Employment in the United States experienced the sharpest decline on record in April as the negative economic effects of the COVID-19 pandemic and social distancing measures caused employers to cut almost 21 million jobs, on net. (The next largest single-month decline was almost three-quarters of a century earlier, in September 1945, when almost 2 million jobs were lost.) Yet the full severity of the job loss was not known for quite a while: More than seven weeks passed from when the first state, California, issued a stay-at-home order on March 19 to when the Bureau of Labor Statistics (BLS) released the first national employment report fully reflecting the onset of the crisis, the report for April released on May 8.

Traditional sources of employment data are lagged, sometimes by a lot. At the national level, the employment report for a given month is typically released on the first Friday of the following month. And those data are based on a survey of firms that takes place around the middle of the month. This is why the jobs report for March had yet to show the full effect of the widespread social distancing measures, since many of those were put into place in late March and early April.

The BLS releases employment data for state and lower levels of geography at even greater lags. For example, the state-level data are typically lagged by another two weeks, coming out in the middle to the end of the month. County and metro employment and unemployment data are released a few weeks after that. And the most comprehensive source of data on local employment comes from the Quarterly Census of Employment and Wages, which is released between five and six months after the quarterly period ends. (For more on state and local labor market data, see "State Labor Markets: What Can Data Tell (or Not Tell) Us?" Econ Focus, First Quarter 2015.)

These lags are not new, or unknown, but in times of rapidly changing circumstances, the data are not sufficiently able to keep up with economic conditions. Knowing that the official employment counts would not be available for some time, economists, policymakers, and analysts looked during the COVID-19 crisis to other sources that could shed light on how the virus and the shutdown of economic activity were affecting the labor market. This includes the Federal Open Market Committee (FOMC), which, according to the minutes from meetings held in March, April, and June, found that traditional economic data could not capture the rapidly evolving situation; instead, the committee referenced high-frequency data.

Unemployment Insurance Claims

One source that directly shows changes in labor markets on an early basis, which the FOMC relied on in March, April, and June, is weekly unemployment insurance claims. Unemployment insurance programs are administered by individual states. Every state is required to report the number of initial and continued claims to the Department of Labor, which in turn releases that data to the public on the Thursday of the following week. As their names imply, initial claims are the number of new claims filed in the reference week, and continued claims are the number of workers who were already collecting unemployment benefits and remained unemployed in the reference week.

Because these data are timelier than payroll employment data from the BLS, they can serve as an early indicator of an economic downturn. In normal times, there is some variation in these data week to week as people move from employment to unemployment and back to employment or as some people decide to leave the labor force rather than continue to look for a new job. There are also seasonal patterns in the data, but those can be removed by applying a statistical procedure known as seasonal adjustment. Hindsight shows that in the weeks leading up to the starts of the last several recessions, the claims data tended to rise steadily and sometimes rapidly.

Take the Great Recession, for example. Data from the payroll survey began showing the decline in employment in February 2008, which was the first of 21 consecutive months of job losses. If we look at the six months prior to that, from August 2007 through January 2008, the payroll data were not alarming, with a slight increase in total employment in the United States (0.3 percent or 388,000 jobs). At the same time, though, initial claims (after being adjusted for seasonal trends) began to steadily increase, and seasonally adjusted continued claims rose 12.4 percent or by 314,000 jobs.

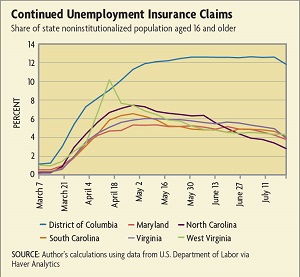

Likewise, evidence of an effect on employment from the COVID-19 pandemic appeared in the initial and continued claims data several weeks before the payroll data were available — but this time at rates never seen before. The first increase in initial claims in the United States came in the week ending March 14, when the number of claims rose 33.3 percent or by around 70,000. In the next week, initial claims rose more than tenfold from around 280,000 claims to almost 3.3 million and then more than doubled the week after to almost 6.9 million. The same data for Fifth District jurisdictions show similar trends except for West Virginia, where the initial claims data didn’t peak for another couple of weeks.

A similar story evolved with continued claims, which began to rise one week after the first spike in initial claims and continued to increase sharply week over week for the next several weeks. Claims rose nearly simultaneously across jurisdictions at the start of the pandemic, but there were variations in trends after that. Most notably, the number of people filing continued claims began leveling off and, in some cases, decreasing by the end of April or the start of May — except for the District of Columbia, where claims continued to rise and remained relatively flat in May and June. (See chart.)

In addition to providing the data to the Department of Labor, some state agencies release more detailed reports of the initial claims data on their own websites. Virginia is one of those states; its weekly reports include breakouts by gender, age, race, ethnicity, education level, and occupation. These breakouts offer a view into disparate impacts on different groups of people. The occupational data, for example, showed that in the week of April 4, the top two most affected occupations were food preparation and serving related occupations and personal care and service operations. In contrast, just prior to the start of the pandemic, the occupations with the largest numbers of claimants were administrative support and construction. This gave an early indication of which workers and industries might see the largest effects, which was confirmed in the payroll employment data several weeks later.

But what about tracking the recovery in real time? One of the limitations of these data is that we do not know the characteristics of those who stop filing a continued claim or the reason why they stopped. A drop-off in continued claims could indicate that people are going back to work, but it could also mean that people gave up looking for a job or exhausted their benefits. So a drop-off doesn't tell us much about the types of people who stopped filing versus those who remain on unemployment or the current demand for workers. Fortunately, there are some other high-frequency data sources that can give a glimpse into the staffing needs of employers.

Online Job Postings

One way to measure the current demand for workers is to look at the job advertisements that employers are posting online. To do that, one could simply peruse sites like LinkedIn or Indeed, but there are companies that offer aggregated data from across multiple websites. One such company is Chmura Economics & Analytics, a Richmond-based consulting service and data provider. Among the company's offerings is a database of online job postings called Real-Time Intelligence (RTI).

To create the RTI database, Chmura's computers scrape information from over 30,000 websites every day, including job sites like Indeed and individual company websites. When the data are processed each night, any duplicate postings that are identified are removed. One of the many pieces of information that Chmura gets from these websites is the date when the job opening was first posted, if available. If no such date is available, Chmura assigns one based on the first day on which their scraping process found the post. This date can be used as a filter and therefore allows a user to see how many job advertisements were posted online over a particular time frame.

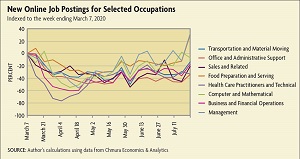

Among the eight occupation groups that accounted for the largest shares of new job postings in the first week of March, postings for food preparation and serving related occupations declined the furthest in late March and early April, followed by office and administrative support, sales and related jobs, and transportation and material moving occupations. (See chart.) This was an early indication that the effects on the labor market would be felt quite differently across different types of jobs, which was confirmed by the official payroll employment data — several weeks after the online job posting data was available.

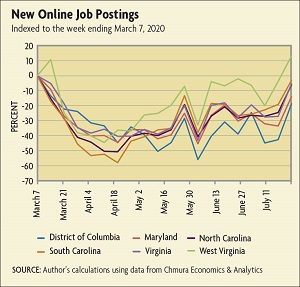

The same data shed light on the recovery in employment. Online postings for health care practitioners and technical workers and transportation and material moving occupations surged in the Fifth District in the week ending July 18. Postings for sales and related jobs also picked up in the first few weeks of July. This could be a sign that business conditions were improving at establishments that employ these workers, such as doctor's offices, shipping companies, and retail shops.

As with unemployment claims data, online job posting data do not tell the whole story. For one, given the number of jobs that were lost in March and April, if the number of new job postings matches the pre-pandemic level, that doesn't mean the labor market has returned to the same level of demand. And one might expect to see the number of new job postings exceed the pre-pandemic level for some time in order to fully recover the jobs that have been lost.

Additionally, while the data do show some trends in the types of jobs that are being advertised for, they do not show how many of those jobs were filled. And with part-time jobs, in particular, they do not show how many hours a week employers needed workers. There is another high-frequency data source, however, that sheds some light on the demand for hourly workers.

Homebase

Homebase is a company that provides free scheduling, time keeping, and communication products to local businesses with hourly employees. These are primarily restaurant, food and beverage, and retail businesses that are individually owned, which were some of the hardest-hit industries. In response to the pandemic, the company made some of its data free to the public so researchers and community members could track the number of hours worked by hourly and shift employees, the number of businesses that were currently closed, and the employees who were not working. All told, these daily data are based on more than 60,000 businesses employing 1 million hourly employees. Data start in January 2020 and are available to the public in more real time upon request.

Because the data are daily, and many businesses are not open seven days a week, the data exhibit some consistent patterns due to normal closures on certain days every week, like weekends. To correct for this, the data can be indexed to a prior period. Data used for this article have been indexed to the median value for the same day of the week for the period Jan. 4 to Jan. 31. This means, for example, that the hours worked on Wednesday, July 1 would be indexed to the median hours worked over the five Wednesdays in January. Looking at the data this way allows comparison over time relative to a particular period and across geographies.

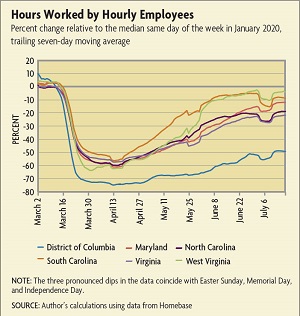

Across Fifth District jurisdictions, the trends in these data broadly coincide with where and when places began to reopen. For example, hours worked by hourly employees in West Virginia and South Carolina have bounced back quicker and are closer to their January levels than in other states — perhaps reflecting that West Virginia and South Carolina began their phased reopenings much sooner than other jurisdictions. The District of Columbia, which was the last in the Fifth District to reopen, remains the furthest from its pre-pandemic level. (See chart.)

Homebase data are also available broken out by industry. This means we can observe trends in the hours worked at just food and drink establishments or the number of businesses open in the personal care industry. In the Fifth District as a whole, these data show trends that one might expect, namely, a steep decline in employees working, hours worked, and locations open (all the way to zero, in some cases) starting in mid-March. The series then bottomed out and began to rise around mid-April when businesses began to resume operations on a limited basis, reflecting the phased approach to reopening that was occurring across much of the nation.

Hours worked leveled off or showed a slight declining trend toward the end of July. This may be a signal that the demand for hourly workers is slowing and may remain below prior levels for some time. Of course, hourly workers are only one segment of the labor force, but this pattern anticipated a similar one in July payroll data, which was released several weeks later and showed a slowdown in the pace of hiring.

Richmond Fed Surveys

In addition to the high-frequency data sources that have been discussed so far, the Richmond Fed has been using its own surveys of business conditions to gain further insights related to the pandemic. For example, in the March surveys of manufacturing and service sectors, which were fielded between Feb. 26 and March 18, respondents were asked additional questions about the impacts to their company so far due to COVID-19 and their expectations for the near term. Although the Richmond Fed publicly releases the results only after surveys have closed, staff often view responses as they come in on a daily or weekly basis.

In general, over the survey period, firms were reporting only minor negative effects on their operations, and most of the comments indicated those were due to supply chain disruptions from China and travel restrictions. By the third week of the survey, however, responses indicated that those negative impacts were escalating and outlooks for the U.S. economy were deteriorating.

The April survey, which ran from March 26 to April 22, was broadened further to include labor market specific questions. Specifically, that survey asked participants to indicate if they were reducing staff or the hours worked by staff. Results from those questions generally showed that the majority of responding firms were not reducing staff or the hours worked by employees; however, similar to the March survey, the results deteriorated as the survey continued. For example, in the first week of the survey, only about 15 percent of responding firms said they reduced staff, while in the final week of the survey, approximately 40 percent said they were cutting staff.

Then, in the May survey, the Richmond Fed collaborated with several chambers of commerce across the Fifth District to reach even more participants with a set of COVID-19 related questions. Overall, results from that survey showed how the labor market responses of firms varied by size and industry, with the most adverse effects being felt in the accommodation and food services, retail industries, and by small businesses. In contrast to earlier surveys, the results were generally consistent over the three weeks of the survey period.

The results of these surveys gave the Richmond Fed timely information about firms' experiences and the actions they took while the COVID-19 situation was unfolding. What's more, they gave evidence that the changing nature of the data over time means that one monthly indicator alone may hide some underlying dynamics or, at the very least, doesn't tell the whole story.

Emerging Sources

A few newer sources have become available. The first is the Real-Time Population Survey (RPS), which is a joint effort between academic economists and the Dallas Fed. The goal of the RPS is to provide a survey similar to the BLS' household survey of employment and unemployment (the Current Population Survey), but it differs in that the RPS is conducted online twice a month, and the results are made available with a shorter lag. The results of the RPS are plotted with the official BLS survey measures of employment and unemployment in reports available on the Dallas Fed's website.

The U.S. Census Bureau also began conducting two new high-frequency surveys to better understand the effects of COVID-19 on the economy. The first was the Household Pulse Survey, which was a weekly survey that began on April 23 and concluded on July 21. The results of the survey were posted one week after the survey period closed and gave insights into issues such as childhood education (including availability of computers and internet), employment, household spending and food sufficiency and insufficiency, health, and housing. The data, which are available at a national, state, and metropolitan level (for the 15 largest metro areas), are still available on the U.S. Census Bureau's website at the time of writing this article.

The second new survey from the U.S. Census Bureau is the Small Business Pulse Survey, which began on May 14 and is still ongoing. It is designed to provide information on small-business operations and finances, including any government support they have received and their outlook for the near future. These data are available at the national and state levels and for the 50 most populous metro areas. An interactive dashboard shows which industries and areas of the country have a relatively higher share of small businesses being negatively or positively affected by the pandemic and where firms are the most optimistic or pessimistic about the near future.

Conclusion

Although none are without limitations, each of these high-frequency data sources offers a glimpse into the labor market in nearer to real-time. The initial unemployment insurance claims data were particularly useful in understanding how many and, in some cases, the characteristics of workers who were being hurt during the crisis when many businesses were scaling back or shutting down operations.

The continued claims data were (and will continue to be) a useful indicator to track the number of people who are collecting unemployment each week. In terms of labor demand, online job posting data offer a glimpse into the types of jobs that employers are recruiting for, and the Homebase data show trends in the hours worked by hourly employees in some of the hardest-hit industries. Lastly, the Richmond Fed has used and will continue to use the ability to add special, topical questions to its surveys of business conditions to understand the effects of the pandemic.

The Richmond Fed has created Pandemic Pulse, an area on its website that features interactive charts of various high-frequency indicators.