A CPI Basket Case

Macro Minute

February 28, 2023

How can a plethora of individual price changes in the economy be combined into a single number that represents the overall change in the cost of living? When building the Consumer Price Index (CPI), the Bureau of Labor Statistics (BLS) accomplishes this by figuring out (via consumer spending surveys) what a representative basket of consumer goods and services looks like. Notably, as consumer spending patterns change, the composition of this basket changes over time.

In January, the BLS announced two changes to its CPI basket. These included: (1) a change in the weights to reflect year 2021 consumption patterns — updating from the prior weights based on 2019-2020 patterns; and (2) increasing the frequency of these updates to annual versus every two years.

More frequent updates to the CPI basket can provide a more accurate picture of inflation, which is one reason why the Fed prefers to measure inflation with the Personal Consumption Expenditures (PCE) price index, where weights vary from month to month. The chained CPI is another such index that features varying weights. In contrast to the PCE and chained CPI, the CPI's fixed-weight approach can give an outdated view of spending patterns. According to the BLS, estimates of current inflation calculated with outdated spending weights tend to be higher than inflation estimates calculated with more current spending weights, because in theory, consumers tend to substitute away from goods and services that become relatively more expensive toward those that become relatively cheaper.

Still, the CPI remains closely watched and popularly cited. The CPI's fixed-weight approach means that historical CPI data are not revised, in contrast to varying weight approaches, which can induce revisions. As the oldest of the main price indexes in use, the CPI also forms the basis of many formal inflation-indexing arrangements such as for federal income tax brackets, Social Security cost-of-living adjustments, and private sector cost-of-living adjustments.

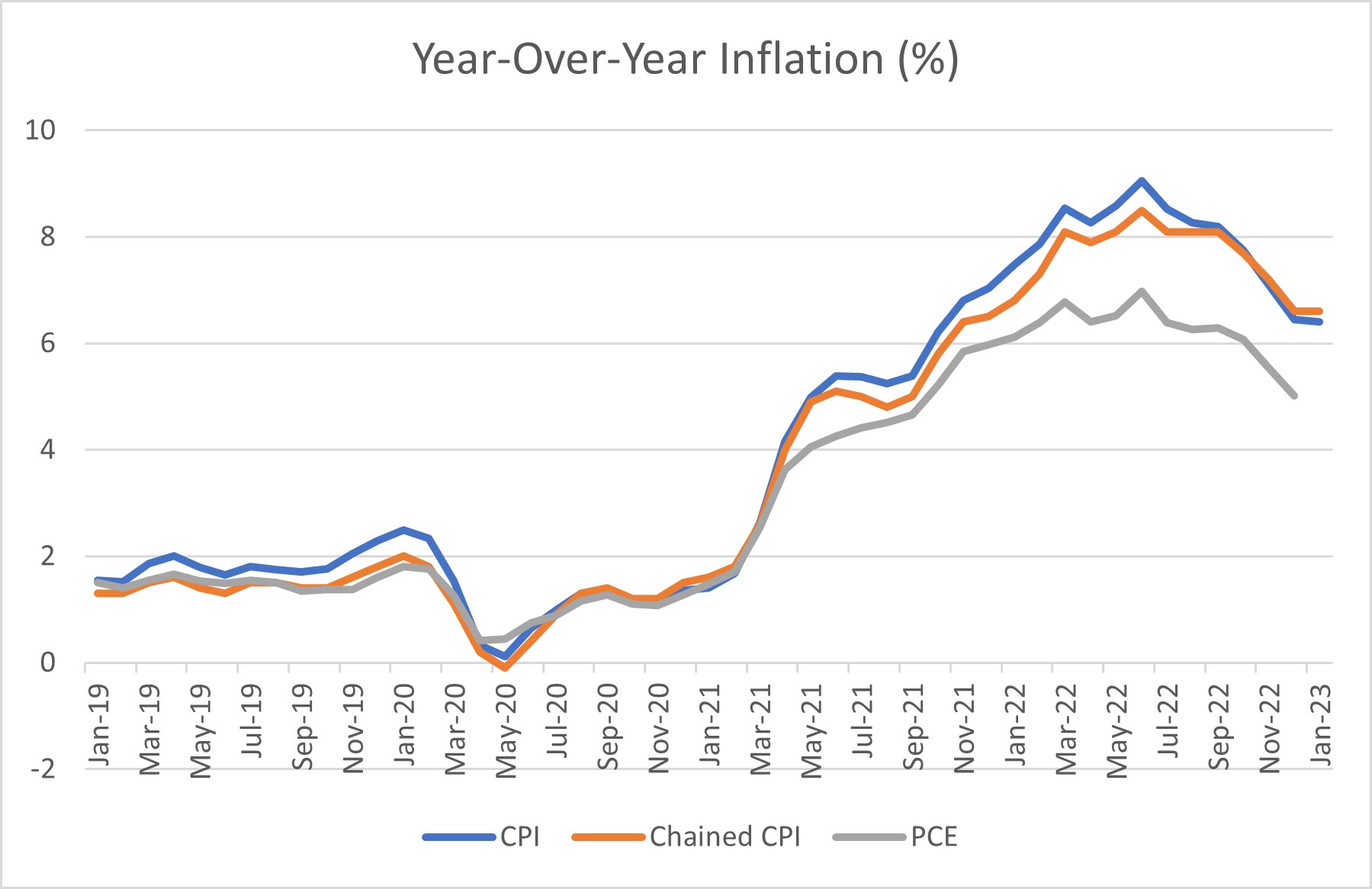

How much does the issue of fixed- versus varying-weight matter in terms of representing inflation? Figure 1 below compares year-over-year inflation in headline CPI, chained CPI, and the PCE price index since 2019. Headline CPI inflation has closely tracked chained CPI inflation, suggesting that the issue of consumer substitution toward cheaper alternatives may not be as important as one might think. From 2010 through 2019, headline CPI inflation was only 0.26 percentage points higher than chained CPI inflation. But it is true that the chained CPI was almost uniformly lower than headline CPI.

Figure 1 below suggests that the much larger gap between CPI inflation and PCE inflation is not driven primarily by the difference between fixed and varying weights, but rather by differences in product coverage across the two indexes. The PCE includes a much larger scope of goods and services consumed by households, including those bought on behalf of households like employer-provided health care.

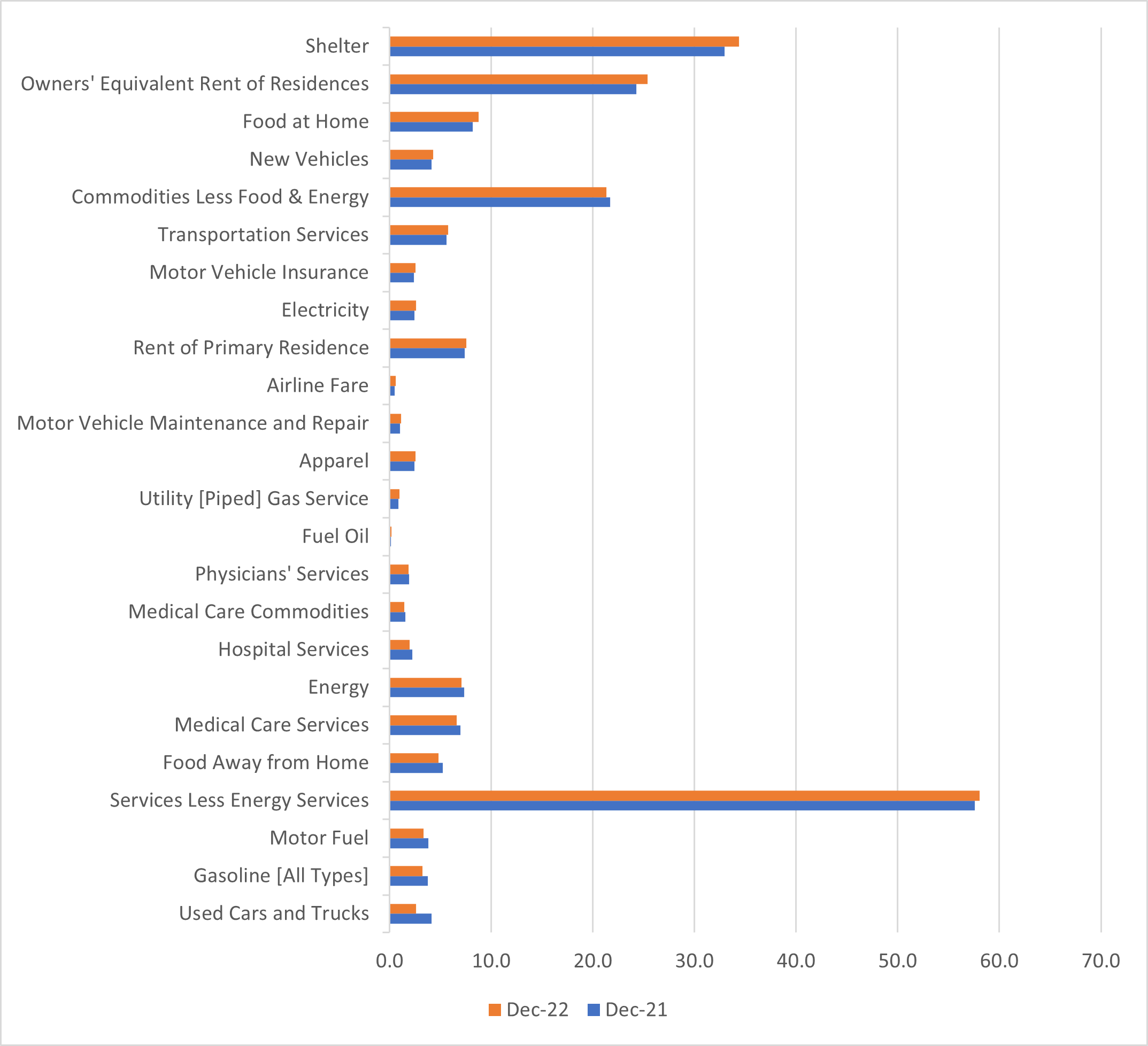

January's updates to the CPI basket suggest the impact of newer weights on inflation is small. The CPI release reports "relative importance" weights associated with each expenditure category. These ratios show approximately how the urban United States distributes its spending among CPI components. Figure 2 below compares a selection of relative importance weights used in the January 2023 CPI release (which uses average 2021 spending) to the older weights which rely on average 2019-2020 spending. While there are differences between the two sets of weights, the updates are minor, with the relative importance of many categories changing by less than a percentage point.

The BLS also provides a comparison of January month-over-month price growth under the new and old weights. A selection of these is shown in Table 1 below. At the headline level, month-over-month growth rates of CPI are similar using both weighting schemes at about 0.8 percent month-over-month growth (prior to seasonal adjustment).

Furthermore, the idea that updated weights will result in a lower estimate of inflation by accounting for substitution does not appear to hold in this revision: The monthly growth of core CPI increases to 0.62 under the new weights versus 0.53 under the old weighting. At the item level, the direction of the change in new vehicles price index flips from negative to positive under the new weights, while monthly growth in the price index for utilities is more moderate. For used vehicles, which saw dramatic price increases due to a combination of low auto supply and high demand during the pandemic, the switch from old weights to new weights makes no difference in the estimate of price growth.

| Table 1: Comparison of Selected CPI-U, U.S. City Average 1-Month Percent Changes Using Old (2019-2020) Weights and New (2021) Weights | |||

|---|---|---|---|

| Series Title | CPI-U 1-month NSA percent change, new (2021) weights | CPI-U 1-month NSA percent change, old (2019-2020) weights | Difference in percent changes |

| All items | 0.8 | 0.763 | 0.037 |

| Food and Beverages | 0.714 | 0.702 | 0.012 |

| Food at home | 0.784 | 0.776 | 0.008 |

| Food away from home | 0.616 | 0.598 | 0.018 |

| Energy | 3.053 | 3.355 | -0.302 |

| Gasoline (all types) | 3.15 | 3.351 | -0.201 |

| Electricity | 2.295 | 2.292 | 0.003 |

| Utility (piped) gas service | 6.621 | 7.708 | -1.087 |

| All items less food and energy | 0.616 | 0.529 | 0.087 |

| Housing | 0.973 | 1.024 | -0.051 |

| Shelter | 0.741 | 0.748 | -0.007 |

| Apparel | 2.639 | 2.471 | 0.168 |

| Recreation | 0.68 | 0.707 | -0.027 |

| Education | 0.116 | 0.117 | -0.001 |

| Communication | 0.395 | 0.4 | -0.005 |

| Medical Care | 0.076 | 0.054 | 0.022 |

| Hospital Services | 0.5 | 0.538 | -0.038 |

| Physicians' Services | -0.1 | -0.363 | 0.263 |

| Prescription Drugs | 2.095 | 2.11 | -0.015 |

| Transportation | 0.735 | 0.479 | 0.256 |

| New Vehicles | 0.461 | -0.311 | 0.772 |

| Used Cars and Trucks | -1.592 | -1.592 | 0 |

Source: Bureau of Labor Statistics

This basket breakdown might bring a bunch of bad news. Perhaps buyers haven't been shopping around for bargains as frequently during this period of high inflation because they're expecting prices are going to be similarly high everywhere. Price setters might exploit this inelasticity to keep prices higher for longer. Maybe buyers aren't shopping around because they're afraid prices will rise further if they delay their purchase. If so, inflation expectations could take longer to fall to levels more consistent with the Fed's target. But January is just one month of data: Time will tell if savvy shopping can make a comeback, yielding more savings to households.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us