Savings Still High, but Not for All Households

Macro Minute

June 27, 2023

Household savings have been a tailwind to spending and inflation, but is that tailwind finally dissipating? On June 16, the Federal Reserve Board of Governors released the latest Distributional Financial Accounts, which allow us to gauge the state of household savings and wealth through the first quarter of 2023. We find that household liquid assets generally remain elevated compared to pre-pandemic levels, but levels and trajectories differ across income categories.

To measure savings, we focus on liquid assets, which are the component of household net worth that can be easily converted to cash. (This is in contrast to other forms of wealth like housing and long-term investments locked up in retirement accounts, which can't be easily spent.) We define liquid assets as the sum of deposits, government and municipal securities, and money market fund shares.

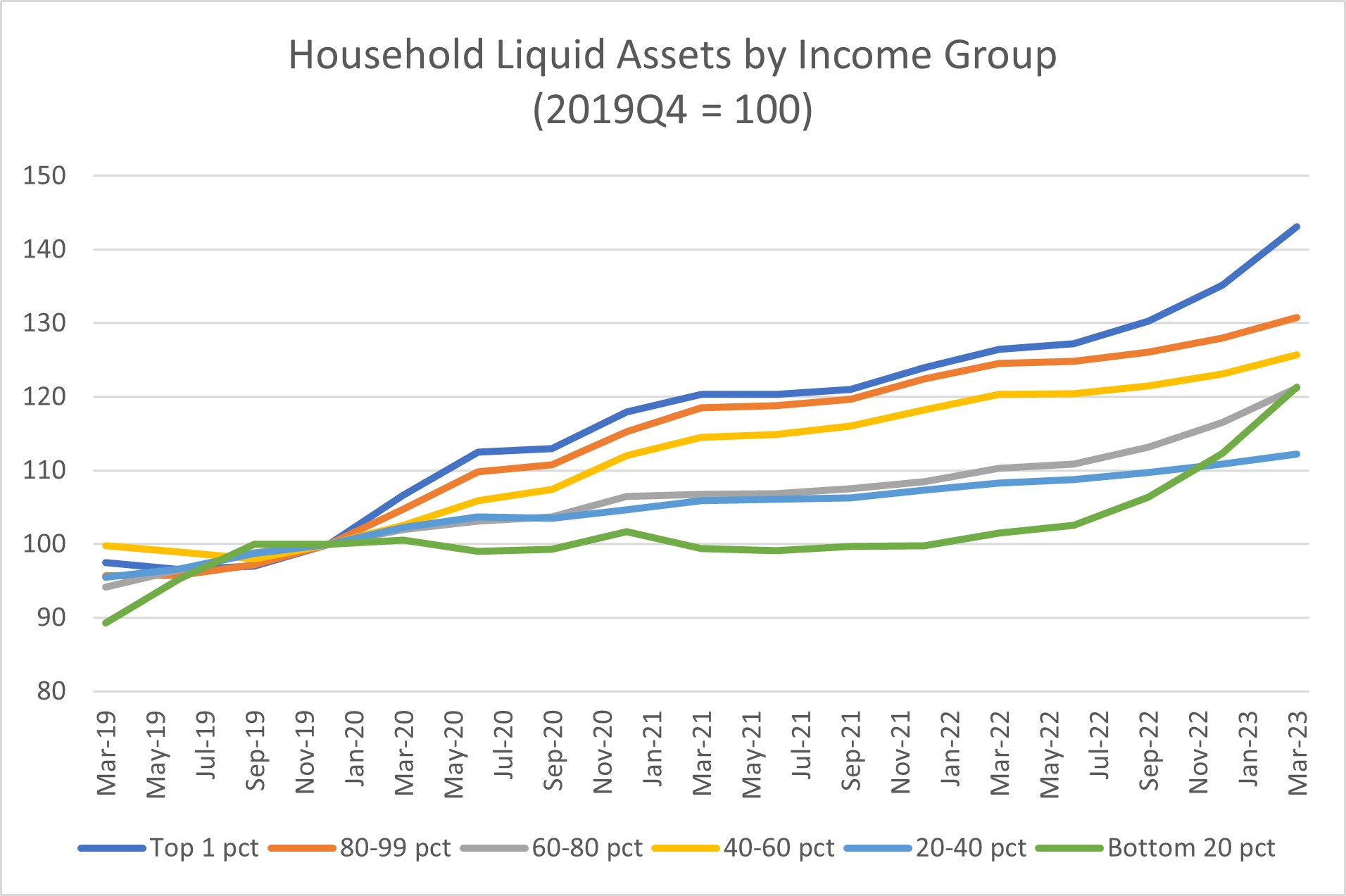

Figure 1 below shows nominal liquid assets by household income group, normalized to equal 100 in the fourth quarter of 2019 as a pre-pandemic baseline. Across the income distribution, liquid assets have increased versus the pre-pandemic baseline. The largest increase accrued to the top 1 percent of households, where liquid assets are up more than 40 percent versus the pre-pandemic baseline. Lower-middle-income households (the 20th to 40th percentile of households) have seen the smallest increase in liquid assets, rising by just over 10 percent since the start of the pandemic.

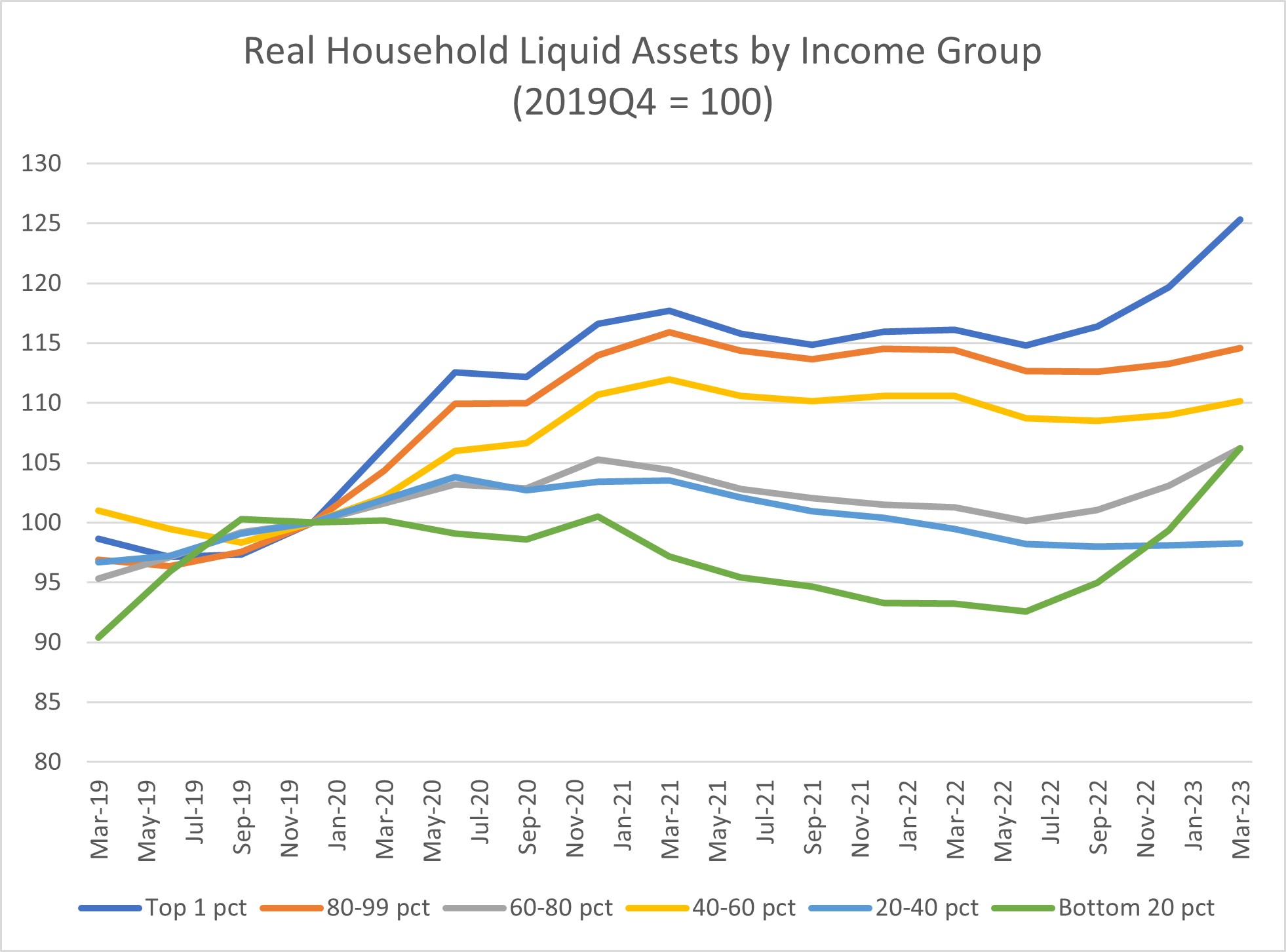

However, while nominal liquid assets may have risen across the income spectrum, prices are higher as well. Figure 2 below adjusts household liquid assets for inflation as measured by the personal consumption expenditure price index. The picture is similar to Figure 1: The largest gains in real liquid assets have accrued to the households earning the highest incomes. However, after adjusting for inflation, we can see that liquid assets for households in the 20th to 40th percentile of income are lower than the pre-pandemic baseline and have been flat for the past year.

The pre-COVID-19 fourth quarter of 2019 level might not be a good benchmark if what households care about is how much they save relative to what they make. Incomes have grown over the pandemic, and it's possible that savings have fallen relative to incomes, making some households feel worse off in relative terms.

In the next figure, we attempt to normalize nominal household liquid assets by income for each income group. To estimate quarterly income by income group, we combine data on the distribution of usual weekly earnings of full-time wage and salary workers from the Bureau of Labor Statistics with data on the number of households in each income group from the Distributional Financial Accounts.

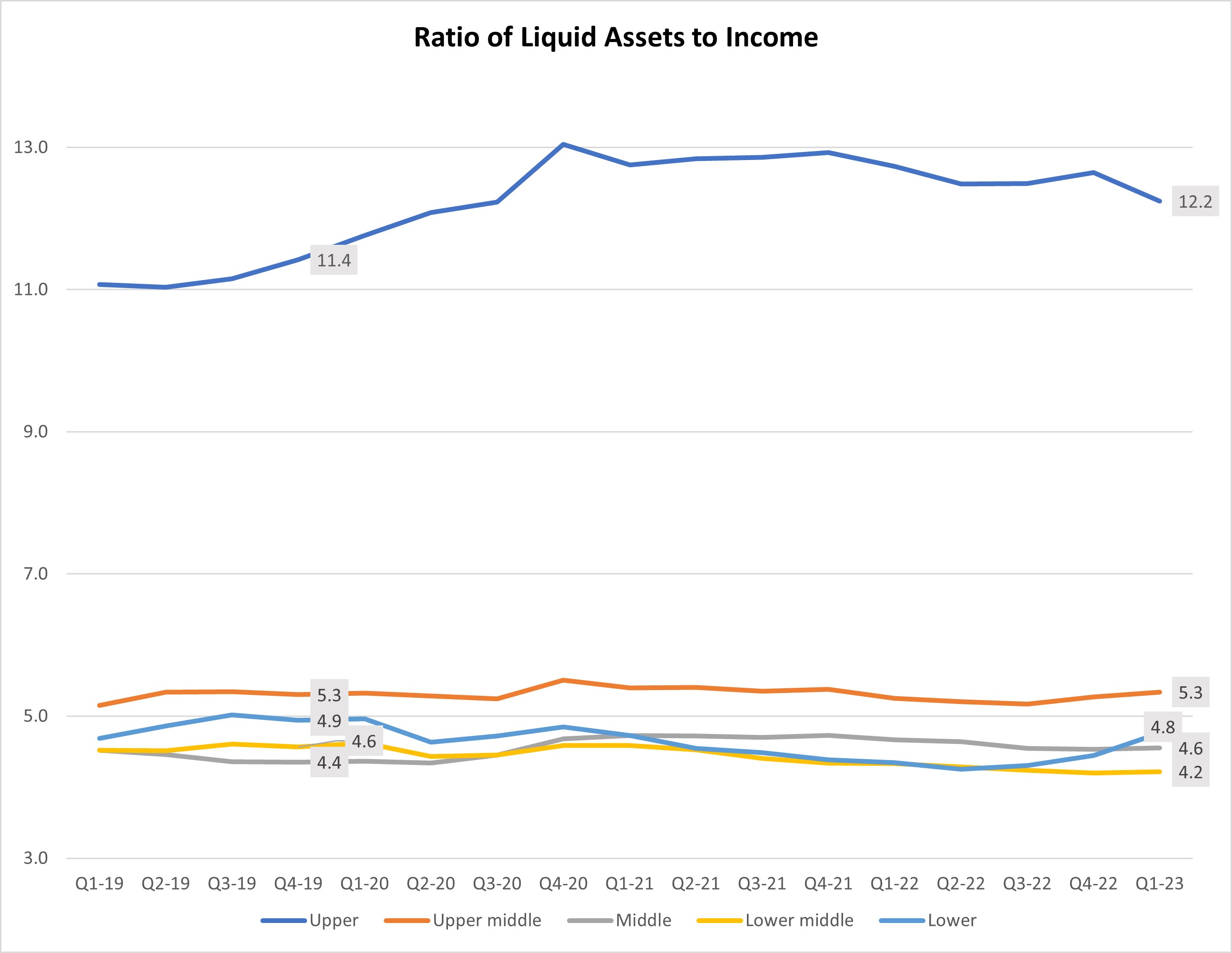

In Figure 3 below, the "Upper" group refers to liquid assets for households in the 80th to 99th percentile, divided by the group's estimated income, where we assume households in the group earn the usual weekly earnings of the 90th percentile of full-time wage and salary workers. Similarly, the ratio for the "upper middle" divides liquid assets of the 60th to 80th percentile by quarterly income for workers in the 75th percentile; the "middle" group matches the 40th to 60th percentile with median (50th percentile) usual weekly earnings; and so on.

We then compare how the savings of each group changed from the fourth quarter of 2019 to the first quarter of 2023. Savings are elevated for upper-income households, where the ratio of liquid assets to income increased from 11.4 in the fourth quarter of 2019 to 12.2 in the first quarter of 2023. For households with income in the upper-middle range, the ratio of savings relative to income stayed the same at 5.3. For middle-income households, the ratio of savings to incomes rose from 4.4 to 4.6. Lower-middle-income households saw a decline from 4.6 to 4.2, and lower-income households saw the ratio fall from 4.9 to 4.8.

Our analysis shows that household savings as measured by liquid assets remain elevated through the first quarter of 2023, except for households toward the lower end of the income distribution. In particular, for lower-middle-income households, real liquid assets are below pre-pandemic levels, and the ratio of liquid assets to income fell by the most of all the income categories we examine. Though the tailwinds to consumer demand from savings continue to blow in the economy for most households, the winds may have died down for households earning the least.

Note for our readers: Macro Minute will be taking the next week off for Independence Day.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us