Rough Road Ahead for Auto Sales

Macro Minute

May 16, 2023

Does the auto industry still have further room to run? While auto sales have been trending up over the past several months, we'll look into a couple of reasons why the future may not be so bright.

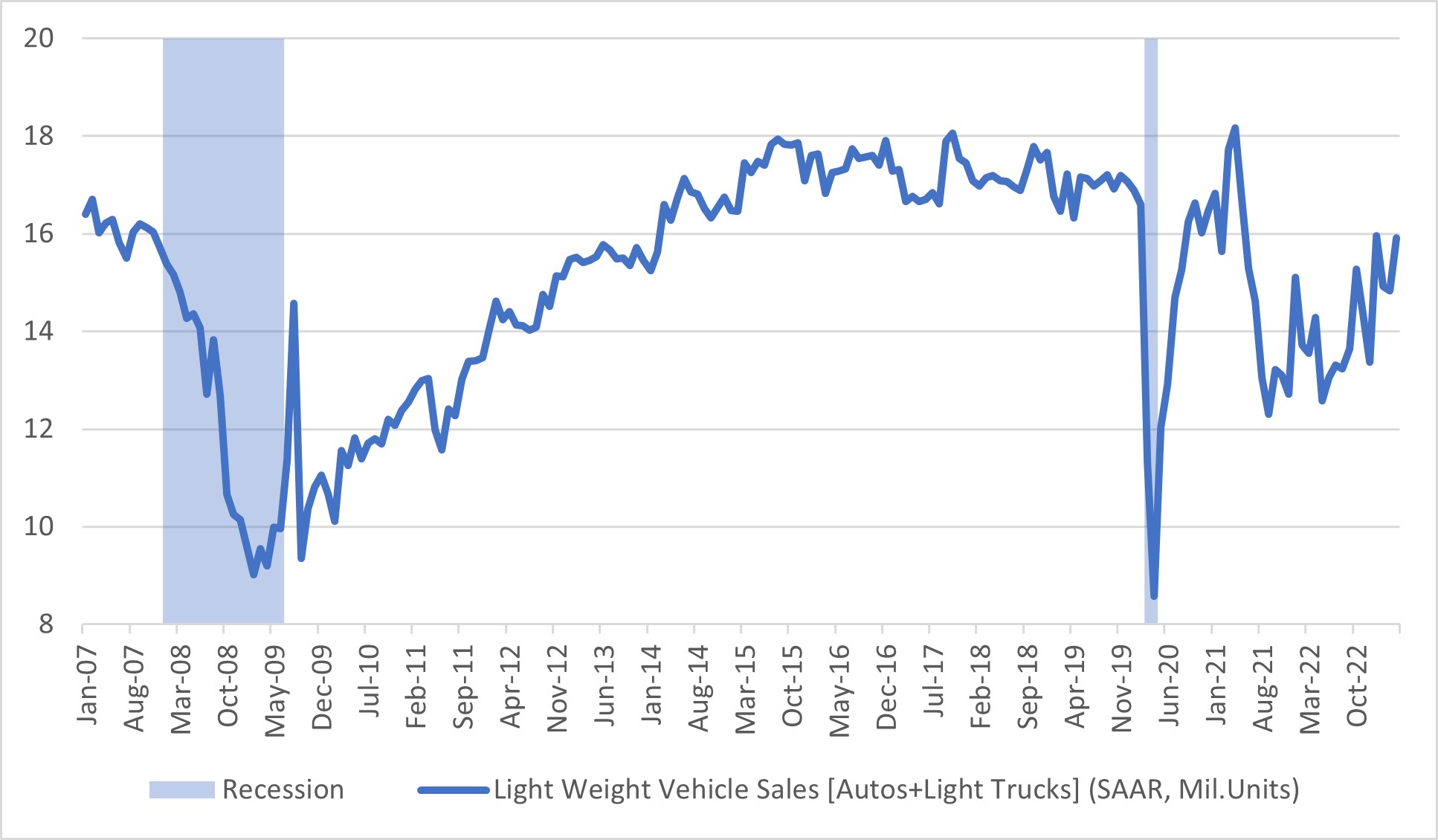

Despite rising interest rates dampening demand in this traditionally interest rate-sensitive sector, the seasonally adjusted annualized rate (SAAR) of light vehicle (that is, auto, light truck and SUV) sales rose to 15.9 million in April from a pace of 14.8 million units in March, as seen in Figure 1 below.

Furthermore, there seems to still be room to grow. The industry has yet to fully recover to pre-pandemic levels, as the overall pace of auto sales remains lower than the SAAR of 17.0 million units seen in the five years before the pandemic.

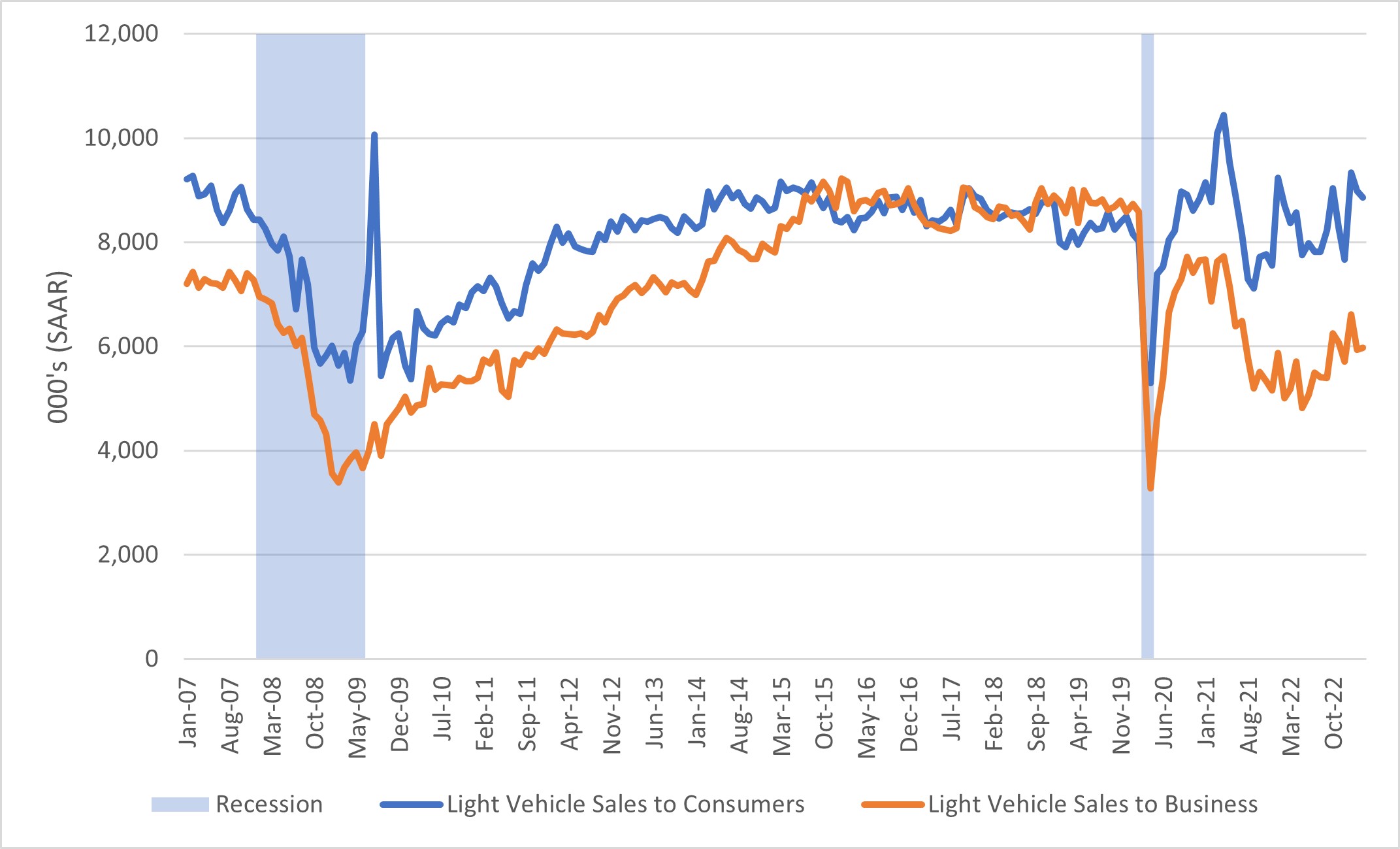

Breaking down light vehicle sales by sector reveals additional insights about the nature of the recovery. As shown in Figure 2 below, light vehicle sales to consumers have more than fully recovered from the pandemic shock. In March 2023, consumer light vehicle sales rose to an 8.9 million SAAR compared to an 8.0 million SAAR in February 2020, an 11 percent increase. In contrast, sales to business customers (which includes fleet sales to rental car companies) remain depressed versus pre-pandemic levels. In March, light vehicle sales to businesses came in at a 6.0 million SAAR compared to an 8.6 million SAAR in February 2020, a 30 percent decline.

Auto industry analysts often consider vehicle sales to be mean reverting. With an approximately 1:1 ratio of vehicles to driving-age population, annual sales in the United States are driven by cycles of vehicle aging and replacement rather than a rising trend in vehicle ownership. Periods of lower-than-normal vehicle sales tend to be followed by periods of higher-than-normal vehicle sales, as pent-up demand among consumers leads to temporary sales surge during a recovery.

The opposite is also true, with periods of higher-than-normal sales followed by periods of depressed sales performance. Thus, the industry suffers payback effects following a boom: After many customers satisfy their demand for new cars, dealers must wait for new-car demand to build up once again.

Is there still room for pent-up consumer demand to push industry sales back up to the 17.0 million pace? Considering the full post-COVID-19 period, light vehicle sales to consumers appear to be running at a normal pace. The average consumer light vehicle SAAR from March 2020 through March 2023 was 8.3 million units, essentially in line with its pre-pandemic average pace. With higher interest rates pushing up the cost of financing and with consumer sentiment low — as indicated by the University of Michigan's April 2023 consumer survey, which said 67 percent of respondents thought it was a bad time to buy a vehicle — it's unlikely that consumers' vehicle purchases will accelerate much further from current levels.

If overall light vehicle sales are to return to a 17.0-million-unit sales pace, the most likely scenario would be a surge of pent-up demand from businesses driving fleet sales back to pre-pandemic levels. The post-pandemic pace of business light-vehicle sales averaged 6.1 million units between March 2020 and March 2023, compared to a SAAR of 8.7 million in the five years before the pandemic. However, as for consumers, high interest rates and weak sentiment on investment suggest businesses aren't ready to embark on a spending spree quite yet.

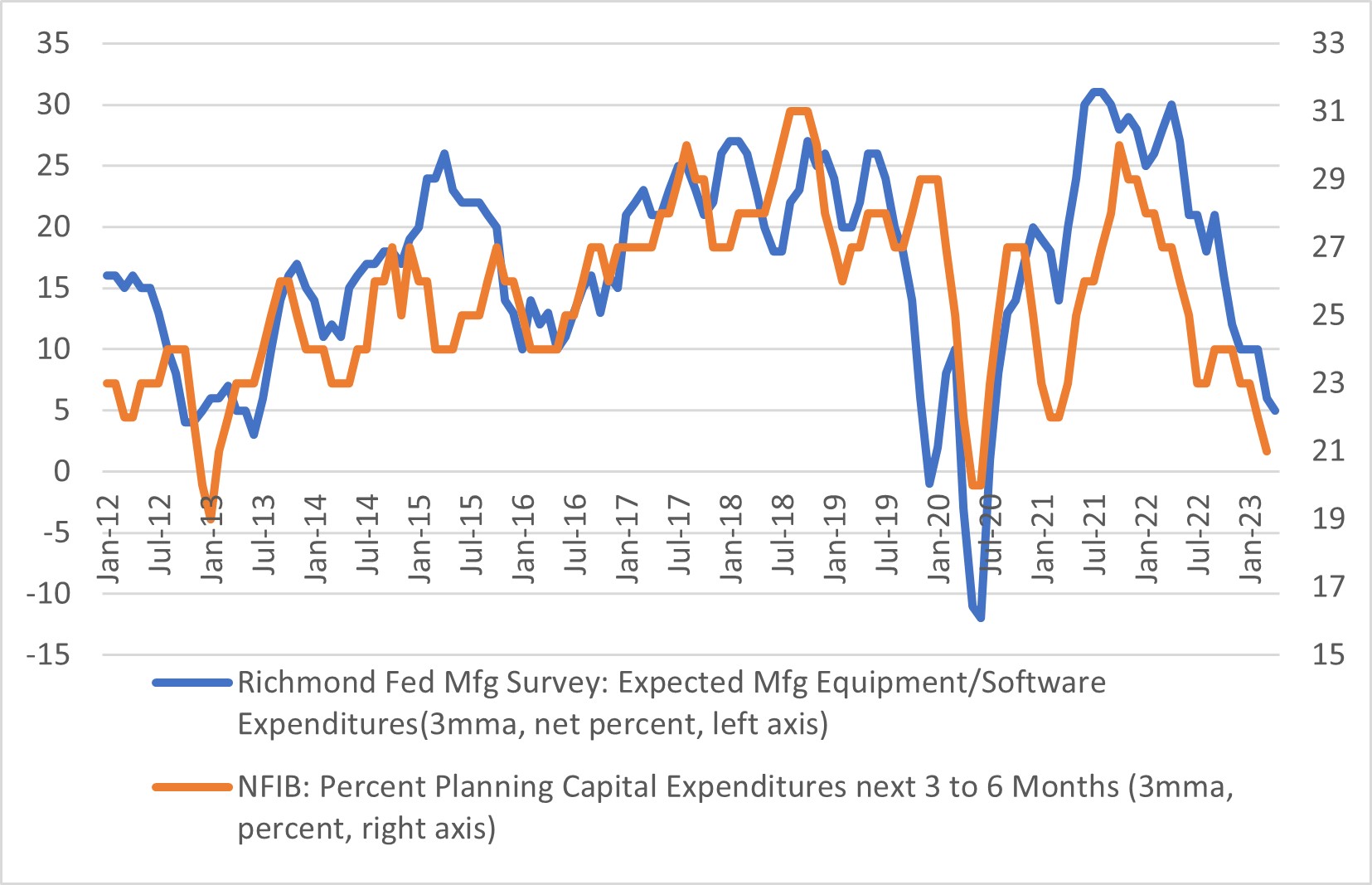

Figure 3 below shows that recent surveys of business investment sentiment have fallen to levels observed right after the COVID-19 recession. Businesses may be tapping the brakes on investment purchases, and the auto industry may be in for a rough road ahead.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us