that appear to have some statistical connection to future economic conditions. In today's post, we look at a few of these leading indicators and what they suggest for economic growth going forward.

"Like the 'check engine' light on a car, warning signs from leading indicators are not in themselves a reason to panic ..."

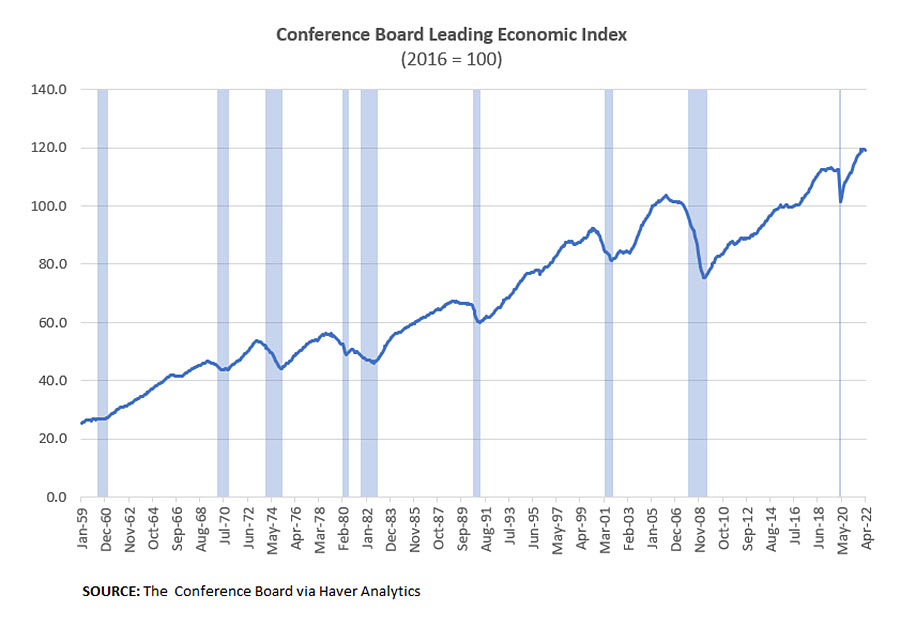

One of the most popular leading indicators is the Conference Board Leading Economic Index (LEI), which combines 10 underlying series, including average weekly hours in manufacturing, initial claims for unemployment insurance, new orders for capital goods and consumer confidence. Month-to-month changes in the index reflect a weighted average of month-to-month changes in the 10 underlying components.

According to the Conference Board, the LEI anticipates turning points in the business cycle by about seven months. Declines in the index suggest softening in future economic activity. However, there are many instances where the LEI has provided "false positives" for recession risk, falling on a monthly basis — sometimes significantly, as in the case of a 1.8 percent decline in January 1996 — without a subsequent corresponding recession.

Figure 1 below shows that the LEI generally tracks downward before a recession. In the latest reading from April, the LEI dropped 0.3 percent to 119.2, following three straight months of increases. Despite the latest drop — which was mild in comparison to the 1.3 percent average drop at the onset of recessions since 1959 — the LEI does not seem to be giving a strong signal of an impending downturn in growth based on visual inspection.

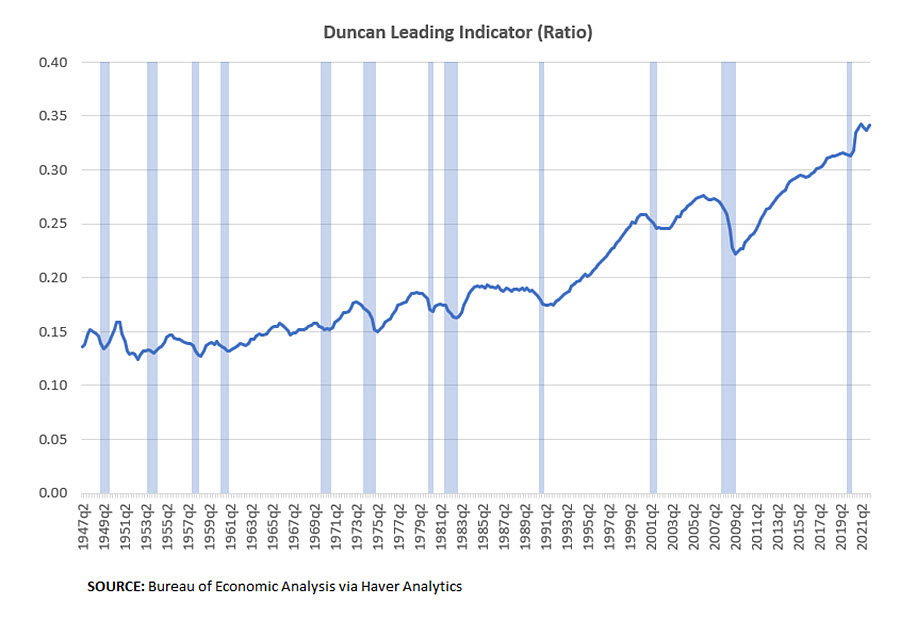

A second leading indicator we explore is the Duncan Leading Indicator (DLI), which is the ratio of real durable goods spending and fixed investment to real final demand. The DLI has been found to hit a peak about four quarters before a recession, on average. In its most recent reading, the DLI rose to 0.342 in the first quarter of 2022 from 0.337 in the fourth quarter of 2021 and does not yet seem to be peaking.

There was a "local" peak in the second quarter of 2021, as the reading of 0.343 was above the readings of both the preceding quarter and subsequent quarter (0.340 and 0.339, respectively). However, as shown in Figure 2 below, the DLI can sometimes give a false positive for a recession over the next year: The index has hit local mini-peaks on several occasions without a recession happening over the next year.

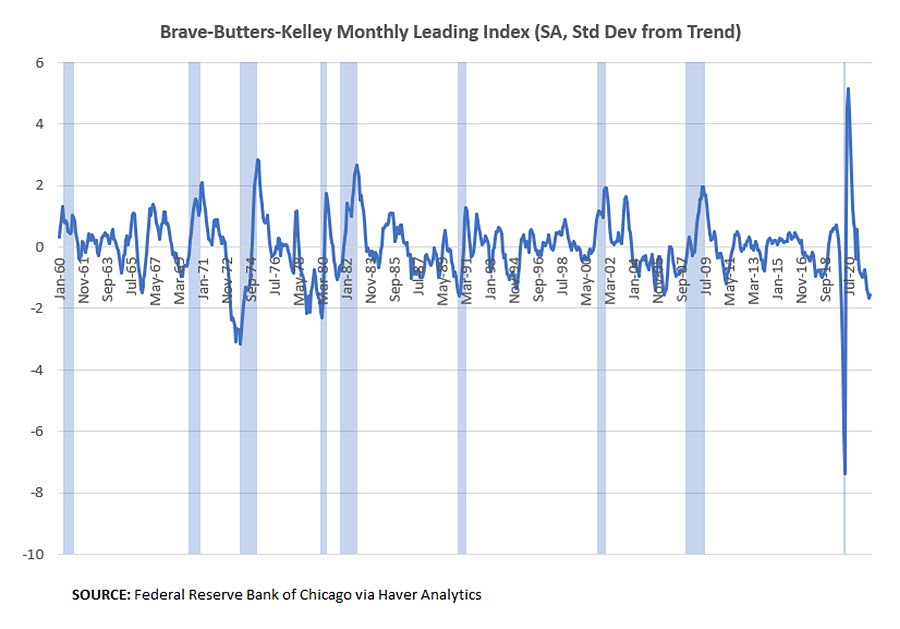

The final series we look at is the Brave-Butters-Kelley Leading Index (BBKLI) published by the Federal Reserve Bank of Chicago. Of the three leading indicators covered here, the BBKLI uses information from the largest set of underlying data, applying dynamic factor analysis (a technique that extracts common underlying factors from big datasets) to 500 monthly macroeconomic time series dating back to 1960. According to the authors, the index has "predictive power for business cycle fluctuations that is roughly on par with that of the Conference Board Leading Economic Index for the U.S."

Values of the BBLKI below −1 have historically tended to signal an elevated likelihood of a recession 10 months hence. In contrast to the other two leading indicators, the BBLKI is currently flashing warning lights for economic growth. In March, the BBLKI registered −1.6, the fourth straight month the index has been below the −1 threshold.

Like the "check engine" light on a car, warning signs from leading indicators are not in themselves a reason to panic, but instead a signal that more information is needed. The figures show that leading indicators can suggest looming recessions that don't actually materialize. Furthermore, the indicators are based on data that are subject to revision, so the latest reading is never the final word on the state of the economy.

The main message stemming from these mixed signals may simply be that the economy continues to be plagued by a high degree of uncertainty. Meanwhile, the quest for a more perfect leading indicator continues to this day with ongoing efforts to incorporate new data sources and analytical methods.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us