Are Retail Inventories Back to Normal?

Macro Minute

June 20, 2023

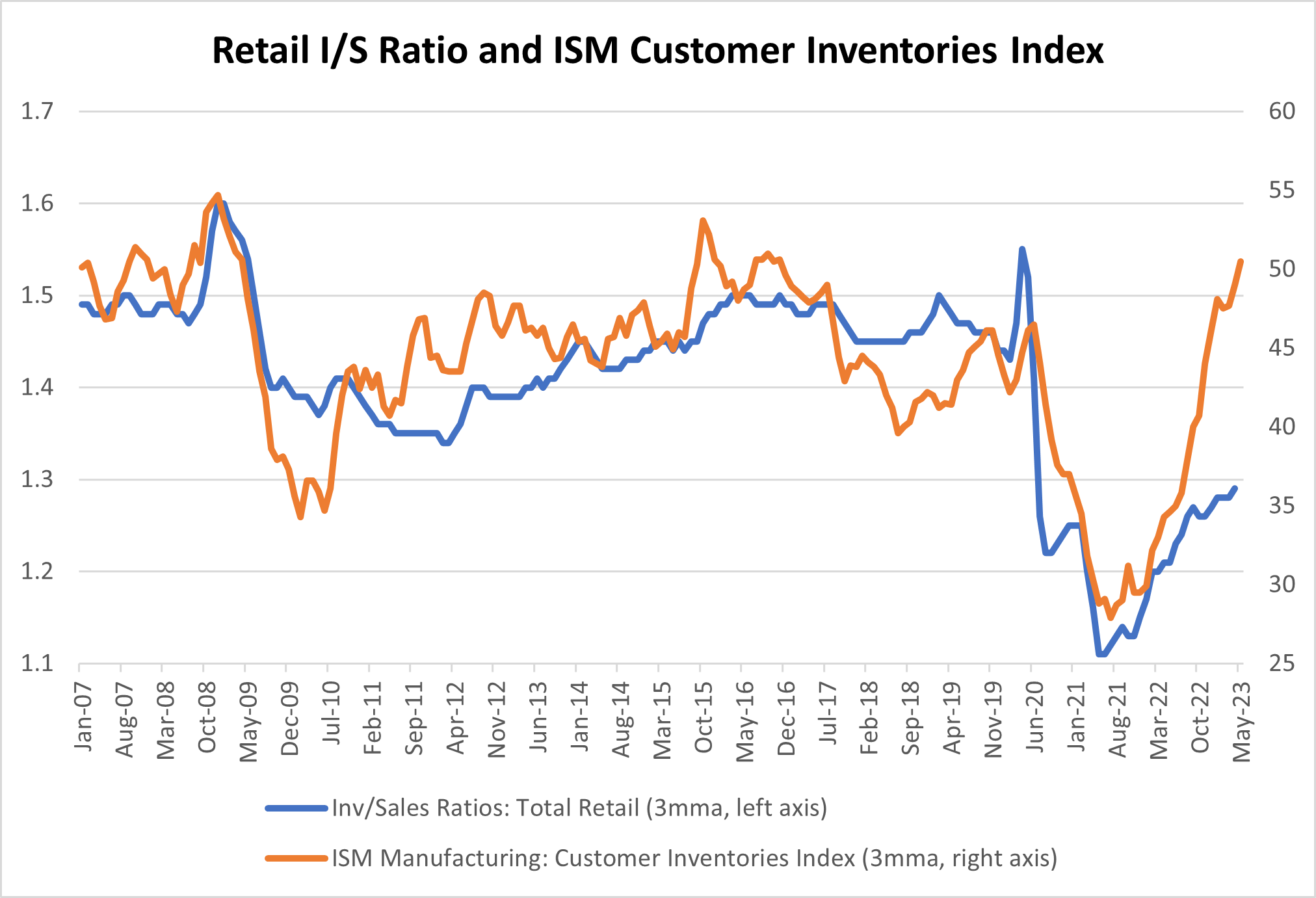

The economy seems to have weathered supply chain disturbances and come out on the other side: In the latest ISM Manufacturing Survey, respondents indicated that customer inventories were roughly in balance, with the survey producing a score of 50.5 in May. (A score of 50 indicates the proportion of respondents indicating inventories were too high roughly equaled the proportion saying inventories were too low.) But at the same time, retail inventory-to-sales ratios remain lower than pre-pandemic levels, as seen in Figure 1 below. In this week's post, we look at the data to see which businesses are driving this picture of lean inventories relative to sales.

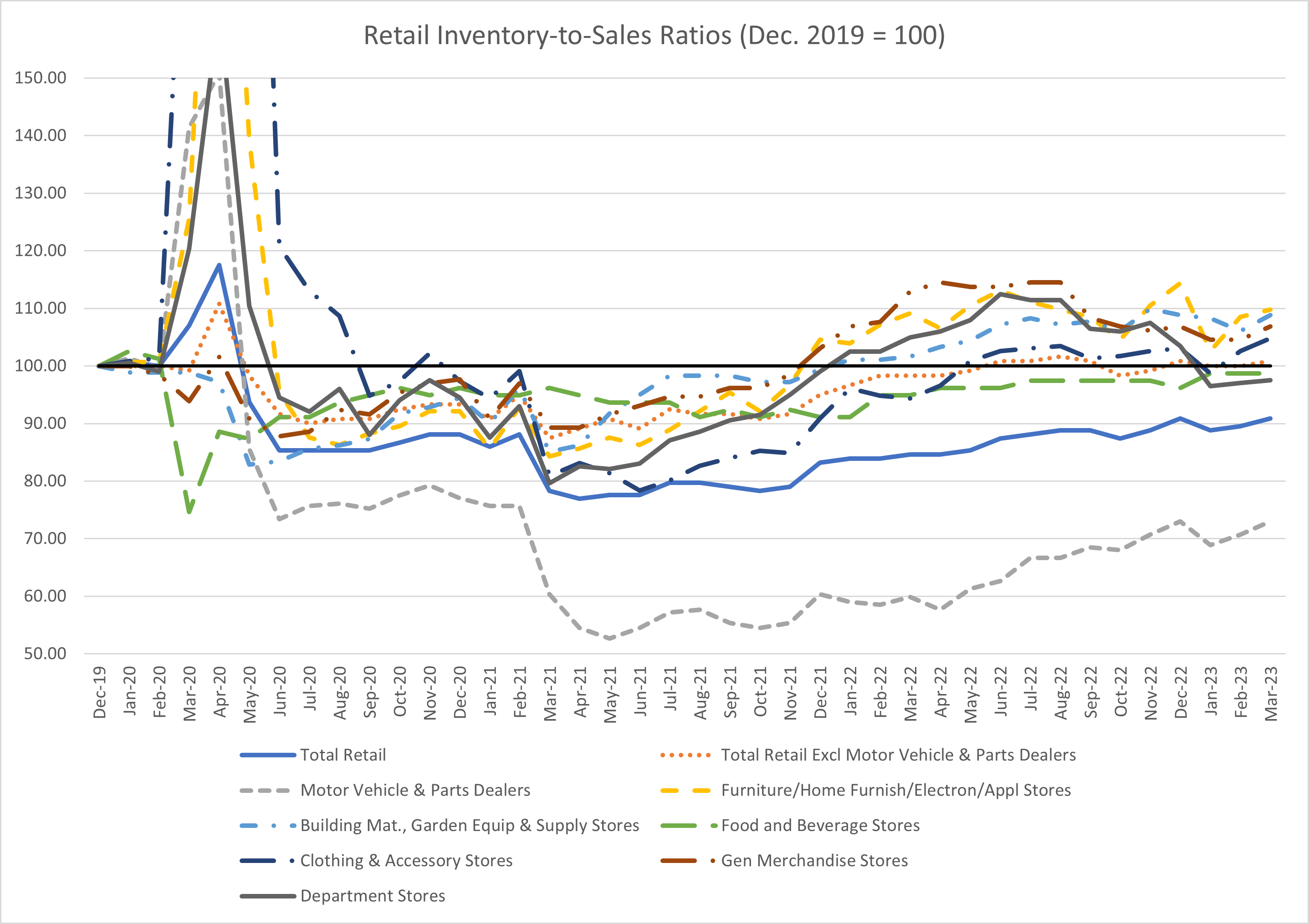

Figure 2 below plots inventory-to-sales ratios by type of retailer, normalizing pre-pandemic (December 2019) levels to 100. Looking across retailer types, most inventory-to-sales ratios are back up to or ahead of pre-pandemic levels, and food and beverage stores and department stores are just barely below their pre-pandemic benchmarks. Figure 2 shows that the decline in the aggregate retail inventory-to-sales ratio versus pre-pandemic levels appears to be largely driven by motor vehicle and parts dealers. In contrast, the broad index of retail inventory-to-sales excluding motor vehicles and parts dealers is essentially equal to its December 2019 level.

The previous figure suggests that the lower aggregate retail inventory-to-sales ratio is mostly being driven by the automotive sector. However, the data in Figure 2 don't account for inflation. Prices matter in assessing inventory levels: In principle, the Census Bureau allows companies flexibility in the methods they use to value their inventories and notes that "methods of valuation may vary according to the accounting practices of each firm." The recent experience of high inflation, supply-chain issues and idiosyncratic price jumps may have also created challenges for retail businesses keeping track of the prices they paid to acquire goods from wholesalers. From a business perspective, most firms likely only care about their own accounting practices and thus focus on the nominal inventory-to-sales ratio.

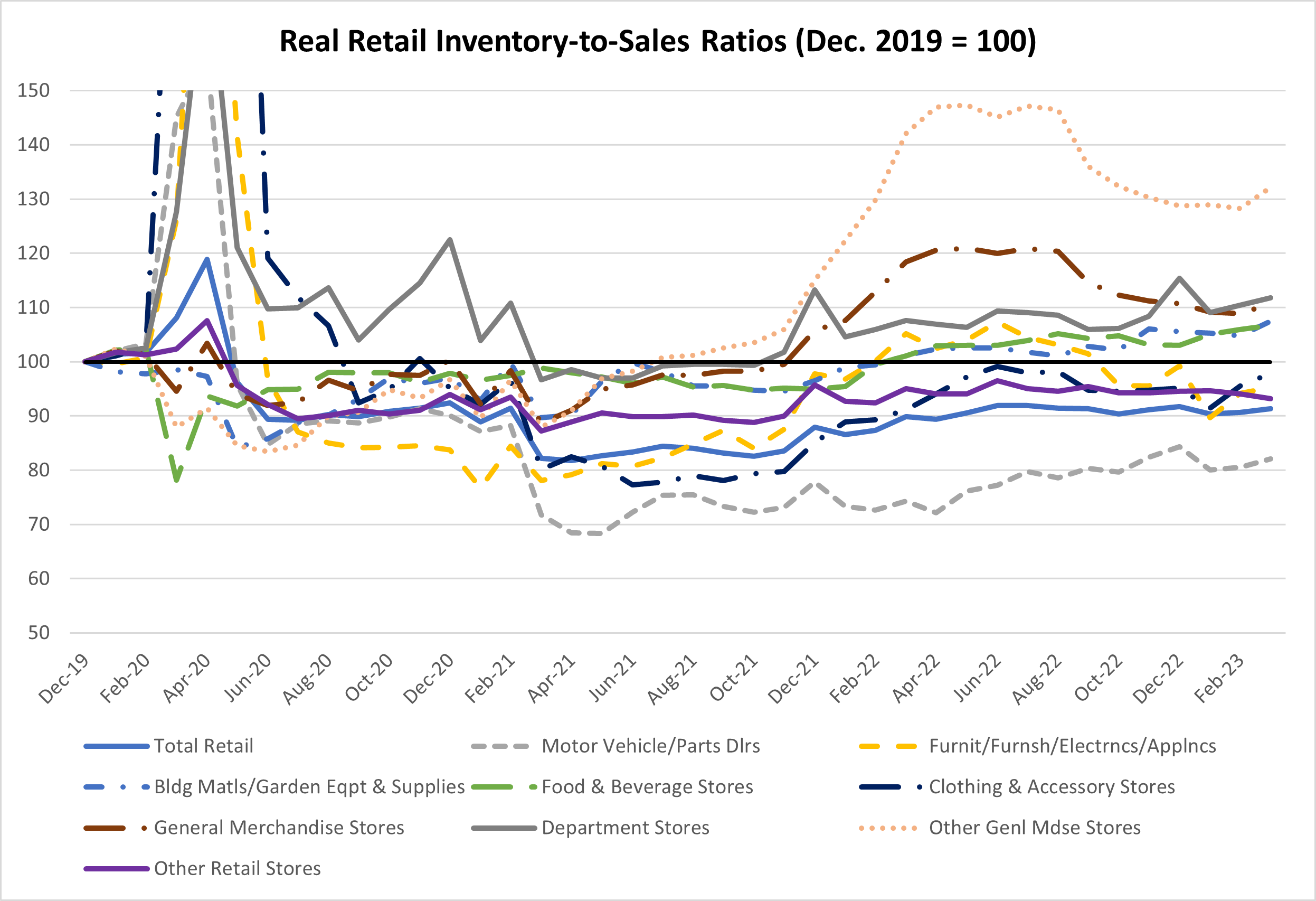

But when aggregating companies' data to produce figures like real GDP, the Bureau of Economic Analysis adjusts inventories for inflation. When looking at inflation-adjusted data, other retail businesses are found to have lower real inventory-to-sales ratios relative to their immediate pre-pandemic levels. Figure 3 below reveals that — along with motor vehicle and parts dealers — furniture, furnishings, electronics and appliance stores, clothing and accessory stores, and other retail stores have also been operating leaner on inventories when inflation-adjusted data are taken into account.

Between the nominal ratios in Figure 2 and the real ratios in Figure 3, which set of data gives the most accurate representation of retail inventories? Previous research has suggested that the real, inflation-adjusted series is best when making comparisons over time, as the nominal ratio can be affected by relative price changes. While these distortions are most troublesome at higher levels of aggregation, large relative price changes have been a prevalent feature of the post-COVID-19 pricing environment and could create similar distortions even when looking within a more disaggregated category.

Based on the real inventory-to-sales ratios, several kinds of retail operations are operating more leanly compared to before the pandemic. It remains an open question whether this reflects a new normal or lingering challenges of earlier supply constraints. If it's the latter case, the manufacturing outlook may be brighter than manufacturing surveys suggest, as retailers look to rebuild their stocks.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us