Sentiment Is Sweet When You’re in the Driver’s Seat

Macro Minute

March 26, 2024

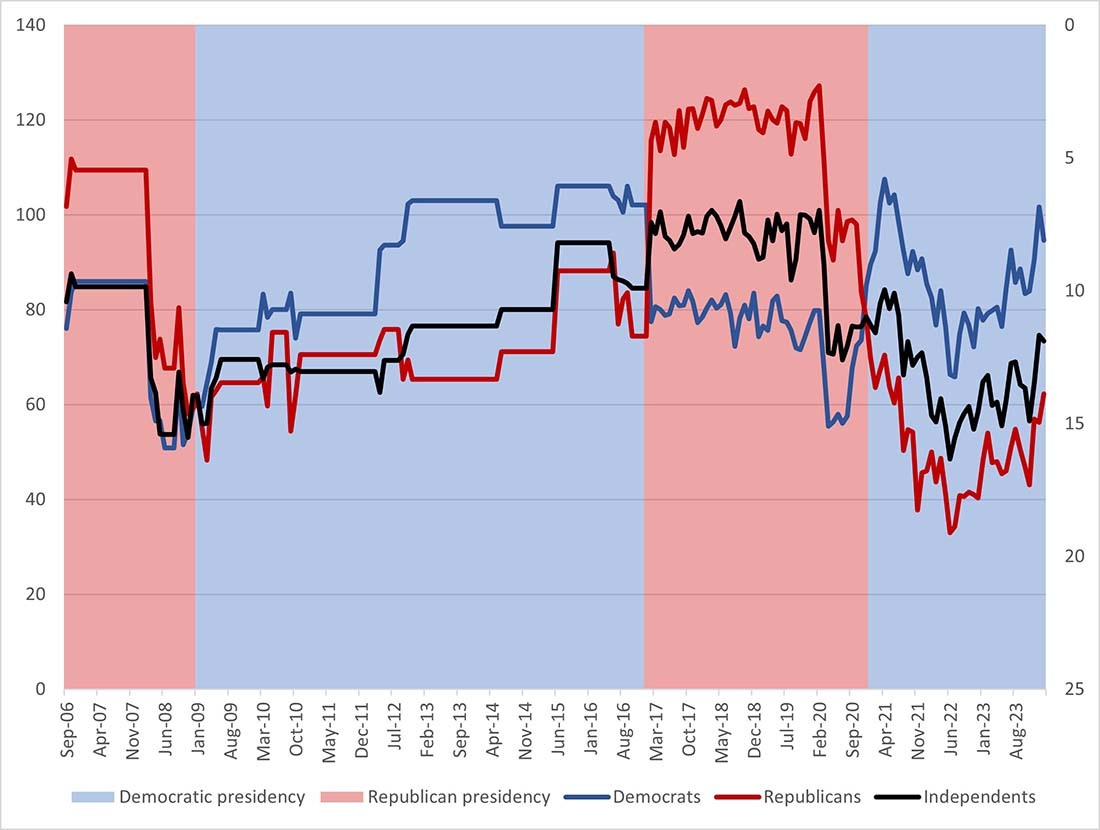

During election years, the topic of economic perceptions across the political divide inevitably becomes a hot-button issue. One economic indicator that provides a particularly clear look at this issue is the University of Michigan's (UM) Consumer Sentiment Index. Since 2017, UM's Surveys of Consumers have asked respondents about their political affiliation on a monthly basis. Prior to that, respondents were asked about their political affiliation several times in each administration, but not in every month. Figure 1 below shows consumer sentiment by political affiliation from September 2006 through February 2024, highlighting significant differences in sentiment across party lines.

The February 2024 report "Partisan Perceptions and Expectations (PDF)" indicates that, when looking across individual characteristics of survey respondents, the partisan gap in sentiment is considerably larger than the sentiment gap across income, age or education level. Also, the January 2022 report "The Partisan Economy (PDF)" indicates that the partisan sentiment gap has been widening over time. And as shown in Figure 1, consumers whose political party is in office tend to have higher sentiment than those affiliated with the party not in office.

There's another kind of sentiment gap that exists: the gap between perceptions of the economy and actual economic fundamentals (the "fundamentals gap"). In a previous post, we discussed how consumer sentiment might be linked to economic fundamentals such as the overall price level.

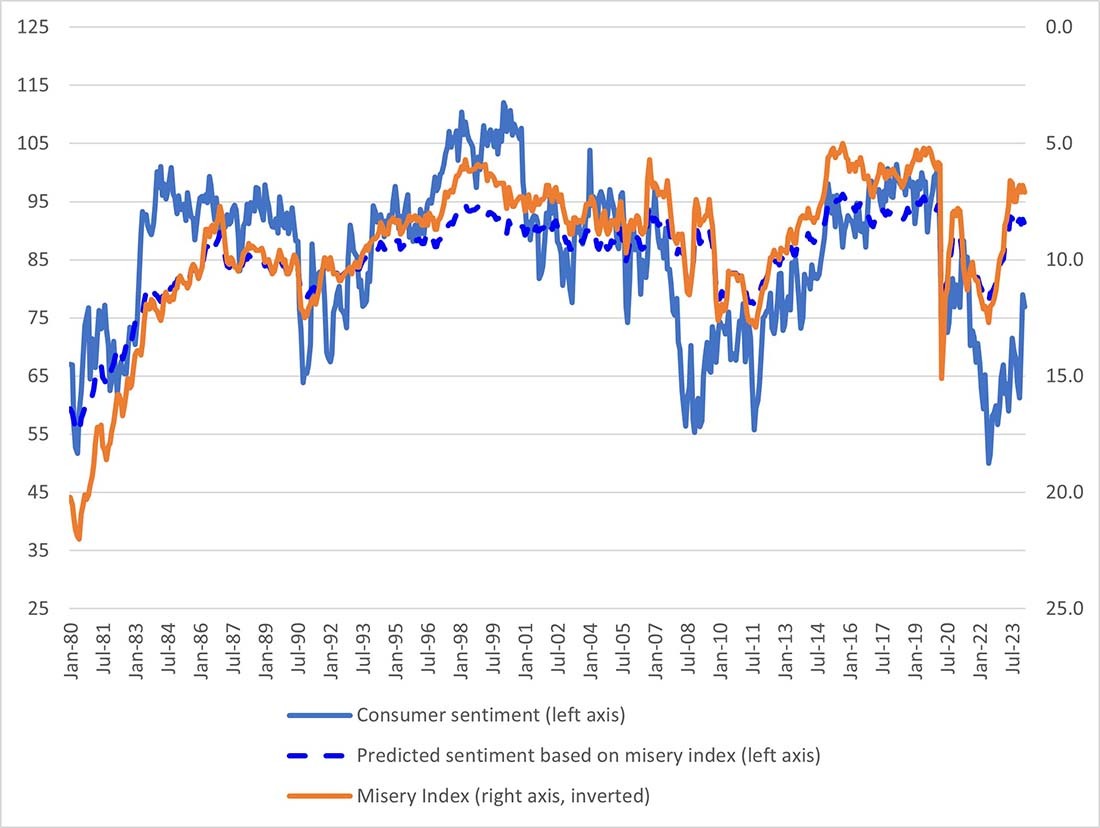

Figure 2 below shows the relationship between the consumer sentiment index in solid blue and the misery index (the sum of year-over-year CPI inflation and the unemployment rate) in orange. The misery index is indicated by the right axis, which is inverted to show how it moves in relation to the consumer sentiment index. In general, sentiment tends to rise as the misery index falls (with a correlation of -0.68), but in some periods (like today), surveyed sentiment can differ from the level of sentiment that would be predicted by the misery index, shown in the dashed blue line in Figure 2.

As with consumer sentiment, the fundamentals gap can differ based on whether the respondent's political party is currently in the White House. To see this, we compute the difference between each political affiliation's consumer sentiment and the level of overall consumer sentiment that would be predicted from the misery index. We explore how these differences change depending on whether the political party holds presidential office.1 We look at both raw differences and their absolute values: Raw differences tell us which direction that's affiliated with the incumbent president skews sentiment, and absolute values tell us how large a "mistake" that respondents who are politically affiliated with the incumbent president are making. We also look at differences in percentage terms (i.e., as a percent of predicted sentiment).

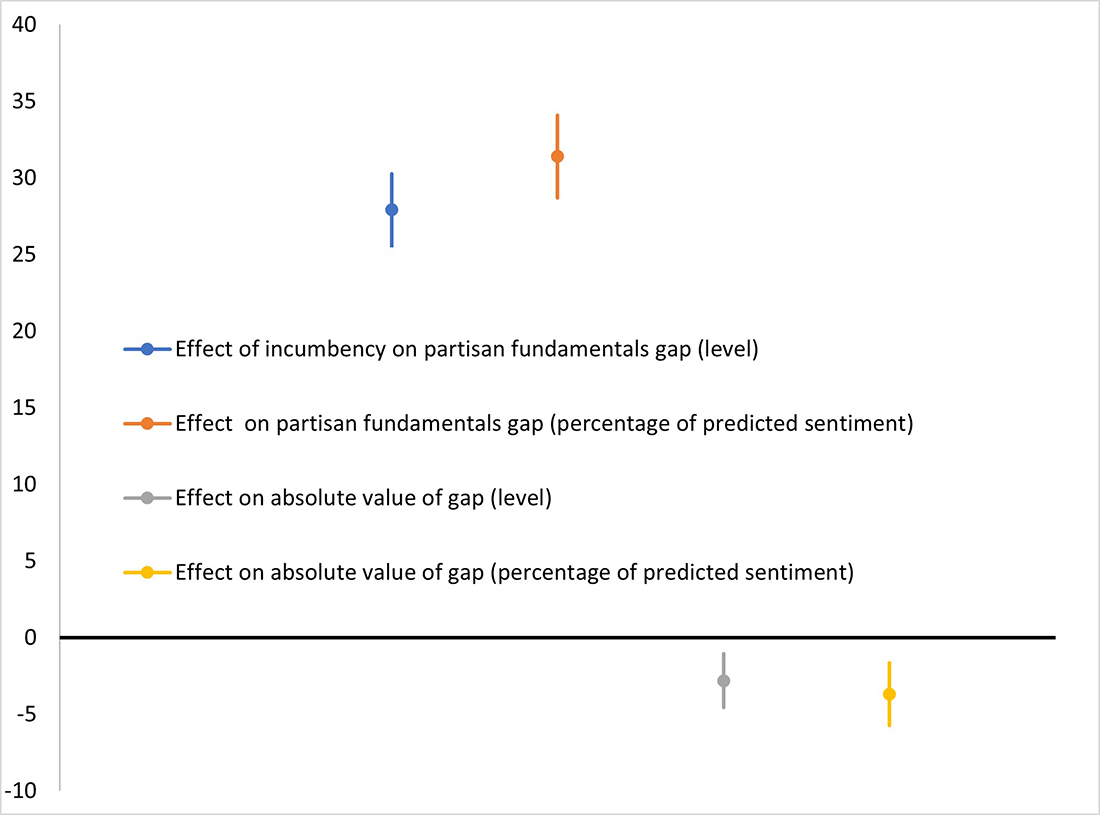

Figure 3 below shows the estimated impact of being affiliated with the incumbent on the partisan fundamentals gap. Between September 2006 and February 2024 (the time span of the analysis), being politically affiliated with the incumbent president lifted sentiment by 28 points (or 31 percent) relative to the level of sentiment predicted by economic fundamentals. Thus, we continue to find that being politically affiliated with the party in the White House is associated with more optimistic consumer sentiment.

However, being relatively more optimistic doesn't imply a greater disconnect from what economic fundamentals would imply: That is, if sentiment is generally lower than what would be predicted by economic fundamentals, then an additional factor that makes survey respondents more optimistic might cause their responses to be more consistent with the state of the economy. In fact, Figure 2 suggests that, over the period of this analysis, average sentiment was generally more pessimistic than would be predicted from the misery index, which means that the above-average sentiment of respondents affiliated with the president's party could be closer to the level of consumer sentiment that would be inferred from the misery index.

To see whether this is the case, we look at the absolute value of the partisan fundamentals gap — in other words, the distance between each political group's sentiment score and the score that would be inferred from the misery index. Figure 3 shows that being politically affiliated with the incumbent president lowers the absolute value of the partisan fundamentals gap, which means that respondents who were affiliated with the party in power had sentiment that was closer to the level that would have been predicted by the misery index. On average over this time period, being affiliated with the president's party was associated with a 2.8 point (or 3.7 percent) reduction in the distance between sentiment and the level of sentiment predicted by the misery index.

These findings could suggest that being affiliated with the party in power makes consumers more engaged and, in turn, more informed about the state of the economy, at least over the past 20 years. However, it's unclear whether these results would hold in periods when average sentiment is more optimistic than would be inferred by economic fundamentals, such as the pre-2006 period. In such periods, a shot of optimism from political incumbency could lift sentiment even further above levels predicted by fundamentals.

1

Formally, we run the following regression: . On the left-hand side is the difference between consumer sentiment for respondents with political affiliation (Democrat, Republican or Independent) and the value of overall consumer sentiment predicted by the misery index. On the right-hand side are indicators for Democrat and Republican, as well as an indicator for whether the president is currently a member of party . We estimate the regression using data from September 2006 through February 2024 (shown in Figure 2).

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us