Economic Impact of COVID-19

Special Report

May 12, 2020

The COVID-19 outbreak has greatly disrupted business activity throughout the economy. The vast majority of businesses in the United States are small, employing fewer than 50 people. In an effort to support small businesses and their employees, the Coronavirus Aid, Relief, and Economic Security (CARES) Act established the Paycheck Protection Program (PPP) to provide forgivable Small Business Administration (SBA) loans to qualifying small businesses. This report provides a descriptive overview of small businesses and reviews the programs, such as the PPP, implemented to aid them during the crisis.

Examining Small Businesses

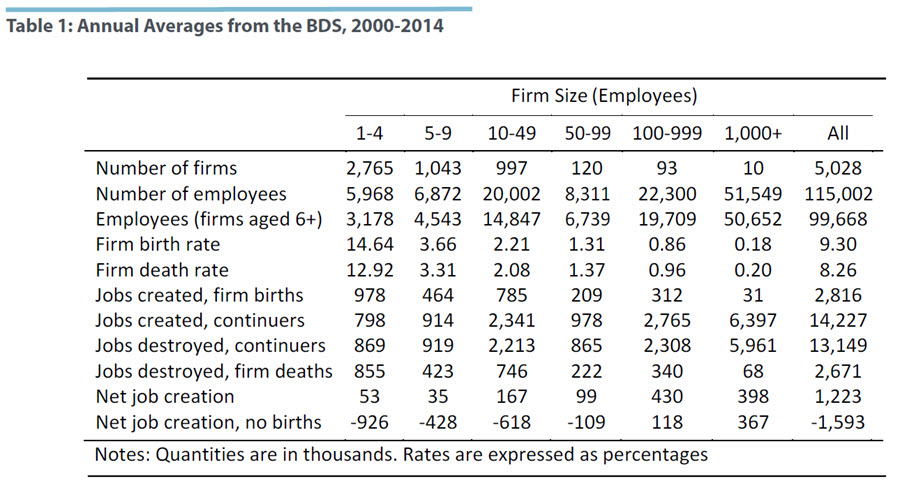

Table 1 presents descriptive statistics by firm size from the Business Dynamics Statistics (BDS), showing annual averages for the period 2000-2014. Although more than 95 percent of firms have fewer than 50 employees, this group employs less than 29 percent of workers. Small firms are characterized by rapid turnover. The birth and death rates for the smallest firms, 14.6 percent and 12.9 percent respectively, are orders of magnitude larger than those for the biggest.

Table 1 shows that most job creation and destruction occurs in ongoing firms. The one exception is the smallest firms — those with one to four employees — where the gross job flows generated by entry and exit are comparable to those generated by ongoing firms. On net, firms with fewer than 100 employees create very few jobs, and most of the jobs they create are due to entry. Once the effects of entry are removed, these firms have negative net job creation. This reflects the "up-or-out"dynamic emphasized by Haltiwanger, Jarmin, and Miranda (2013): A handful of small, young firms grow large, while the rest stagnate or exit.1 As the authors describe, small firms initially grow more quickly than large firms, but once the effects of age are removed, larger firms grow more quickly. They also document the effects of age itself (see also Decker et al., 2014). Conditional on surviving, young firms have the highest growth rates, by far. In short, older smaller firms show very little growth. Even so, such firms are common. Table 1 shows that even among firms with fewer than five employees, more than half of the employment is at firms six years or older.

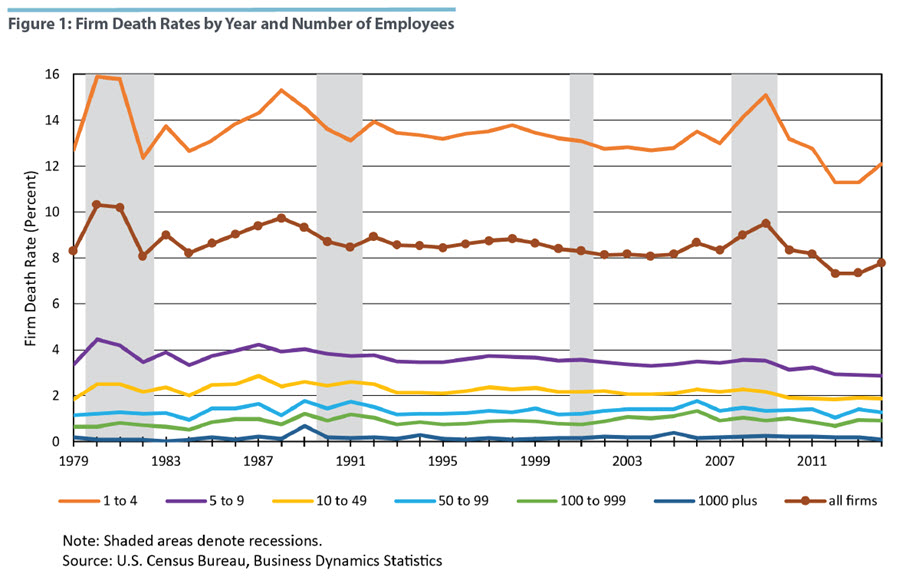

Figure 1 shows that firm death rates, especially for small firms, increased significantly during the recessions of 1980 and 1981-1982 and the Great Recession of 2007-2009. Young businesses are especially susceptible to downturns. In the Great Recession, the net job growth of younger firms fell much more than that of older firms, even when controlling for size.2

Small Business Profitability

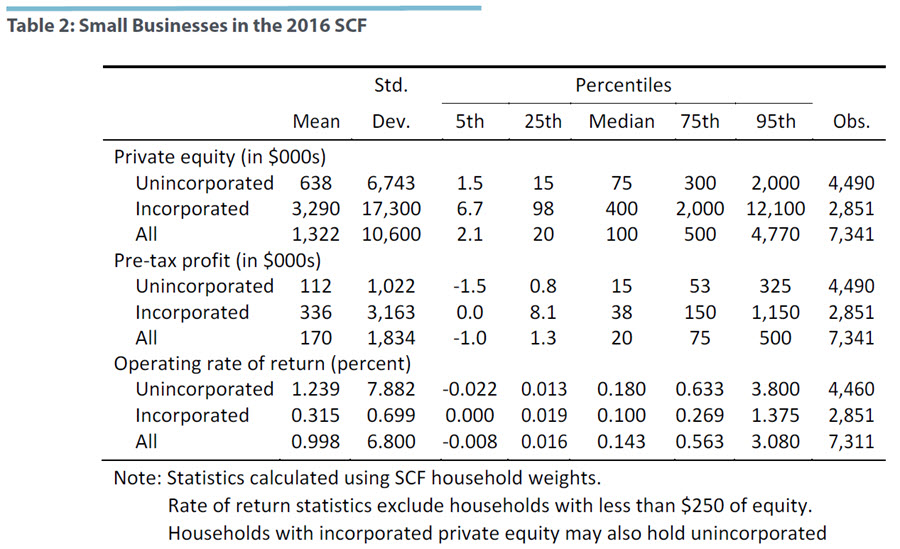

The BDS suggests that many small firms are unprofitable. A similar set of conclusions can be drawn from Table 2 which summarizes business equity and business income data from the 2016 Survey of Consumer Finances (SCF). The SCF includes single-person, self-employed businesses as well as those with employees. We distinguish between households who have at least part of their private equity in an incorporated firm and those whose equity resides wholly in unincorporated ventures. As expected, households invested in incorporated firms have much larger equity holdings, with a median value of $400,000, compared to $75,000 for the non-incorporated. They have much larger profits as well.

The SCF data for entrepreneurs varies greatly year to year. Nonetheless, within each type of household, as well as overall, the distributions of equity, profits, and returns exhibit the familiar thick right tail. Many of the unincorporated ventures operate at an extremely small scale. At the 25th percentiles of their respective distributions, these households have $15,000 of equity and receive $800 of profits. These may be secondary sources of income, but they are nonetheless quite small.

In assessing the income of small business owners, it is important to consider how well they might have done as employees. Several papers have sought to compare the income of entrepreneurs to their foregone earnings or capital income from alternative investments. Hamilton (2000) concludes that entrepreneurs earn considerably less than they would have as workers.3 Moskowitz and Vissing-Jørgensen (2002) find that returns on private equity are less than those available on public equities, while Kartashova (2014) argues that this is true only in particular periods.4

Neither paper addresses the riskiness of private equity. Hall and Woodward (2010) find that even though venture-backed entrepreneurs on average earn $5.8 million, once the return is adjusted for risk, entrepreneurs have an effective expected return close to zero.5

The low measured returns realized by so many small businesses have been taken as evidence that their owners are driven by nonpecuniary concerns, such as the satisfaction of being one's own boss. But even if most small businesses are unable or unwilling to expand, others have the potential to implement new technologies and/or create large numbers of new jobs. A number of recent studies emphasize the importance of high-growth young firms (the so-called "gazelles") and argue that the financial constraints these firms face can inhibit aggregate economic growth.6 For example, in their case study of the dairy industry, Jones and Pratap (2017) find that financial constraints have little effect on low-productivity farms, which appear more driven by nonpecuniary concerns, but restrict the growth of larger, more productive farms.7 Such findings suggest that, if possible, programs intended to assist small business should place considerable emphasis on the gazelles.

COVID-19 Credit Programs for Small Businesses

The PPP for forgivable SBA loans created by the CARES Act had an initial authorization of $359 billion. Under this program, a participating depository institution makes loans to qualifying small businesses (typically businesses with up to 500 employees). The loans have a maturity of two years and an interest rate of 1 percent. The amount of the loan is based on the borrower's average two-month payroll for the preceding year. The lending institution is protected from credit losses by an SBA guarantee. In addition, all or part of the loan will be forgiven if the funds are used for payroll costs, interest on mortgages, rent, and utilities; at least 75 percent of the forgiven amount must be for payroll. Forgiveness is conditioned on the borrower retaining or rehiring employees and maintaining compensation levels through June 2020.

To support this program and to mitigate balance sheet costs for lending banks, the Federal Reserve introduced the Paycheck Protection Program Liquidity Facility (PPPLF). This facility allows a lender to borrow from the Fed against its PPP loans on a nonrecourse basis. These discount window loans have the same maturity as the PPP loan collateral, and they have an interest rate of 35 basis points. The lending Federal Reserve Bank bears no risk, as the credit guarantee and forgiveness are provided by the U.S. Treasury, as authorized in the CARES Act.

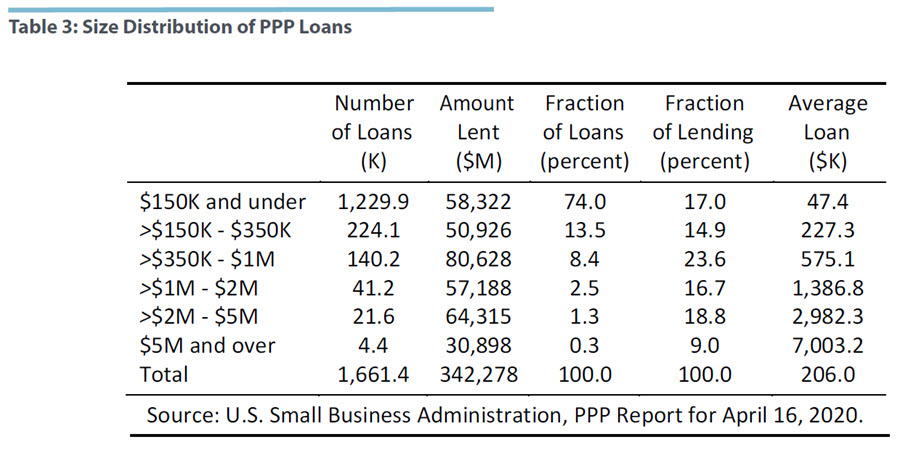

While the PPPLF became operational on April 16, lenders began processing applications for PPP loans on April 3. By April 13, the SBA reported more than 1 million loan approvals for a total of nearly $250 billion, and on April 16, the agency announced that it had reached its CARES Act limit. Table 3 shows the distribution of loans by size. Although nearly three-quarters of the loans were for $150,000 or less, more than 44 percent of the funds extended were for loans of $1 million or more.

In terms of industry, the sector with the greatest number of approved loans was professional, scientific, and technical services (208,360). The greatest dollar amount of approved loans went to construction ($50 billion). In addition to these two, other industries with more than 150,000 approved loans were health care and social assistance, accommodation and food services, and retail trade. Manufacturing had a somewhat smaller number of loans but was also among the largest recipients by dollar amount at $41 billion.

In addition to the PPPLF, the Fed announced its Main Street lending programs. With equity participation from the Treasury, the Fed will purchase 95 percent of an eligible loan made by a bank or other qualified lender to businesses with up to 10,000 employees or up to $2.5 billion in 2019 revenue. These loans have a longer maturity (four years) and an adjustable interest rate equal to the Secured Overnight Financing Rate plus 250-400 basis points. Interest and principle amortization are deferred for one year. Businesses that receive PPP loans may also receive Main Street loans. These programs appear more likely to reach better established, and perhaps larger firms in the small business universe, as the youngest and smallest firms typically do not have significant bank credit (other than through the SBA).

Assessing the Small Business Credit Programs

Given that firm turnover is high even during expansions and that many firms are relatively unproductive, what are the justifications for the PPP and the Main Street programs? If their primary goal is to assist workers who would otherwise be unemployed, why is unemployment insurance (UI) not sufficient? The most compelling answer is that modern economies are complex, interconnected systems that are vulnerable to collapse if too much of their "organizational capital" is destroyed.8 This variant of a network externality suggests that individual businesses will ignore the value of economic cohesion when deciding whether to maintain their supplier and employee relationships. Such concerns are amplified in times of great disruption. The counter to this argument is that preserving existing economic relationships impedes the creation of new, potentially superior ones. A line of thought dating back to Joseph Schumpeter contends that recessions "cleanse" the pool of businesses. Such arguments have additional salience in the current environment, where personal safety concerns may necessitate the wholesale transformation of certain industries.

A related question is whether losses due to social distancing represent a "legitimate" reason for businesses to close. If one expects the economy post-crisis to resemble its pre-crisis counterpart, one can make the case that businesses endangered by social distancing are economically viable operations hit by an extraordinary shock. If so, both efficiency and fairness argue that these businesses, along with their supplier and employee relationships, deserve protection. As with almost any government (or central bank) credit program, distinguishing those firms from those unlikely to be viable in the longer run can be difficult or impossible, especially in the midst of a widespread economic disruption. Even if a wholesale economic transformation is inevitable, there may be fairness arguments for ensuring that the costs of this transformation do not fall too heavily on any particular group. There are of course better ways to compensate small business owners than sustaining non-viable businesses, and every public insurance program runs the risk of moral hazard. It may still be too early, however, to make such a determination.

How does the distribution of approved PPP loans across industries align with these considerations? Some suggestive evidence can be found in a recent survey of small businesses by Bartik et al. (2020).9 Respondents were asked about their likelihood of remaining in business and maintaining their staffing through shutdowns of various lengths. Not surprisingly, the industries that appear most vulnerable to an extended crisis include food services and travel and tourism. While the food services sector is indeed one of the largest recipients of PPP loan approvals to date, travel and tourism is not, although this may simply reflect the size and industrial organization of the industry. Other industries near the top of the SBA's approved loan list, with exception of retail trade, do not appear as vulnerable in the survey. On the other hand, these sectors (e.g., professional, scientific, and professional services) may be the ones more likely to contain small firms with high growth potential.

Another argument for the lending programs is that in the absence of government intervention, financial frictions will limit the credit available to the smallest borrowers. From this perspective, it is not surprising that reports of PPP loans going to firms whose survival may not be threatened by the shutdown have received much attention. These firms include some restaurant companies whose designation as "small businesses" relies on their subsidiary structures. One of these, Shake Shack, announced that it was returning its PPP loan. There is a widespread belief that the program favors larger businesses with established bank relationships. To help address these concerns, the $310 billion extension of the PPP program signed by President Trump on April 24 sets aside $60 billion for smaller lenders. The SBA guidelines for the PPP now address the issue as well.10

The lending programs also seem likely to impose a significant administrative burden, as there are a number of required attestations regarding the uses of the funds, stemming from restrictions in the CARES Act. Citing this, the CEO of Keybank speculated in a recent Brookings Institution webinar, that the program would be primarily attractive to borrowers whose credit has become impaired.11 This might include businesses that have been relatively more disrupted by the pandemic response but could also include businesses whose problems have other sources. The administrative requirements for these programs will be most burdensome for the smallest firms, many of whom may instead use UI.

Even if we accept the need to keep most firms afloat, it is not obvious that the PPP, with its focus on employee retention, provides the best approach. While firms surely benefit from retaining experienced and skilled workers, they have other expenses, such as rent, utilities, insurance, and supplies. Although landlords and other upstream suppliers would ultimately benefit from forgiving some expenses to maintain their customer base, they too may face financial constraints.12 Programs aimed at helping firms meet their fixed costs, or helping their suppliers waive them, could thus prove valuable. The PPP supports firms along this dimension, but it may not be sufficient.

We conclude by noting that loans cannot offset sustained losses. The generous forgiveness provisions of the PPP demonstrate that policymakers already recognize this point. These concerns may well only intensify. Bartik et al. (2020) find that the median firm has less than one month's worth of cash on hand, and if the crisis lasts four months rather than one, the fraction of businesses that expect to be open in December falls from 72 percent to 47 percent. Should the disruptions from the pandemic prove sustained, the need to develop and implement transformative technologies will likely grow in importance as well.

John Bailey Jones is a senior economist and research advisor, Tim Sablik is an economics writer, and John Weinberg is a policy advisor in the Research Depart¬ment of the Federal Reserve Bank of Richmond. The authors thank Tom Barkin and Chen Yeh for detailed and extremely helpful comments. Rachel Rodgers and Luna Shen provided outstanding research assistance.

1

John Haltiwanger, Ron Jarmin, and Javier Miranda, "Who Creates Jobs? Small vs. Large vs. Young," Review of Economics and Statistics, 2013, vol. 95, no. 2, pp. 347-361.

2

Teresa C. Fort, John Haltiwanger, Ron S. Jarmin, and Javier Miranda, "How Firms Respond to Business Cycles: The Role of Firm Age and Firm Size," IMF Economic Review, August 2013, vol. 61, no. 3, pp. 520-559.

3

Barton H. Hamilton, "Does Entrepreneurship Pay? An Empirical Analysis of the Returns to Self-Employment," Journal of Political Economy, June 2000, vol. 108, no. 3, pp. 604-631.

4

Tobias J. Moskowitz and Annette Vissing-Jørgensen, "The Returns to Entrepreneurial Investment: A Private Equity Premium Puzzle?" American Economic Review, September 2002, vol. 92, no. 4, pp. 745-778; Katya Kartashova, "Private Equity Premium Puzzle Revisited," American Economic Review, October 2014, vol. 104, no. 10, pp. 3297-3334.

5

Robert E. Hall and Susan E. Woodward, "The Burden of the Nondiversifiable Risk of Entrepreneurship," American Economic Review, June 2010, vol. 100, no. 3, pp. 1163-1194.

6

Francisco J. Buera, Joseph P. Kaboski, and Yongseok Shin, "Entrepreneurship and Financial Frictions: A Macrodevelopment Perspective," Annual Review of Economic, August 2015, vol. 7, pp. 409-436; Ryan A. Decker, John Haltiwanger, Ron S. Jarmin, and Javier Miranda, "Where has all the skewness gone? The decline in high-growth (young) firms in the U.S.," European Economic Review, July 2016, vol. 86, pp. 4-23; John Haltiwanger, Ron S. Jarmin, Robert Kulick, and Javier Miranda, "High Growth Young Firms: Contributions to Job, Output, and Productivity Growth," In Eds. John Haltiwanger, Erik Hurst, Javier Miranda, and Antoinette Schoar, Measuring Entrepreneurial Businesses: Current Knowledge and Challenge, University of Chicago Press, 2017; Virgiliu Midrigan and Daniel Yi Xu, "Finance and Misallocation: Evidence from Plant-Level Data," American Economic Review, February 2014, vol. 104, no. 2, pp. 422-458; Andrea Caggese, "Financing Constraints, Radical versus Incremental Innovation, and Aggregate Productivity," American Economic Journal: Macroeconomics, April 2019, vol. 11, no. 2, pp. 275-309.

7

John Bailey Jones and Sangeeta Pratap, "An Estimated Structural Model of Entrepreneurial Behavior," Federal Reserve Bank of Richmond Working Paper No. 17-07, May 2017.

8

Olivier Blanchard and Michael Kremer, "Disorganization," Quarterly Journal of Economics, November 1997, vol. 112, no. 4, pp. 1091-1126.

9

Alexander W. Bartik, Marianne Bertrand, Zoë B. Cullen, Edward L. Glaeser, Michael Luca, and Christopher T. Stanton, "How Are Small Businesses Adjusting to COVID-19? Early Evidence from a Survey," Becker Friedman Institute for Economics at the University of Chicago Working Paper No. 2020-42, April 2020.

11

Brookings Institution, "Government Lending to Small Businesses during COVID-19-Why? How? And Will It Work?" April 14, 2020.

12

See Grey Gordon, John Bailey Jones, and Jessie Romero, "Loan Delinquency Projections for COVID-19," Federal Reserve Bank of Richmond Economic Brief no. 20-05, April 2020; and Jenny Schuetz, "Halting evictions during the coronavirus crisis isn’t as good as it sounds," Brookings Institution The Avenue blog, March 25, 2020.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.