The Potential Impact of Public Service Student Loan Forgiveness in the Fifth District

Economic Brief

August 2022, No. 22-29

The Public Service Loan Forgiveness program offers government and nonprofit workers relief from outstanding federal loans after 10 years of employment. In October 2021, the Department of Education temporarily waived certain requirements, making many public service workers retroactively eligible for loan relief. This waiver expires on Oct. 31, 2022, creating a risk that many eligible beneficiaries will not access benefits. The program may be especially important in the Fifth District, which has a higher share of public service workers than the U.S. as a whole.

Student loans are the second largest source of consumer debt in the U.S., with more than 43 million individuals holding over a total of $1.6 trillion in student debt. In the Fifth Federal Reserve District, there are about 4.3 million borrowers with balances totaling more than $169 billion.1

For student loan borrowers working for governments and nonprofit organizations, the Department of Education's Public Service Loan Forgiveness (PSLF) program offers relief from outstanding federal loans after 10 years of employment. This program may be especially important in the Fifth District, where the proportion of workers employed in these sectors is greater than in the U.S. overall.

To date, the number of borrowers who have received PSLF benefits lags far behind the number who are likely eligible for immediate forgiveness. To address challenges that limited access to the PSLF program in prior years, the Department of Education issued a series of changes rendering many public service workers retroactively eligible for loan relief. Because some of these changes are set to expire on Oct. 31, 2022, there is a risk that many eligible beneficiaries will not access benefits.

In this Economic Brief, we begin by quantifying public service employment in the Fifth District and the nation. We then describe the PSLF program and the recent waiver that allows for retroactive consideration of eligibility. Next, we turn to an overview of borrowers who are likely eligible for relief under the PSLF waiver. Finally, we discuss barriers to takeup, as the extent and distribution of loan relief ultimately depends on whether workers succeed in navigating the application process.

Public Service in the Fifth District and the Nation

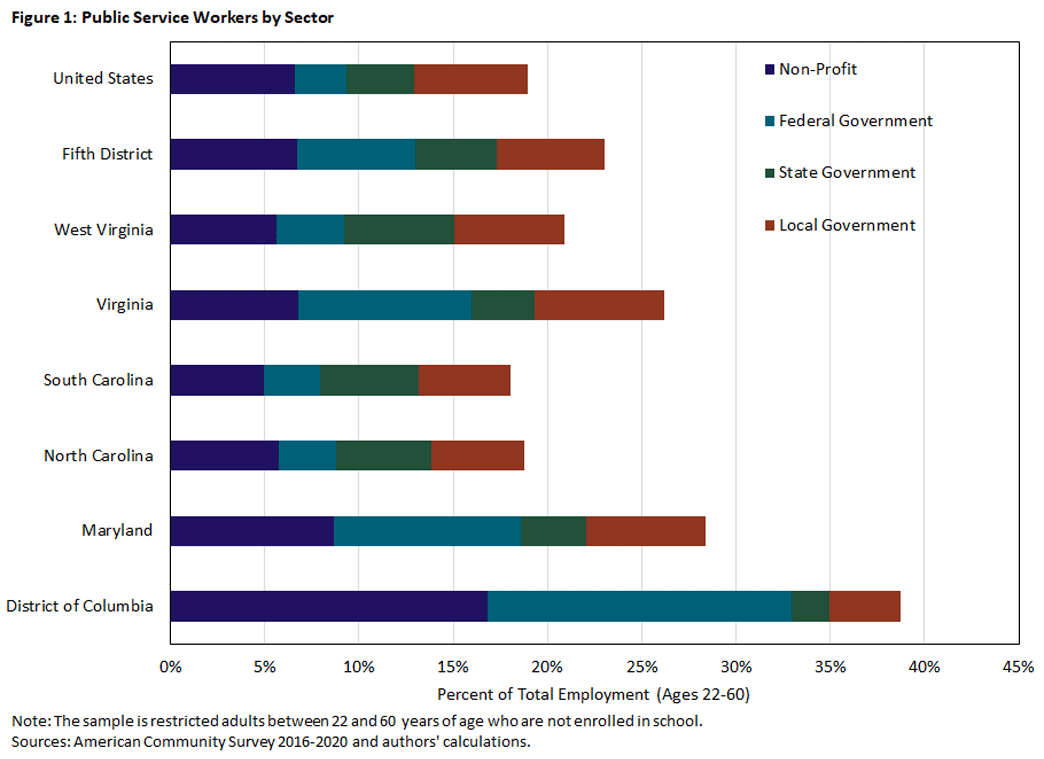

The Department of Education defines public service employees as those employed by local, state or federal government or by an organization with 501(c)(3) nonprofit status. This describes about 19 percent of U.S. adults and 23 percent of Fifth District adults. (All estimates in this article refer to adults between the ages of 22 and 60 who are not enrolled in school.)2 Figure 1 displays public service workers by sector and location.

Due to the high concentration of federal government employment in Washington, D.C., and its surrounding areas in Maryland and Virginia, 6.3 percent of all Fifth District workers are with the federal government, compared to 2.7 percent of workers nationwide. In terms of shares of public service workers, 27.4 percent of the Fifth District's public sector employees are in the federal government, compared to about 14.3 percent nationwide. Outside of the federal government, some of the main public service occupations include teaching, protective services, social work and health care.

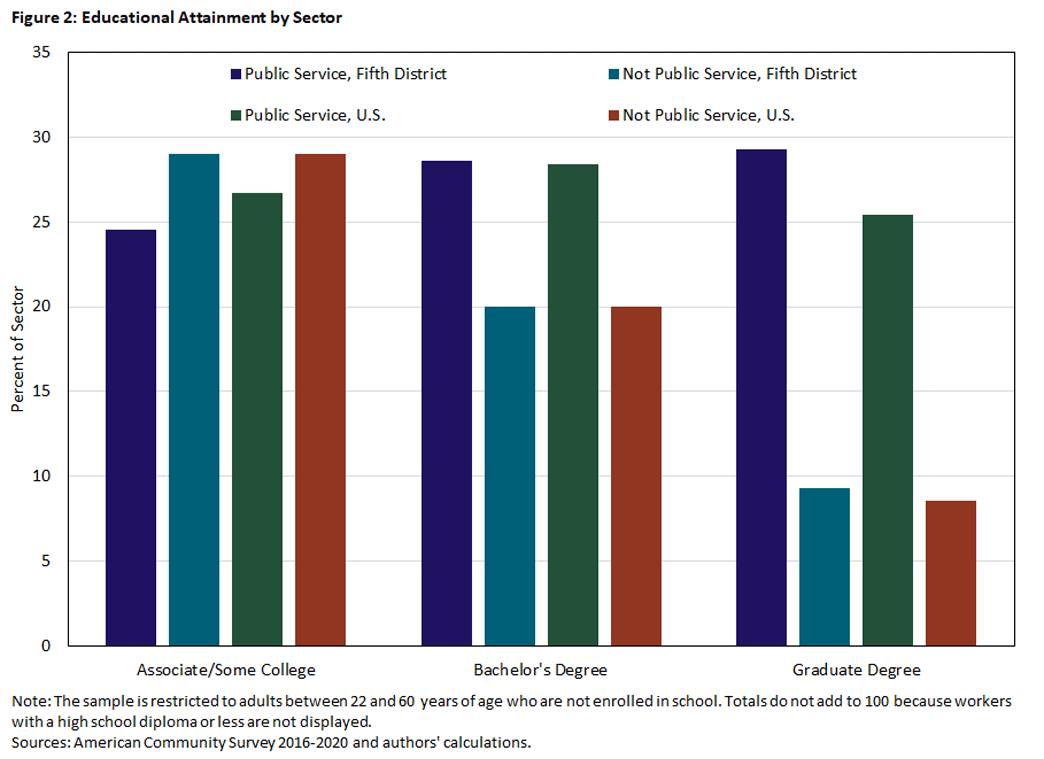

Many public sector occupations — such as teaching and social work — require at least a bachelor's degree and often some graduate-level course work. Both nationally and in the Fifth District, public service workers are more likely to have bachelor's and graduate degrees than workers in other sectors. This is especially true in the Fifth District, where 29.3 percent of public service workers hold graduate degrees compared to 25.4 percent nationwide, as seen in Figure 2.

More years of education are associated with higher levels of student debt. According to the 2022 working paper "Waivers for the Public Service Loan Forgiveness Program: Who Would Benefit From Takeup?":

- About 15 percent of adults who attended college but did not receive a bachelor's degree hold student debt, with the median amount owed about $12,000.

- Among those with a bachelor's degree, about 23 percent hold student debt, with the median borrower owing about $20,000.

- Among adults with a graduate degree, about 28 percent hold student debt, with the median borrower owing about $40,000.

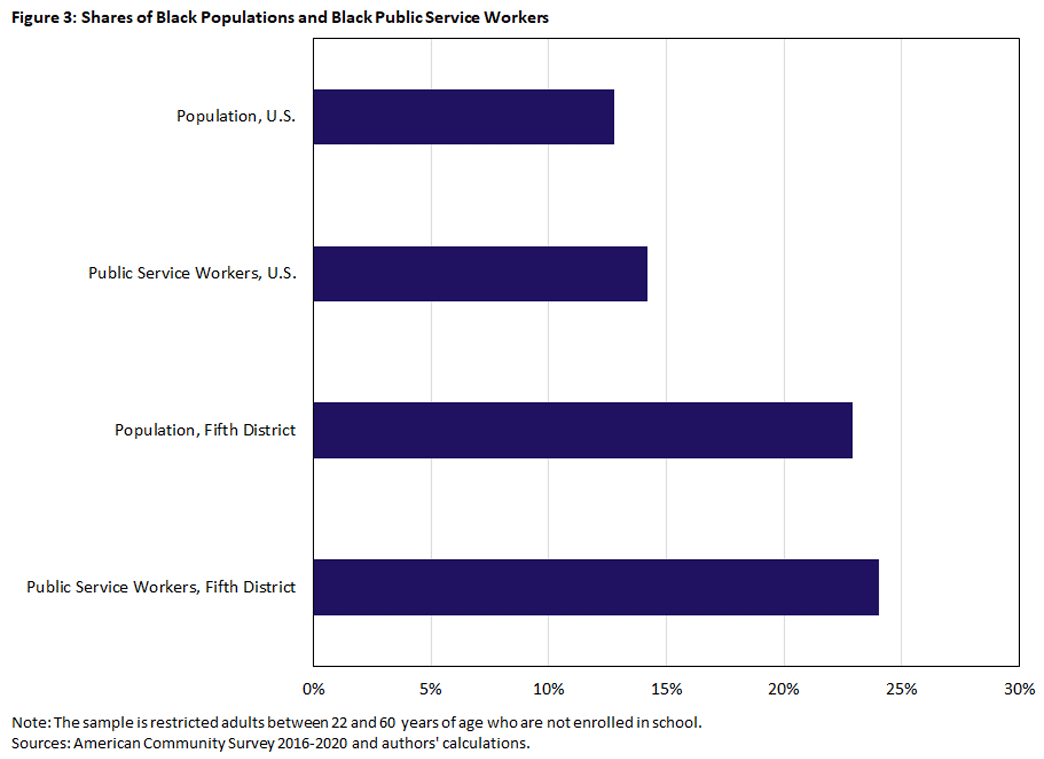

Public service workers also tend to be a bit more racially diverse than the working-age population as a whole. Black workers make up 14.2 percent of U.S. public service workers aged 22-60, compared to 12.8 percent of the total population of the same age. The proportion is even higher in the Fifth District, where Black workers comprise 24.0 percent of public service workers and 22.9 percent of the population. The larger proportion of Black public service workers likely reflects both the fact that the Fifth District has a higher share of Black residents than the U.S. as a whole, and the slightly higher overall representation of Black workers in public service sectors, as seen in Figure 3.

Student debt among those with at least some college experience also varies by race. Black college attendees and graduates are more likely to hold student debt overall (28.6 percent relative to 19.8 percent for White attendees and graduates). This holds true within the public sector, where 33.8 percent of Black workers have student loans, compared to 25.5 percent of White workers. Among public service workers, the mean (median) student debt held by Black workers is $43,687 ($26,000) versus $39,535 ($23,000) for White workers.

Overall, the public service workforce is a large and diverse population that also carries significant student loan debt. How could the PSLF program help this population in the nation and the Fifth district?

The Public Service Loan Forgiveness Program

On the surface, the PSLF program appears very straightforward: It offers full forgiveness of federal student loans for workers with 10 years of full-time public service employment and 120 qualifying monthly payments. But in practice, determining and demonstrating eligibility have proven to be quite complicated.

The first year that borrowers were expected to receive PSLF relief was 2017, 10 years after the program was introduced in 2007. At the time, about 40 million people were employed in public service in the U.S. Around 30,000 people applied for forgiveness that year — and only 96 received it. By the end of 2018, just 338 people had seen their loans forgiven. Even by the end of September 2021 (prior to the eligibility changes that will be discussed in more detail below), only about 16,000 people had received forgiveness.3

Why did relatively few borrowers complete applications for forgiveness, and why did such a small share receive it? Both complicated administrative processes and poor communication about the requirements likely limited access to the program and contributed to high denial rates.

For example, borrowers needed to have a form signed by an authorized official certifying their employment at a public or nonprofit organization, and for some borrowers this form can only be submitted via standard mail or fax.4 In addition, only borrowers with federal Direct Loans using a standard or income-based repayment plan qualified for PSLF. And even if a borrower consolidated non-qualifying loans into a Direct Loan, the payments made prior to consolidation didn't count toward the required 120. Some student loan servicers also have been criticized for allegedly failing to inform borrowers that they were eligible for PSLF or steering them into forbearance programs instead.

The PSLF Waiver

In October 2021, in response to the continued effects of COVID-19 pandemic, the Department of Education announced a year-long waiver of certain program requirements to increase access to PSLF.5 In particular, nearly all student loan borrowers who were employed full time in public service occupations and were not in default became retroactively eligible to have prior payments on any repayment plan count as qualifying payments, even if the payments were made late or were not for the full amount due. Certain periods of forbearance and deferment will also be counted under the waiver. In addition, workers with federally guaranteed loans (Federal Family Education Loan) could have prior payments count retroactively so long as they consolidate to Direct Loans.

This means that workers who have accrued 10 years of full-time public service employment are eligible for immediate full forgiveness, while those with a shorter employment history may receive additional qualifying payments, shortening the time to forgiveness. The waiver is set to expire Oct. 31, 2022.

While the waiver expands eligibility, many administrative hurdles remain, and the process can be complicated and time consuming. This may be especially true when individuals have worked for multiple employers, since they are required to submit multiple forms certifying their employment. And individuals who have different types of loans face additional challenges, as the waiver still requires them to consolidate older Federal Family Education Loan loans or Perkins loans to Direct loans to receive benefits.6

Potential Beneficiaries of the Waiver

How many borrowers and how much debt are affected by the PSLF waiver? One of the authors of this brief (Turner) and co-authors Diego Briones and Nathaniel Ruby estimate as many as 3.5 million borrowers owing a total of $145 billion of student loan debt are potentially eligible for immediate PSLF relief.

Who are these potential beneficiaries? The distribution of workers in the public sector who have at least 10 years of full-time experience provides a starting point:

Occupations

The largest single occupational group is the teaching profession, representing about 23 percent of potential PSLF recipients. Nurses and related health-assisting occupations are about 10 percent of potential PSLF forgiveness recipients. Other occupations that are well-represented among potential immediate PSLF beneficiaries are social workers (6.1 percent), those in the protective services such as firefighters and police officers (4 percent), and physicians (1.9 percent).

Education

Graduate education dominates among those with potential immediate PSLF eligibility, reflecting in part the concentration of occupations like teaching, social work and nursing in public service. Over 45 percent of the immediate PSLF population holds a graduate degree, and these graduate borrowers hold more than 63 percent of the debt likely eligible for immediate PSLF relief. This reflects the fact that individuals with graduate degrees have almost twice as much student debt as individuals with bachelor's degrees.

Income

Nationally, those workers eligible for PSLF relief are likely to be concentrated above the median of the overall income distribution. Nearly 54 percent (approximately $80 billion) of potential immediate PSLF relief would go to workers in these deciles. Naturally, those employed full time in public service professions are underrepresented at the very bottom and very top of the income distribution.

Race

The distribution of potential PSLF relief by race reflects the relative concentration of Black Americans in the public sector and their greater reliance on educational borrowing to finance post-secondary education. While Black and White borrowers are similarly likely to be potentially eligible for PSLF forgiveness, Black borrowers can expect somewhat higher levels of forgiveness: Average relief for Black borrowers would be around $47,900, while average relief for White borrowers would be about $38,800. Considered in the context of debt per capita, the Black-White gap in student loan debt would be predicted to drop from $1,575 to about $868 if all eligible recipients took up benefits.

While it is not possible to observe employment histories and loan balances at the state level, the employment and demographic distribution of states in the Fifth District suggest magnified opportunities for PSLF relief:

- There are simply more public sector workers per capita in the Fifth District than in the nation.

- The higher education levels in the Fifth District among public service workers also suggest higher debt burdens and thus greater potential relief from the PSLF program.

- There is a higher proportion of Black workers in public service in the Fifth District, who are more likely to have loans and to have larger debts than White workers with the same level of education.

The Distributional Effects of Limited PSLF Takeup

As of the end of June 2022, nearly 165,000 borrowers with a total of $10.5 billion in debt had qualified for loan forgiveness, including through the waiver. While this represents a significant increase over previous years of the program, it still pales in comparison to the 3.5 million public service workers who are potentially eligible for immediate relief.

In the Fifth District, the number of borrowers receiving relief has also been modest, ranging from fewer than 1,000 people in West Virginia to 5,830 in Virginia, as seen in Table 1.

Table 1: PSLF Forgiveness in the Fifth District

| Borrowers With PSLF Discharges (as of June 2022) | ||

| State | Borrower Count | Outstanding Balance (in Millions) |

| D.C. | 1,180 | $98.0 |

| Maryland | 4,700 | $320.5 |

| North Carolina | 4,170 | $270.2 |

| South Carolina | 2,940 | $206.8 |

| Virginia | 5,830 | $372.0 |

| West Virginia | 1,060 | $53.8 |

| Total | 19,880 | $1,321.3 |

| Note: Borrower counts are rounded to the nearest 10. Totals may not equal the sum of the values due to rounding. | ||

| Source: U.S. Department of Education | ||

While neither race nor occupation among those who have received PSLF benefits is known, one may make some inferences based on the levels of relief received. For the nation as a whole and the Fifth District, benefits levels have been relatively high:

- The national average is nearly $65,000.

- The Fifth District average is more than $67,000.

- In Washington, D.C., the average is more than $85,000.

Those who have been among the first to succeed in takeup with the PSLF program have been among those with substantial graduate school debt. According to testimony from Richard Cordray of the Federal Student Aid Office, 83 percent of those who received PSLF relief by October had graduate-level debt, while more than 30 percent had current income above $100,000.

This raises the concern that takeup behavior may widen rather than narrow socioeconomic disparities in debt burdens. Doctors and lawyers — who tend to have the highest debt levels and the highest incomes — may be among the most likely to have access to professional services to reduce the burden of navigating the application process.7

Improved outreach to public service workers — including better communication from the Department of Education and loan servicers — is one way to help workers access benefits under PSLF. Still, such efforts may need to go beyond simple nudges or basic notifications given the complexity of the application process. Prior experiments have convincingly demonstrated that outreach efforts that provide administrative support to assist with completing forms and submitting of materials can increase takeup.8

In this brief, we do not attempt to identify how and by whom such support might be provided. But recognizing the potential benefits of PSLF and encouraging action before the Oct. 31 deadline may yield student debt relief for millions of public service workers in the Fifth District and across the U.S.

Elizabeth Link is a research assistant and Sarah Turner is the Souder Family Professor of Economics and Education at the University of Virginia. Jessie Romero is an assistant vice president in the Research department at the Federal Reserve Bank of Richmond.

1

The Fifth District is comprised of Maryland, North Carolina, South Carolina, Virginia, most of West Virginia and Washington, D.C. For detailed student loan data, see the New York Fed's quarterly reports on Household Debt and Credit and the Department of Education's Federal Student Loan Portfolio.

2

Estimates in this paper were generated using data from the American Community Survey (ACS) and weighted using frequency weights downloaded with the ACS data. The data include information from 2016 to 2020 and only considers observations in which a respondent was between 22 and 60 years of age and not enrolled in school. With these restrictions, there are 6,970,606 observations within the sample. There are 690,763 observations in the Fifth District.

3

See the Department of Education's Public Service Loan Forgiveness Data for more information.

4

Only borrowers whose loans are already serviced by MOHELA can submit their forms online.

5

Prior to this waiver, Congress also created Temporary Expanded Public Service Loan Forgiveness, which provided limited, additional conditions under which borrowers could be eligible for forgiveness.

6

See the aforementioned 2022 working paper "Waivers for the Public Service Loan Forgiveness Program: Who Would Benefit From Takeup?" and the 2022 working paper "Public Service Loan Forgiveness Waivers: A Time-Limited Opportunity for Debt Relief" for an extended discussion of the policy changes.

7

This potential "selection" into takeup among those with relatively high income is consistent with recent social science evidence which suggests that "bandwidth tax" of administrative process is most onerous for those from the least advantaged groups. See the 2013 book "Scarcity: Why Having Too Little Means So Much," the 2018 book "Administrative Burden: Policymaking by Other Means," the 2021 paper "Increasing Enrollment in Income-Driven Student Loan Repayment Plans: Evidence From the Navient Field Experiment," the 2019 paper "Takeup and Targeting: Experimental Evidence From SNAP" and the 2022 podcast "The Scourge of the 'Time Tax.'"

8

See the 2012 paper "The Role of Application Assistance and Information in College Decisions: Results From the H&R Block FAFSA Experiment" and the 2019 paper "Takeup and Targeting: Experimental Evidence From SNAP."

To cite this Economic Brief, please use the following format: Link, Elizabeth; Romero, Jessie; and Turner, Sarah. (August 2022) "The Potential Impact of Public Service Student Loan Forgiveness in the Fifth District." Federal Reserve Bank of Richmond Economic Brief, No. 22-29.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us