Update on Trimmed Mean Inflation

Macro Minute

July 12, 2022

May's personal consumption expenditure (PCE) report showed month-over-month core inflation was more modest than the headline measure. But an alternative measure of core inflation suggests little relief in underlying inflation.

In the May report, headline PCE inflation was 0.6 percent monthly and remained at a 6.3 percent year-over-year rate. Core PCE prices rose 0.3 percent monthly for the fourth straight month, while the year-over-year core inflation rate dropped to 4.7 percent in May from 4.9 percent in April.

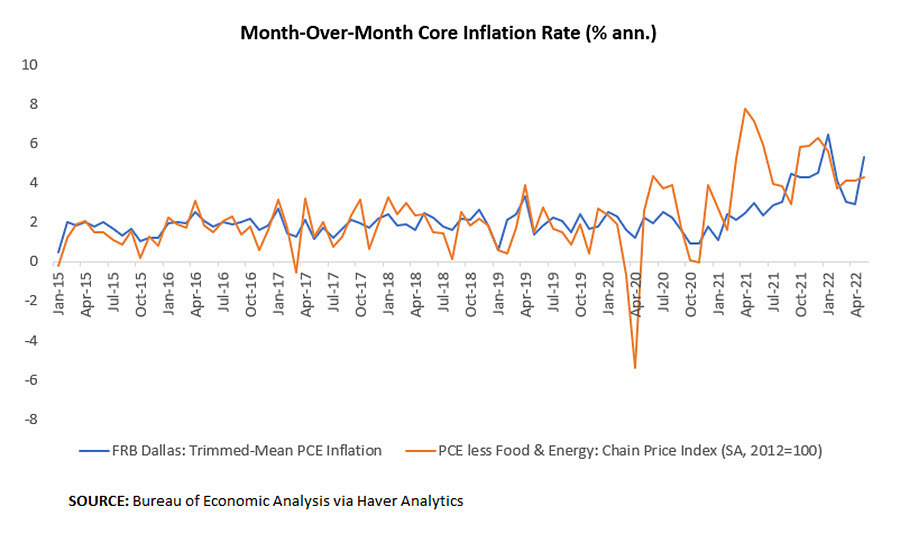

However, trimmed mean PCE — which we discussed in our previous post on this inflation measure — suggests monthly underlying inflation has yet to cool. Trimmed mean PCE inflation grew 5.3 percent annualized in May versus 2.9 percent annualized in April. The 12-month trimmed mean rate rose from 3.8 percent in April to 4 percent in May, the highest reading since October 1990. Figure 1 below compares month-over-month annualized changes in trimmed mean PCE inflation versus the official core PCE inflation measure.

In addition, the composition of trimmed mean PCE continues to send warning signs for underlying inflation in May. The (consumption-weighted) share of trimmed mean PCE with prices rising faster than 10 percent annualized rose to 23.6 percent in May, up from 18.7 percent in April.

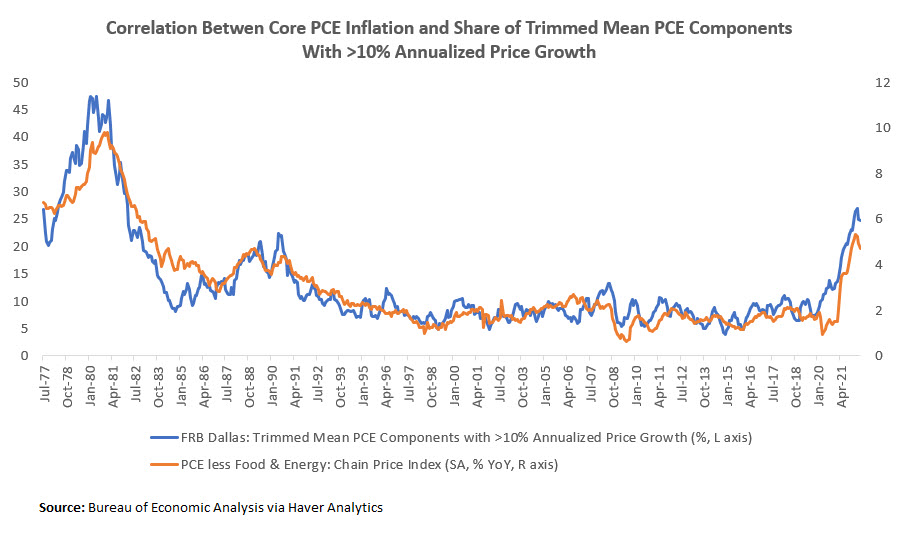

In our previous post on trimmed mean inflation, we showed that this measure has displayed a strong correlation with core PCE inflation from 1977 through today. Figure 2 below plots year-over-year core PCE inflation on the left axis versus a six-month moving average of the share of trimmed-mean PCE with price increases greater than 10 percent.

The correlation between the two metrics is 0.93. In May, the six-month moving average share was 24.6 percent, down only slightly from April's reading of 24.9 percent.

The continued high level of the six-month moving average share is another symptom of inflationary pressures not yet falling meaningfully following a 25-basis-point increase in the fed funds rate in March and a 50-basis-point increase in May. This highlights the view expressed in the Statement on Longer-Run Goals and Monetary Policy Strategy that monetary policy actions tend to influence prices with a lag.

Contact Us