Income, Spending and Inflation

Macro Minute

August 16, 2022

What does normalization from a period of high inflation look like? Does getting back to the Fed's inflation target start with households cutting back on spending? Or does the labor market tend to slow before high inflation is whipped? Depending on the answers, we might see the economic data unfold in different ways. In the first case, we might see nominal personal spending drop ahead of a decline in inflation readings. In the second case, nominal personal income might fall before inflation falls.

In this week's post, we look at how nominal income and spending behave in the months surrounding inflation peaks. We use core PCE inflation, which exclude highly volatile food and energy prices, in order to focus on the inflationary episodes that are the most persistent.

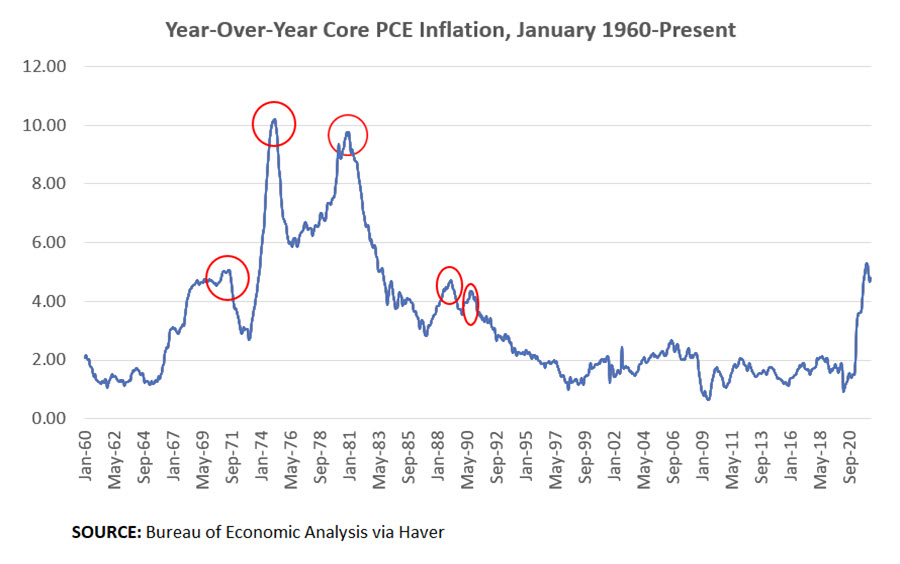

First, we identify five high-inflation peaks in history, based on visual examination of the data since 1960. These peaks are highlighted in Figure 1 below.

- July 1971 (7.8 percent)

- February 1975 (11.2 percent)

- November 1980 (10.2 percent)

- February 1989 (8.3 percent)

- September 1990 (6.9 percent)

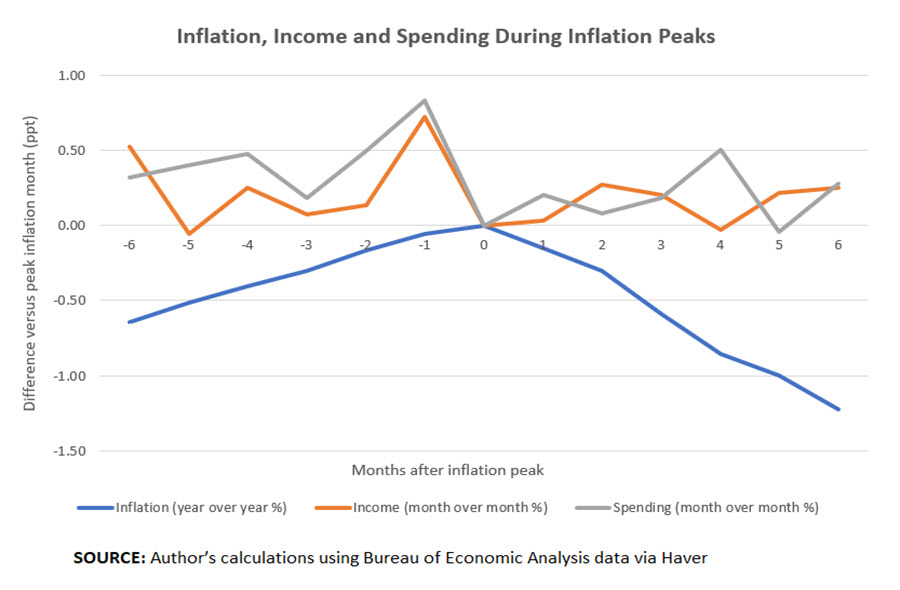

Next, we look at monthly growth rates of nominal personal income and personal consumption expenditure in the intervals surrounding inflation peaks. We normalize the monthly growth rates by subtracting the growth rate observed in the month that inflation peaked from the surrounding observations. (This also makes the value in period 0 — or the month where inflation peaked — equal to zero.) Our results are shown in Figure 2 below, which plots the average across the five episodes.

The blue line in Figure 2 shows the difference between year-over-year core PCE inflation and its level in the month that inflation peaked, averaged across the five episodes of peaking inflation we identified earlier. The horizontal axis indicates months before and after the inflation peak. As expected, inflation readings in the six months preceding and following the peak were lower than during the peak.

The orange line in Figure 2 shows the difference between the month-over-month growth rate of nominal personal income and its growth rate during peak inflation, averaged across the five episodes of peaking inflation. The gray line shows the analogue for nominal personal consumption expenditure.

We tend to see an acceleration of monthly nominal income and spending growth in the months preceding an inflation peak. Monthly growth rates of both variables appear to be at their most elevated just before inflation peaks, with a sequential rise from three months before peak through the month immediately preceding the inflation peak. In these previous episodes, the acceleration of nominal income and spending have happened roughly simultaneously.

These results suggest we may not necessarily see slowing in monthly personal income and spending prior to hitting peak inflation. In fact, we may even see an acceleration in both series. Will this historical pattern play out in the current high-inflation episode?

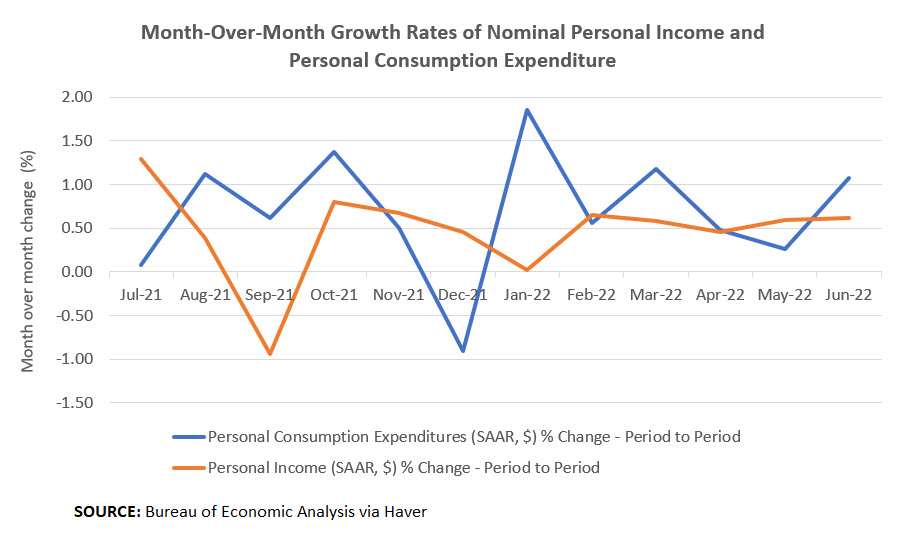

With only five episodes of history to draw from, it's difficult to make firm inferences about what will happen this time around. As of this writing, month-over-month growth rates of personal income have risen each month from April to June, and nominal personal spending saw a large 1.1 percent monthly increase in June, as seen in Figure 3 below.

That acceleration might tempt one to believe that peak inflation could be imminent. But to date, the highest reading for year-over-year core PCE inflation came in February, when core inflation hit 5.3 percent and was preceded by three months of decelerating growth in nominal personal income.

As noted by many economic observers, a key feature of today's economy is how different it looks from the past. As a result, maybe the only thing we can expect as inflation returns to normal is for the unexpected to occur.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us