Digging Into Construction Data

Macro Minute

January 16, 2024

In this week's post, we dig into an important input into GDP and a barometer of investment sentiment: the monthly Construction Spending Report — also referred to as the Value of Construction Put in Place (VIP) Report — produced by the U.S. Census Bureau. The VIP survey provides monthly estimates of the dollar value of construction work done in the United States, covering private residential and nonresidential construction as well as public construction. The data are collected mostly from a monthly mail-in survey of a sample of privately owned nonresidential, state and local, and federal projects, while estimates of residential construction and home improvement spending are obtained from the Census Bureau's Survey of Construction and Bureau of Labor Statistics' Consumer Expenditure Surveys, respectively.

"Construction" refers to new buildings and structures, additions, repairs, renovations, site-related structures such as sidewalks and water supply lines, and site-specific equipment such as boilers and storage tanks. The reported dollar amounts capture costs of materials and labor; contractors' profits; costs of architectural and engineering work; overhead costs; and other fees, interest and tax costs paid during construction. Focusing on private construction, total spending is broken down into residential and nonresidential spending. Residential spending is further disaggregated into single-family, multifamily and improvements, while nonresidential spending is disaggregated into 11 categories including office, commercial (including retail, wholesale and selected service industries), health care and manufacturing.

These data are tracked by economy watchers for several reasons. Construction spending on new projects can provide a useful barometer of current investment sentiment and the tightness of current financial conditions. Additionally, because construction projects can last for many years, willingness to spend on new projects today can reveal builders' optimism about the future. Construction spending estimates are also the main input in calculating private fixed investment in structures for GDP accounting. Over the past five years, private fixed investment in structures has accounted for 7.1 percent of nominal GDP, while government investment in structures — which also uses data from the VIP report — has accounted for 1.6 percent of GDP over the same period.

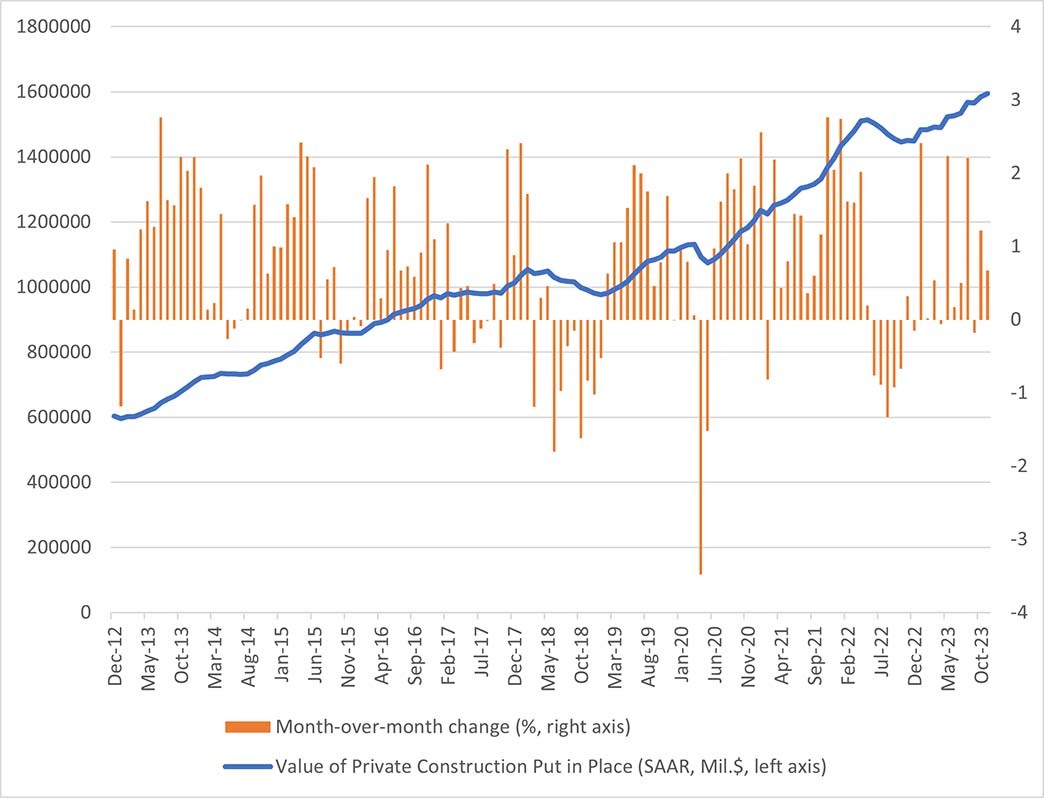

Figure 1 below shows the value of total private construction put in place from the VIP report. In November, private construction spending rose 0.7 percent month over month (slowing from an October growth rate of 1.2 percent) and is up 10 percent over a year ago (versus being up 9.6 percent year over year in October).

Adjusting the nominal spending figures (such as the series shown in Figure 1) for inflation can be a tricky exercise. We follow the Bureau of Economic Analysis (BEA) methodology of matching VIP entries with price deflators. Some entries, such as office and health care construction, have directly corresponding producer price indexes (PPIs) for construction that can be used to convert to constant-dollar amounts. Other line items are associated with a closely related PPI index: For example, the PPI for warehouses serves as a multitasking deflator for warehouses, multimerchandise shopping, food and beverage establishments, and other commercial structures construction. Residential construction is deflated not by a PPI but rather by the Census Bureau's price indexes for new single-family and multifamily houses under construction.

For some entries, price indexes are constructed from multiple series: For example, spending on residential improvements is deflated by an average of the Census's price index for single-family construction, the PPI for home maintenance and repair construction, and the BLS's Employment Cost Index for the construction industry. And in some cases, the BEA uses industry-published cost indexes such as the Engineering News Record construction cost index for communication construction and the Turner Construction Building-Cost Index for a number of other categories.

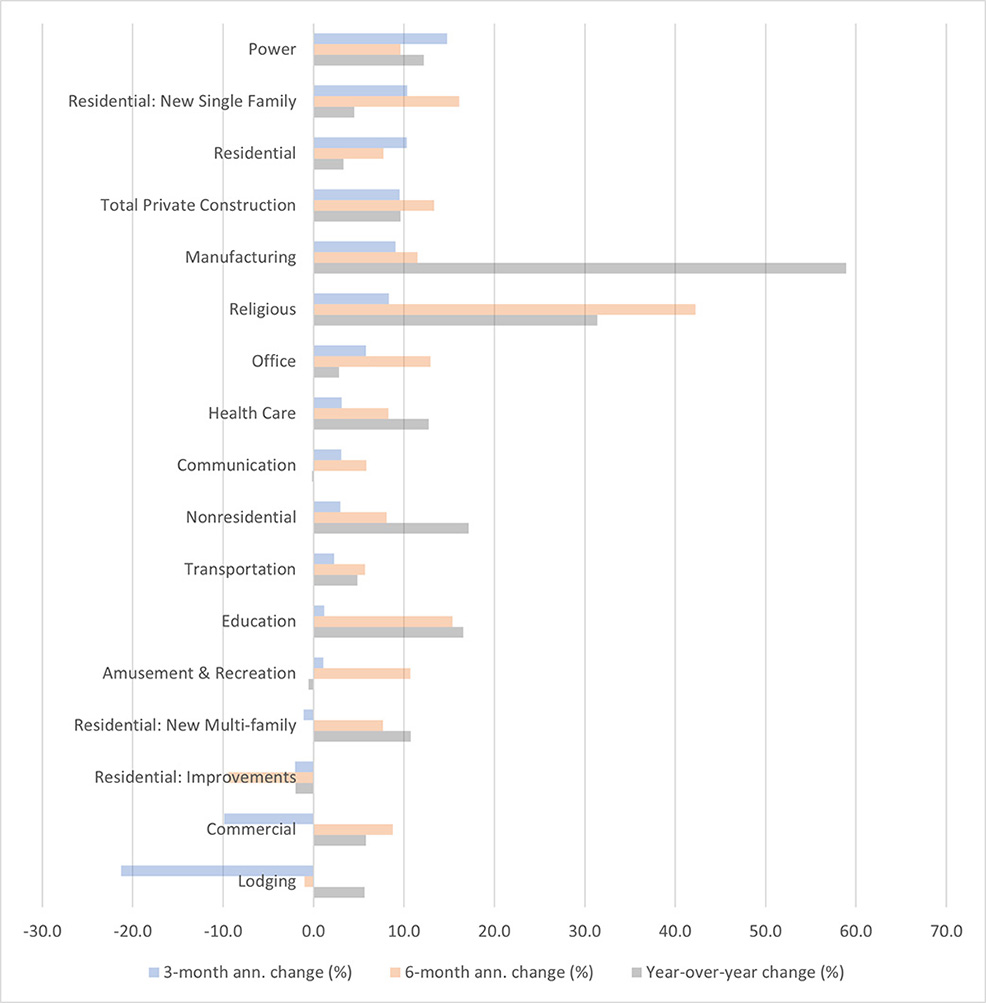

Figure 2 below shows three-month and six-month annualized changes in real private construction by category, deflating by PPI indexes for series that have a close match and by BEA investment price indexes in other cases.

Manufacturing construction has displayed tremendous growth over the past year, with real construction spending up 59 percent. It should be noted, though, that the pace of growth has slowed to 11.5 percent annualized over the past six months and 9.1 percent over the past three months. Annualized growth of new single-family construction spending has remained in double digit territory over the second half of 2023, compared to a year-over-year growth rate of 4.5 percent, suggesting a pickup in homebuilder sentiment as the year progressed. Despite worries about the impact of remote work on office demand, the pace of office construction has recently accelerated: Growth over the past three months has been faster than its 12-month pace.

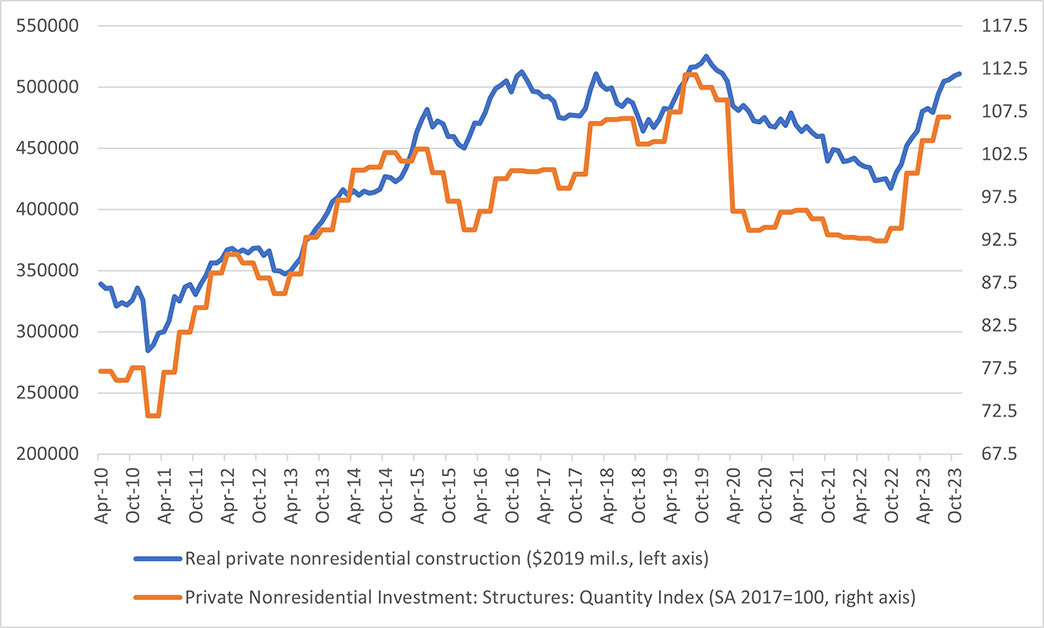

Figure 3 below shows how real private nonresidential construction spending from the monthly report has tracked closely with the nonresidential structures investment index from the quarterly GDP report, though the relationship isn't perfect because the nonresidential structures index includes data on "mining exploration, shafts and wells" obtained from energy industry sources.

Overall, the data point to a sustained and robust pace of real private construction spending toward the end of 2023. Figure 2 indicates that the most recent three-month annualized growth rate of 9.5 percent is close to its year-over-year growth rate of 9.6 percent, while Figure 3 shows that real spending has been on an increasing trend since October 2022. These data suggest that builders are going into 2024 on an optimistic note and could impart tailwinds to the rest of the economy as well.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us