Who's in Need?

Measuring low- and moderate-income status and poverty status in the Fifth District

Econ Focus

First Quarter 2023

Both governments and community-based organizations administer means-tested programs that serve populations in financial need. Some programs, such as the Supplemental Nutrition Assistance Program (SNAP) or Housing Choice Vouchers, provide immediate access to necessary resources. Others, such as Pell Grants, provide resources so beneficiaries can access opportunities that will improve their long-term earning potential.

How do policymakers decide who qualifies for means-tested programs? Depending on the goals and available resources of the program, policymakers may decide to limit eligibility to low-income or both low- and moderate-income (LMI) individuals and families. For place-based initiatives, in which resources support a project that serves a community as opposed to an individual, policymakers may limit eligibility to areas where aggregate income statistics indicate that the population living in the area is predominately low income or LMI.

Policymakers and researchers studying LMI populations need a benchmark to assess individuals' or households' incomes. The two most commonly used are the poverty threshold and area median income (AMI). This article discusses differences between them and how they are used to describe income dynamics in the context of the Fifth District.

Who is Considered LMI?

Characterizing income relative to the poverty threshold or AMI are two different ways to tell a similar story. There are practical differences between the two measures. Most notably, the poverty threshold is nationally determined and used to identify extremely low-income populations, whereas AMI is locally or regionally determined and is more often used to understand or characterize conditions facing LMI populations. Technically, the poverty threshold serves as the basis for absolute measures of poverty, meaning a measure that compares people's income against a foundational needs standard that remains consistent over time. AMI is used to create relative measures of income, which consider how well-off people are compared to a standard of living that is allowed to shift over time and in relation to their peers.

Sidebar

For research purposes, the question of whether to use income relative to AMI or income relative to the poverty threshold to evaluate a population depends on the question being asked.

The poverty threshold was created in 1963 and was based on three times the cost of a minimum food budget. This is because, at the time, most families' food budgets were their largest recurring expense, accounting for about one-third of their total budget. Because the cost of a family's food budget depends on the number of family members, different poverty thresholds were defined based on family size. Every year, the Census Bureau calculates current poverty thresholds by adjusting the 1963 poverty threshold for inflation. The Census Bureau's 2022 poverty thresholds range from $14,036 for a household of one person over age 65 to $64,815 for a family that consists of nine or more related adults.

People living in families earning less than the poverty threshold are considered to be in poverty, meaning they are extremely low income. Researchers and policymakers also consider depth of poverty measures, which instead compare family incomes to a fraction or multiple of the poverty threshold. For example, some researchers consider families earning up to 200 percent of the poverty threshold to be low income. In this way, depth of poverty measures more fully describe the economic well-being of families.

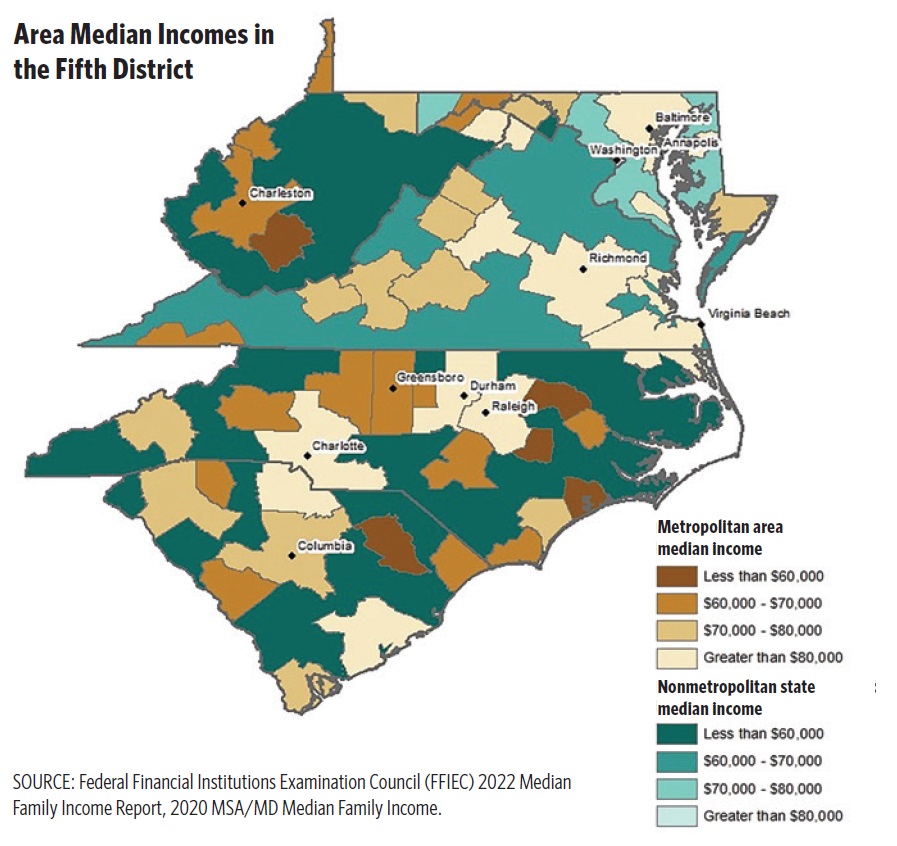

AMI measures the median income at the metropolitan statistical area (MSA) level for metropolitan areas and state-level nonmetropolitan median income for nonmetropolitan areas. Because income tends to be higher in metropolitan areas, AMI tends to be greater in those areas than in nonmetropolitan areas. As a case in point, none of the nonmetropolitan state median incomes in the Fifth District exceed $80,000, whereas many MSA median incomes do. (See map below.)

Most organizations use a definition of LMI that includes families earning up to 80 percent of AMI, but definitions of who is considered extremely low income, very low income, or low income vary. One commonly used scale is:

- Extremely low income: at or below 30 percent of AMI

- Low income: 31-50 percent of AMI

- Moderate income: 51-80 percent of AMI

- Middle income: 81-120 percent of AMI

What Places Are Considered LMI?

Income characteristics can also be described for geographic areas, such as counties or census tracts.

A geographic area can be characterized by the area's poverty rate, which indicates the share of people living below the poverty threshold. A geographic area is considered high poverty if its poverty rate is over 20 percent.

Alternatively, a geography may be considered LMI depending on how aggregate income characteristics compare to AMI. In most cases, a geographic area is considered LMI if its median income is less than 80 percent of AMI. For example, in 2020, the city of Baltimore's median income was $52,164, which is about 50 percent of the Baltimore-Columbia-Towson MSA AMI of $104,637; therefore, Baltimore is considered low income. Nonmetropolitan counties are considered LMI if their median income is less than 80 percent of the nonmetropolitan state AMI. For example, in 2020, McDowell County in southern West Virginia had a median income of $26,072, which is 44 percent of West Virginia's nonmetropolitan state median income of $59,300, so it is considered low income.

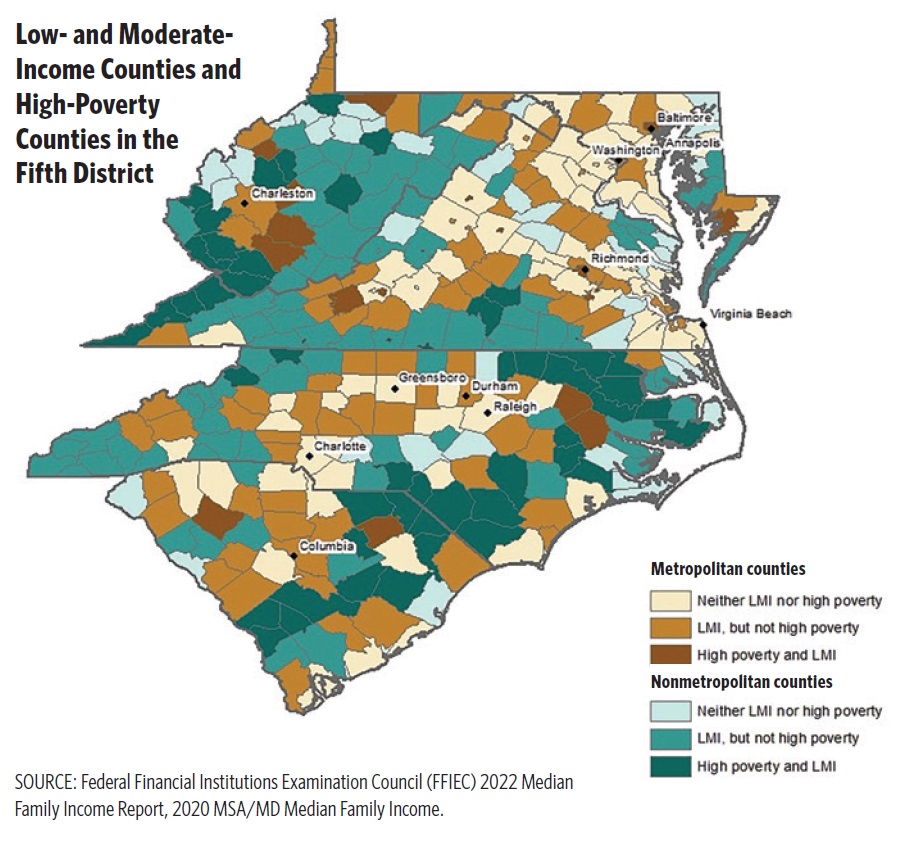

In the Fifth District, nonmetropolitan counties are more likely to be both high poverty and LMI than urban counties. Significant shares of both metropolitan and nonmetropolitan counties are LMI but not high poverty. (See map below.)

Measuring the Eligibility of Individuals

To determine whether families or individuals are eligible for public assistance, state and federal agencies frequently compare their incomes to the poverty threshold. For example, families are eligible for SNAP (which provides food subsidies) or Head Start (which provides free early care and education) if their incomes are at or below 130 percent of the poverty threshold.

Eligibility criteria can be complicated. For example, some state-administered programs (including SNAP) can override federal eligibility criteria. To clarify how location-specific criteria influence the amount of benefit a family is eligible to receive, the Atlanta Fed has developed the Policy Rules Database. This resource takes into account the number of adults and children in the family, age of adults, and disability status. Users then select which public assistance programs they want to consider, and the database displays how public assistance benefits will vary as their employment income changes.

Federal programs that use AMI to assess individual and family eligibility tend to provide benefits related to expenses for which prices fluctuate across localities. For example, programs administered by the U.S. Department of Housing and Urban Development (HUD), such as Housing Choice Vouchers, use AMI to determine eligibility. This allows the value of housing benefits to adjust to the cost of housing across communities.

To simplify the process of determining whether a family is income-eligible for public assistance programs, some states use broad-based categorical eligibility, which expands eligibility from one program to another. For example, qualifying for the Temporary Assistance for Needy Families program would confer categorical eligibility on a family, making them eligible to receive SNAP public assistance as well.

Some government programs are also designed with flexible eligibility thresholds. For example, North Carolina has a child care subsidy program that is funded with both state and federal resources. Families are income-eligible if they earn up to 200 percent of the poverty threshold, but the program is also available to families that meet certain situational criteria (for example, if a parent is in school or a job training program). Mecklenburg County, N.C., augments these resources to expand eligibility to households earning up to 300 percent of the poverty threshold, and to reduce the work/education-hour requirements for families earning less than 200 percent of the poverty threshold.

Measuring the Eligibility of Places

Some grants or loans are awarded to organizations that will use those resources to improve the economic conditions of a specific place. In order to be awarded or get credit for place-based program funding, organizations are required to describe aggregate income characteristics of the community they intend to serve.

The Community Reinvestment Act (CRA) was established to make sure banks were equitably providing access to credit throughout their service area. In particular, the CRA requires banking regulators such as the Fed to encourage banks to meet the credit needs of the communities they serve, including LMI communities. The CRA defines LMI communities based on aggregate income characteristics of a place. Banks meet CRA requirements by providing or purchasing loans and for providing grants and services in LMI communities. A community may consist of a subcounty geography, such as a block group or tract. According to the CRA, a geography is low income if it has a median family income of at most 50 percent of AMI, and moderate income if it has a median family income of 50 percent to 80 percent of AMI.

Our Related Research

"The Shortcomings of a Work-Biased Welfare System," Economic Brief No. 21-15, May 2021.

"Revisiting the Community Reinvestment Act," Econ Focus, First Quarter 2022.

"Connecting a Region Apart," Econ Focus, Second Quarter 2022.

"Rural Spotlight: Creating Family Economic Security in Western Maryland," Regional Matters, September 2021.

Other programs, such as the New Markets Tax Credit (NMTC), allow the applicant — generally an investor — to decide whether to use poverty rates or AMI to determine whether the target community is considered low income. NMTC provides federal income tax credits to investors that contribute to qualified investments in low-income communities. With a few exceptions, a community is considered low income if it is located in a census tract with a poverty rate of at least 20 percent, or where the median family income does not exceed 80 percent of AMI.

Some place-based programs take a different approach to assessing eligibility: They specify that LMI populations are intended to be served using resources provided, regardless of aggregate income measures. For example, Community Development Block Grant (CDBG) funds are allocated to states, cities, and counties on a formula basis and are used to expand housing and economic opportunities for LMI people. Instead of relying on comparing the community median income to AMI, applicants need to consider how many people in the community they plan to assist fall in this income range. These data are not available in standard Census Bureau American Community Survey (ACS) tables, which most organizations rely on for timely data. HUD, the agency that administers CDBG, works with the Census Bureau to provide data on the number of LMI people at the county level every five years.

Using aggregate income measures to determine place-based eligibility may present challenges for places with small populations, such as rural areas. Because five-year ACS data are based on a sample of about 5 percent of households, places with small populations may observe greater variance in median income estimates from year to year than places with larger populations. This could influence the community's eligibility from one year to the next, making it difficult for community leaders to anticipate what resources they can rely on over time.

Some place-based funding tends to be awarded on the basis of a combination of factors, including the local unemployment rate, income, and poverty characteristics. For example, the Community Development Financial Institutions Fund's Bank Enterprise Award Program is awarded to depository institutions that have increased their investments in census tracts with poverty rates above 30 percent and unemployment rates that are at least 50 percent greater than the national unemployment rate. As another example, the Appalachian Regional Commission determines match requirements based on an economic distress index, which takes into account a county's unemployment rate, per capita income level, and poverty rate.

LMI Measures in the Fifth District

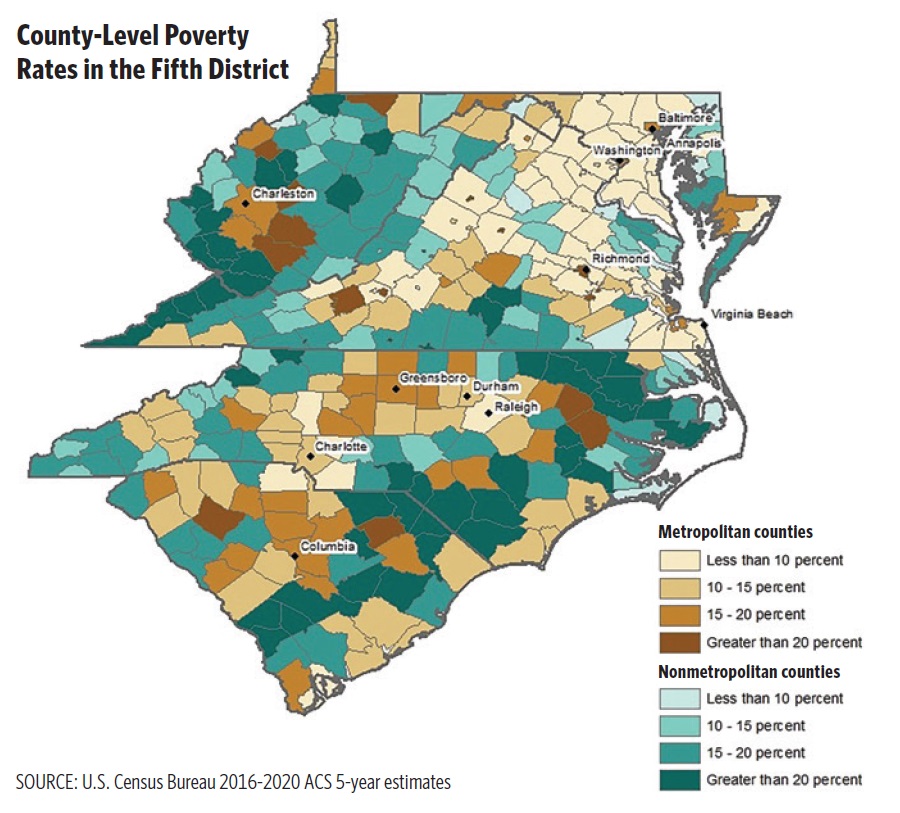

Looking at Fifth District communities' poverty rates and median income relative to AMI presents two different ways to understand income characteristics of the local population. At the county level, there are clusters of high poverty counties in eastern North Carolina and South Carolina, in western Virginia, and in southern West Virginia. High poverty metropolitan counties tend to be scattered throughout the Fifth District. (See map below.)

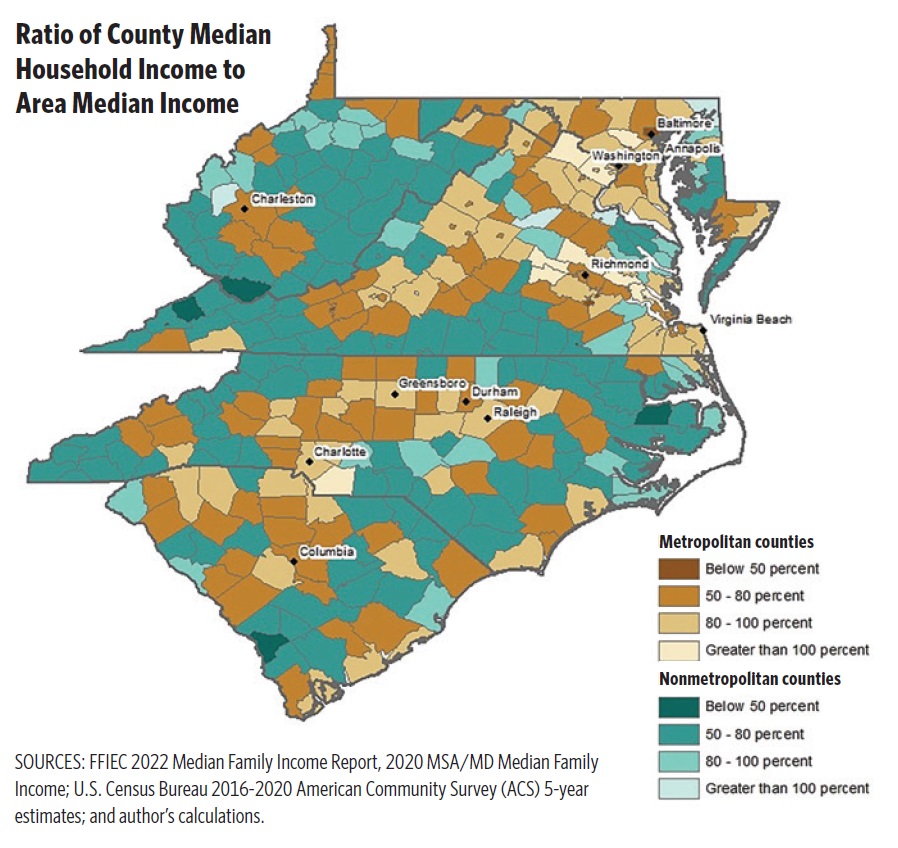

Most nonmetropolitan counties in the Fifth District are LMI, and more than half of metropolitan counties are LMI. Few counties in the Fifth District have median incomes greater than 100 percent of AMI. (See map below.) Note that, while this analysis displays county-level statistics, the same analysis can be conducted at smaller geographies.

Looking at these two maps together tells a more complete story about specific places. Some places are unambiguous. For example, McDowell County in southern West Virginia is both high poverty and low income. Other stories are more complicated. For example, Richmond is high poverty, but moderate income. This means that, while about 21 percent of Richmond residents live below the poverty threshold, there are enough people with relatively high incomes to somewhat offset those with extremely low incomes.

Neighborhood-level poverty and income characteristics in Richmond reveal how this might be the case. Neighborhoods in the eastern part of the city tend to be both high poverty and low income, whereas neighborhoods in the western part of the city tend to have incomes greater than 100 percent of AMI and lower poverty rates. Most neighborhoods with high poverty rates are also low income; the one exception is the Woodland Heights neighborhood, which is in the central part of the city and is both high poverty and has a median greater than 100 percent of AMI.

Conclusion

AMI and the poverty threshold are two benchmarks against which to measure the economic well-being of a family or individual. They can also be used in aggregate to assess the extent of economic need in a community. When studying community income dynamics, the poverty rate and median income-to-AMI ratio can be used in conjunction to tell a more complete story, and hint at income distribution. In addition, the Supplemental Poverty Measure provides another lens through which to assess the economic well-being of populations.

Subscribe to Econ Focus

Receive an email notification when Econ Focus is posted online.

By submitting this form you agree to the Bank's Terms & Conditions and Privacy Notice.

Contact Us