Real-Time Signs of Cooling Labor Demand

Macro Minute

August 9, 2022

Job openings have been a very stark signal of labor market tightness in recent months, with Federal Reserve Chair Jerome Powell referencing historically elevated levels of job openings at the last six Federal Open Market Committee press conferences. But some signs may be pointing to that tightness starting to ease.

Last week, the Bureau of Labor Statistics (BLS) announced that June job openings declined to 10.7 million from 11.3 million in May, with the job openings rate falling to 6.6 percent compared to 6.9 percent in May. For every unemployed person, 1.8 jobs were available, falling from a ratio of 1.9 job openings per unemployed person in the previous month.

"Are we on track for a sustained decline in labor demand?"

Are we on track for a sustained decline in labor demand? If so, where and how rapidly is employer demand for workers cooling? As we discussed in an earlier blog post ("Strong Start for Job Openings in 2022"), high-frequency data can provide real-time information about labor market developments and appears useful in indicating turning points in the economy during the depth of the pandemic.

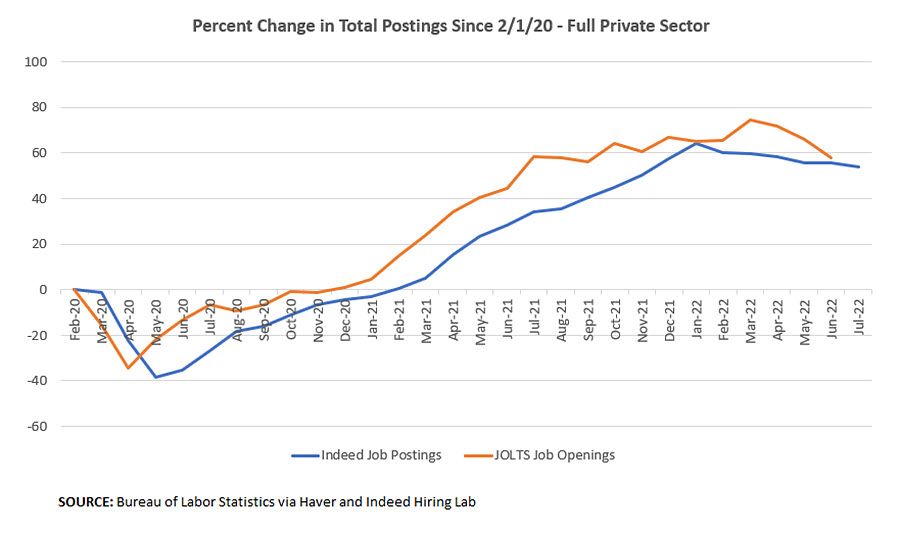

Figure 1 below plots high-frequency job postings data from Indeed Hiring Lab against the official BLS job openings estimate from the Job Openings and Labor Turnover Survey (JOLTS). The figures show that the high-frequency data have followed broad trends in the official series relatively well since the start of the pandemic. The latest observations suggest that job openings in July fell further from June levels, indicating June may have been just the start of an expected cooling in labor demand.

While month-over-month declines in the high-frequency data don't always perfectly translate to month-over-month drops in job openings from JOLTS, mean reversion following the pandemic-related growth spurt makes it more likely that the recent high-frequency developments will eventually be reflected in the official BLS numbers.

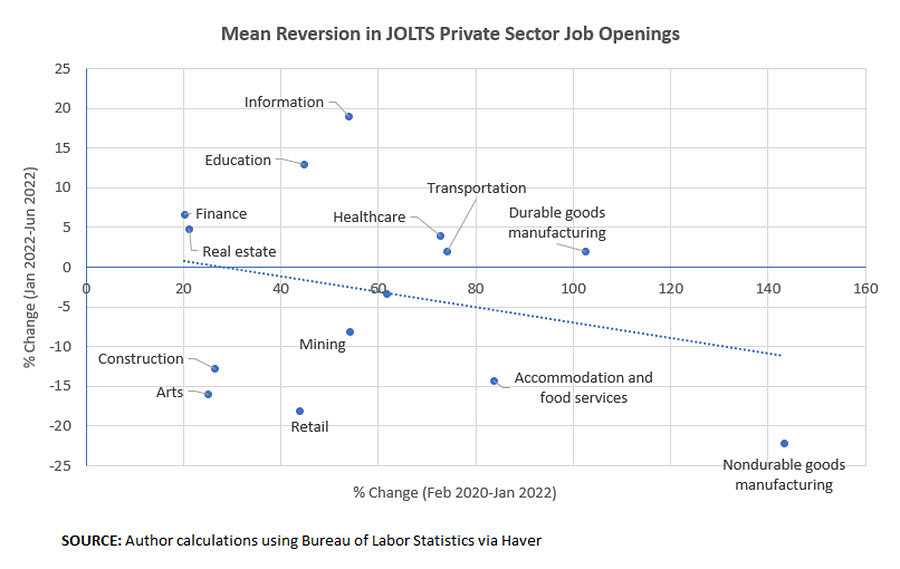

In Figure 2 below, we show a scatter plot of 16 private sector industries broken out in the JOLTS report. On the X-axis, we show the percentage increase in job openings from February 2020 to January 2022, while the Y-axis represents the subsequent change from January 2022 to July 2022.

If the current decline in job postings mainly reflects mean reversion, we'd expect to see a negative relationship between the two, with the sectors that experienced the most dramatic increases in job vacancies in 2020 and 2021 seeing the biggest declines over 2022. As shown in Figure 2 above, there seems to be some evidence for mean reversion.

On average, for every 1 percentage point increase in job openings between February 2020 and January 2022, we see a subsequent 0.1 percent decline in postings over the first half of 2022. Notably, postings in the nondurable goods manufacturing, accommodation and food services, and retail sectors were temporarily elevated by pandemic shortages and are among those seeing the largest declines in vacancies so far in 2022.

But some sectors appear to be outliers. The health care, information and education sectors continue to see increases in job vacancies over the course of 2022. This points to an uneven adjustment process for labor demand. Some industries are continuing to feel squeezed for workers, while other industries are now starting to cut back on hiring.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us