Revisiting Forecasts for Rent Inflation

Macro Minute

May 24, 2022

Last summer, Xiaoqing Zhou and Jim Dolmas at the Dallas Fed warned that rising home prices threatened to push up rent prices, adding pressure to overall inflation. How well have these early warnings held up? In this blog post, we look at how actual rents have fared since last summer and dive into what the most recent numbers imply for rent inflation going forward.

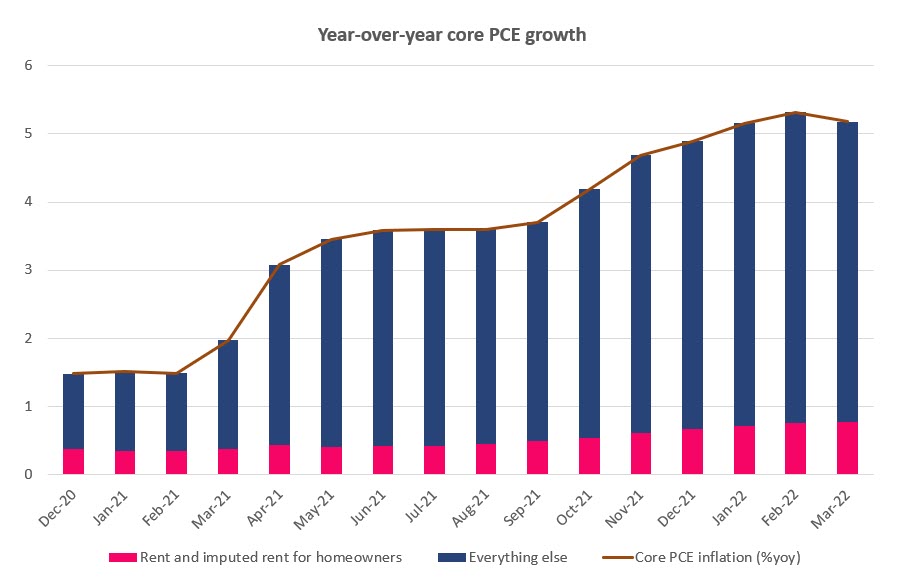

Figure 1 below shows that, indeed, the contribution of rent and imputed rent for homeowners to year-over-year core inflation has increased over recent months. (See the blog post "Gimme Shelter Inflation" for a discussion of the differences between rent and imputed rent.) The contribution has risen from 38 basis points in December 2020 to 77 basis points in March 2022.

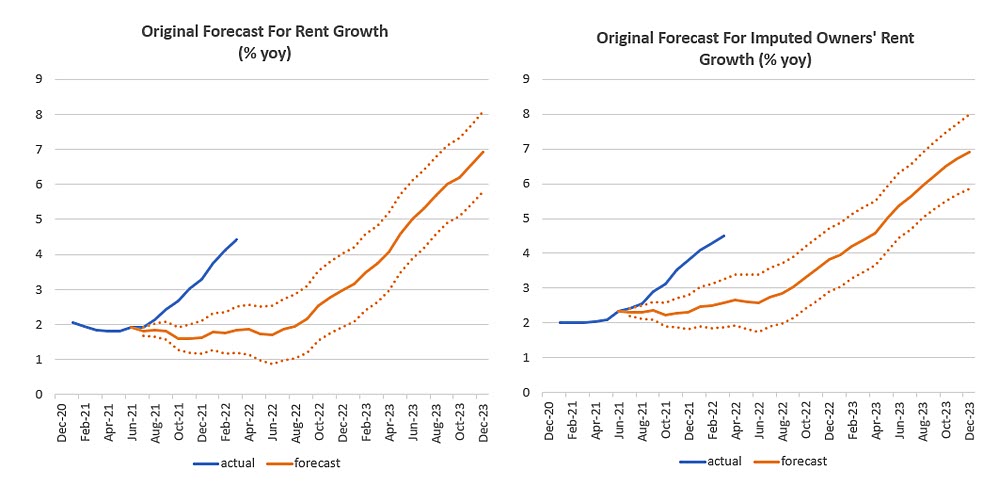

Figure 2 shows how rent and imputed rent exceeded the predictions of the Dallas Fed forecast from last summer.

Growth in the PCE rent index exceeded 4 percent year over year in March, a threshold that the model predicted would not be crossed until the second quarter of 2023. Similarly, imputed rent for homeowners rose 4.4 percent in March, which the model predicted would have been attained in the first quarter of 2023. Year-over-year growth in both rent and imputed rent was over 1.5 percentage points higher than the upper confidence interval of the forecast in March.

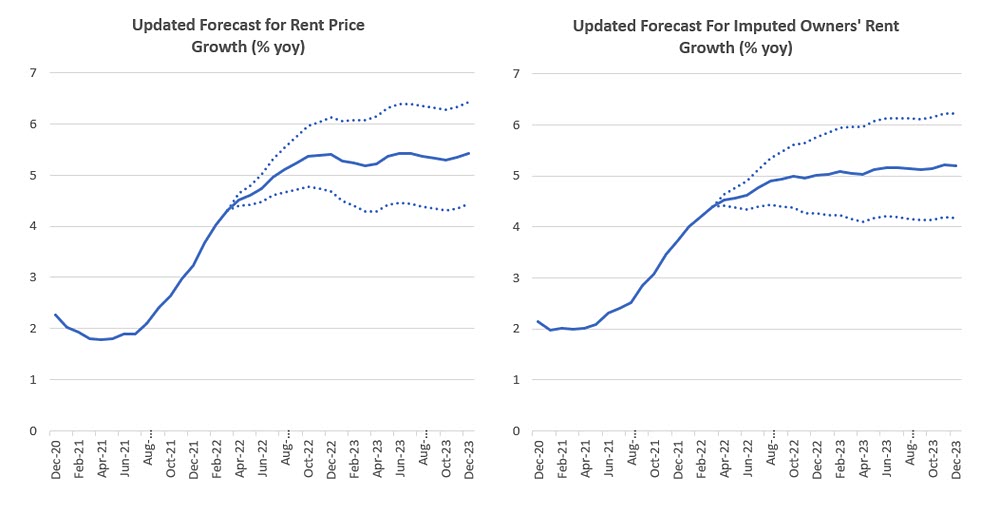

Despite the large forecast miss, it might still be interesting to see what the model is predicting today, after incorporating the most recent readings for inflation and home prices. In Figure 3 below, we rerun the Dallas Fed model incorporating the latest data.

The updated results suggest that, given current growth rates of rents and house price indexes, we should expect year-over-year growth rates for both rent and imputed rent to remain elevated — around 5 percent year over year — for an extended period. However, in contrast to the original forecast, both series are no longer expected to reach 7 percent growth by the end of 2023.

Like the original forecast, the evolution of rent and imputed rent may turn out to be different from the model's predictions. Optimists would note that this model doesn't account for the Fed's current policy normalization path, and it could be that rising interest rates cause shelter prices to come down relative to what the model predicts. But the model's forecast for further elevated price growth — along with its recent history of underpredicting rents — highlight that inflation risks stemming from rents may very well be tilted to the upside as well.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us