Do Student Loans Drive Up College Tuition?

Economic Brief

August 2022, No. 22-32

To what extent do student loans drive up college tuition? In ongoing research, we find the answer has varied substantially over time. Following large expansions in student loan limits in 1993 and 2007, our results show further increases in loan limits would have essentially zero effect. In contrast, in the years before those expansions, our estimates indicate tuition would have increased $0.10 for every $1 increase in borrowing limits.

The Federal Student Loan Program (FSLP) has existed under various names since the late 1960s. The amount that students can borrow through the program to finance their college tuition has risen steadily (though unevenly) since that time, with total borrowing for undergraduate students currently limited to $57,500.

Alongside the increase in loan limits, college tuition has risen considerably since the FSLP's advent. In a famous New York Times op-ed titled "Our Greedy Colleges," then-Secretary of Education William Bennett wrote "increases in financial aid in recent years have enabled colleges and universities blithely to raise their tuitions." Over 30 years later, this claim — known as the Bennett hypothesis — remains the subject of debate.

But more importantly for policymakers: Is the hypothesis true? Was Bennett correct that increases in student loan limits pass through to college tuition, and if so, what is the magnitude of the passthrough rate?

In this article, we report on one facet of our working paper "Accounting for Tuition Increases Across U.S. Colleges (PDF)" that sheds critical light on this debate. Our analysis shows that the passthrough rate from student loans to tuition varies drastically over time based on economic and policy conditions. In other words, there is no such thing as "the" passthrough rate: Passthrough rates were at their highest in the late 1980s — when Bennett articulated his hypothesis — before subsequently dropping to almost zero in the mid-to-late 1990s, steadily rising until 2006-2007 and finally collapsing to near zero in the late 2000s.

This pattern helps explain some of the conflicting evidence from empirical studies on the passthrough rate of student loans. We will explain these patterns, the reason for their variation and why passthrough rates for subsidized and unsubsidized loans are at times different and at times similar.

Modeling the Impact of Student Loans on Tuition

The passthrough rate for student loans is defined as the amount by which net tuition goes up in response to a $1,000 increase in borrowing limits, then divided by $1,000. For example, if borrowing limits rise $1,000 and net tuition goes up by $300, the passthrough rate is 0.3 ($300/$1,000).

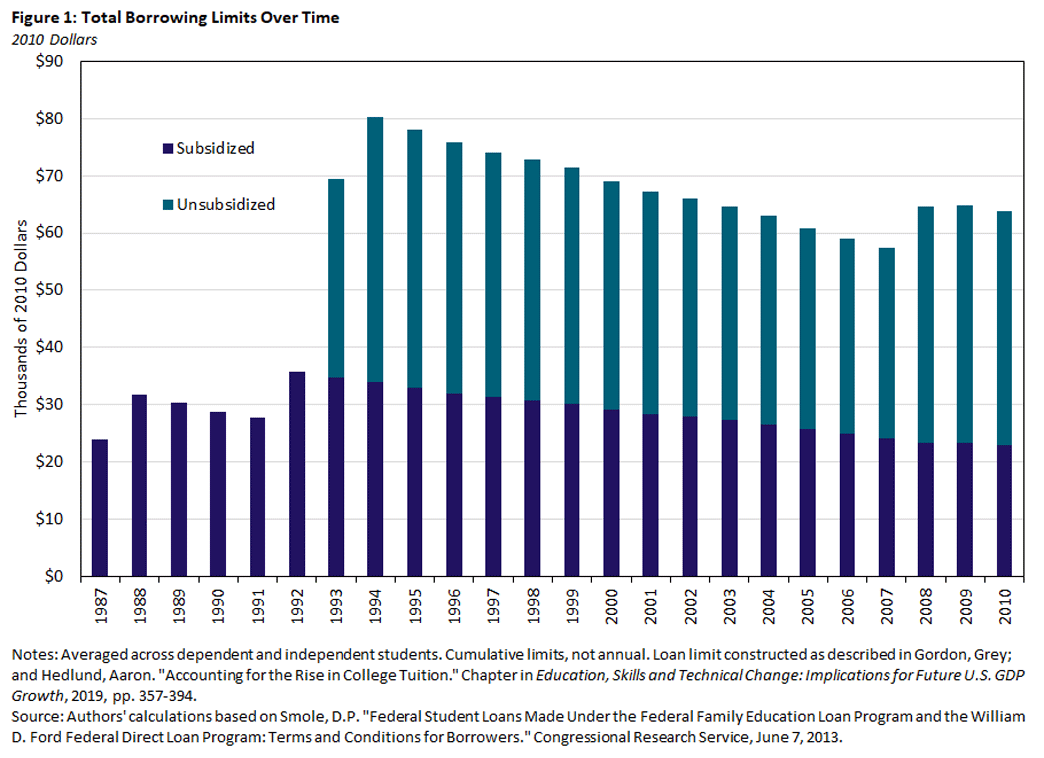

Because policy details and economic forces differ somewhat between subsidized and unsubsidized loans, we consider each passthrough rate separately. Moreover, within a category, there is a distinction between annual and total borrowing limits. Figure 1 displays the total limits adjusted for inflation to 2010 dollars. Because Congress increases the statutory limits only sporadically, the nominal value is often flat, which causes the real value to decline gradually in between legislative changes. Also, unsubsidized borrowing did not enter the picture until 1993, as indicated by the blue bars.

Our passthrough estimates come from a computational, data-disciplined model of the higher education market that takes into account the decisions of colleges, students and workers as well as the unique economic and institutional environments where their interactions take place.1

In the model, high school graduates make college application decisions, including whether to apply at all. College-bound students then decide how to finance their education, including how many and which types of student loans to take out, subject to their individual eligibility as determined by the FSLP. Colleges decide whom to admit, how much to charge each student (tuition minus institutional aid) based on their academic backgrounds and family financial situations, and how much to spend on quality-enhancing budget items. Once no longer in school, workers allocate their financial resources among consumption, saving and student loan repayment, which also includes the option to default on their loans, subject to the penalties and restrictions that the FSLP imposes.2

Each model element affects the other pieces. For example, one college's pricing decisions impacts how other colleges set tuition and where students decide to apply. These linkages capture the rich interactions and sources of feedback in the data that simpler, model-free statistical comparisons overlook.

After disciplining the parameters of the model with several detailed data sources, we establish that the model can generate the actual observed evolution of the college market post-1987 — especially rising tuition and changing enrollment patterns across college types — thus validating the model as a reliable laboratory economy in which to conduct counterfactual experiments.

In particular, we use the model to simulate the effects of increased loan limits by comparing the actual evolution of the college market in recent decades (which the model is able to successfully replicate) to the model's simulation for how college tuition would have evolved had loan limits remained static. This comparison then allows for calculation of time-varying passthrough rates.

Do Student Loan Limit Increases Pass Through to Tuition?

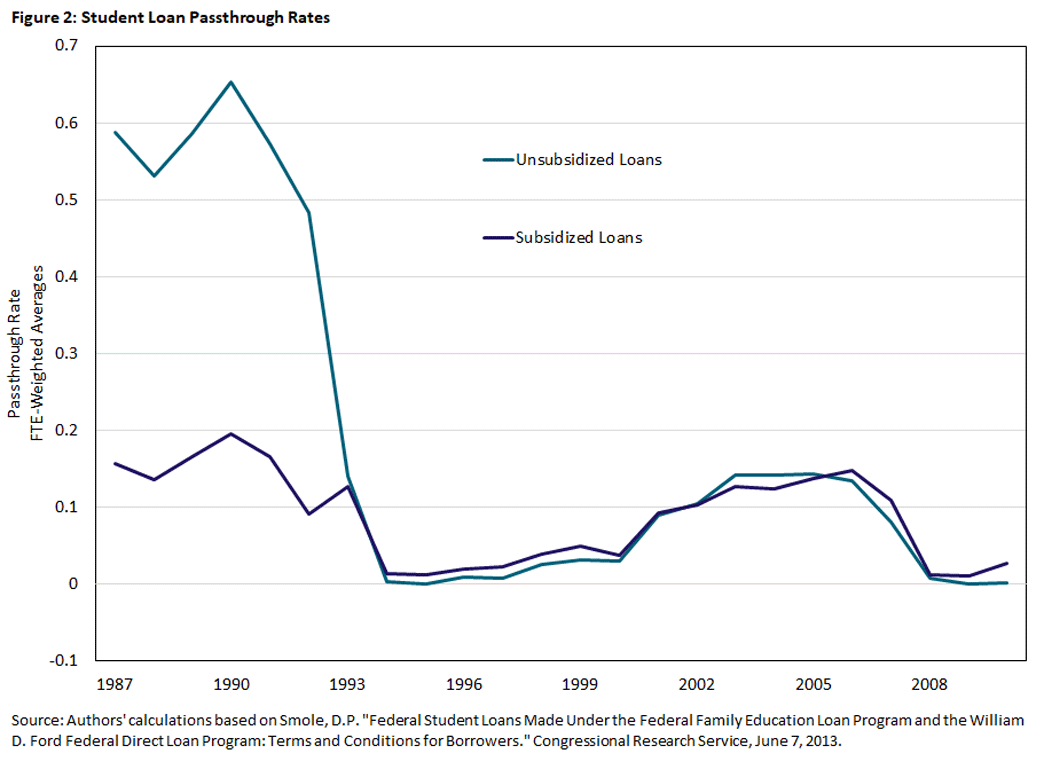

Figure 2 reports the passthrough rates for subsidized and unsubsidized loans.

One striking pattern (which we return to in more depth later) is the near-identical passthrough rates for subsidized and unsubsidized loans after 1993 despite the loan programs differing in important ways in terms of their eligibility requirements and generosity.

More broadly, the time-varying nature of loan passthrough rates emerges as a salient pattern. Arguably the most noticeable dynamics occur in the immediate aftermath of 1993 and 2008, when loan passthrough rates rapidly decline from the prior year. The key fact linking these periods is that both 1993 and 2008 were years of substantial expansion in the FSLP, as Figure 1 indicates.3

Why Passthrough Rates Rise and Fall

Why might large loan limit expansions decrease passthrough rates? Intuitively, if loan limits are tight, borrowers feel more constrained, and their demand for college will be more responsive to an expansion in the capacity to borrow. By contrast, if loan limits are loose, more borrowers are likely to be at or near the point where they're already taking out the largest loan that they are willing to borrow. Thus, the demand for college will not respond as strongly to a further relaxation of borrowing limits. To put it differently, the availability of student loans has declining marginal effects. For example, the effect of, say, the first $10,000 in loan availability is greater than the effect of the second $10,000 in loan availability.

Prior to 1993, eligibility requirements meant that some students did not qualify for subsidized loans but may have still been borrowing constrained, implying that they either had to go to a cheaper college than the one they wanted or cut back drastically on consumption while in college. The introduction of unsubsidized loans allowed these students to pay higher tuition, causing an increase in demand that put upward pressure on prices. With fewer borrowing-constrained students remaining after this expansion, any near-term further increase in borrowing limits was bound to have less of an impact on college demand and, therefore, tuition prices.

However, after longer periods of time, the inflation-induced erosion of the real value of the statutory borrowing limits combined with rising tuition from other causes gradually increased the number of constrained borrowers (and thus, the passthrough rate) once again until the next time Congress raised loan limits, causing the passthrough rate to again fall.

Why Evidence of Student Loan Passthroughs Has Been Mixed

As mentioned in the introduction, the Bennett hypothesis has adherents as well as detractors. Part of the controversy is because the empirical evidence on it is mixed, and our results shed light on these mixed estimates.

To pick just one paper, the 2019 article "Credit Supply and the Rise in College Tuition: Evidence From the Expansion in Federal Student Aid Programs" finds that unsubsidized loans have a passthrough rate of 0.18 before 2008, which comports well with our model-implied estimate.4 In contrast, the authors' estimate for the post-2008 period is statistically insignificant, which means they cannot rule out statistically that the passthrough rate is in fact 0. However, this result, too, is exactly what our model predicts: Following the large 2008 loan expansion, students were no longer credit constrained, and any subsequent loan limit increase should not pass through to tuition.

Interestingly, when Bennett penned his op-ed, our model implies passthrough rates were essentially at their all-time highs given the large number of borrowing-constrained prospective students. After the introduction of unsubsidized loans in 1993, however, the number of borrowing-constrained students fell, thereby significantly attenuating the forces driving previously high passthrough rates, at least temporarily.

The credit constraint intuition above also explains why the passthrough rate for unsubsidized loans upon their introduction in 1993 was much higher than for subsidized loans. In particular, when the unsubsidized loan program launched, it addressed a large set of prospective college students who were credit constrained yet did not meet the eligibility requirements for the subsidized loan program. Thus, each $1,000 of additional borrowing capacity for these students had a large impact on their willingness to pay for college, which led to a high passthrough rate to tuition. By contrast, students who qualified for subsidized loans already had access to nearly $30,000 of total subsidized borrowing capacity. Thus, the ability to borrow another $1,000 did little to further increase the amount these students were willing to pay for college, translating to a lower passthrough rate.

It is still striking the extent to which the passthrough rates for these two loan types converged after 1993. An examination of the structure of these programs gives some clues. First, although the terms for subsidized loans are more generous — namely, the government pays the interest on subsidized loans while the student is enrolled, whereas unsubsidized loans accrue interest — the treatment of loan interest is important only once the borrower has left college and entered the loan repayment phase. Both programs enhance students' upfront ability to pay for college by the same amount. In particular, whether it's coming from a subsidized or unsubsidized loan, $1,000 of additional borrowing capacity translates to $1,000 of additional upfront purchasing power, even though the subsequent loan servicing costs differ across loan types.

Second, as alluded to previously, subsidized loans include eligibility requirements related to financial need. Specifically, the government solicits income and asset information about each dependent student's family and calculates an expected family contribution (EFC) that reflects the amount of college expenses the family should be able to cover on its own. Students can then take out subsidized loans for any amount above the EFC up to the lower of the total cost of attendance and the loan limit. If the loans prove insufficient, the student must either forgo attending that college or turn to other modes of financing like unsubsidized loans, which have broader eligibility because they do not depend on financial need.

That said, as a practical matter, because passthrough rates are weighted by enrollment, they significantly reflect the situation at large public schools, where many students have a low EFC and, thus, have eligibility for subsidized loans. Thus, expansions of both loan types have broad impacts on an enrollment-weighted basis and often give rise to similar passthrough rates. For this argument, it is important that the subsidized and unsubsidized limits are not too different to begin with. Otherwise, whichever limit is smaller will tend to have a larger passthrough rate, as we already established.

Conclusion

Is Bennett's 1987 famous assertion about high passthrough rates of student loan expansions to higher tuition correct? Our model indicates that the answer depends on the time period. Back in 1987, it appears that he was correct, because a significant fraction of students were borrowing constrained and thus primed to be responsive to any expansion in their ability to borrow.

However, after the creation of unsubsidized loans largely satiated borrowing needs, the response of tuition to further increases in borrowing limits temporarily evaporated for about eight years. As tuition grew over time for a host of other reasons (which we document in our analysis), credit constraints started to bind again, causing passthrough rates to increase. The last big loan expansion in our sample, which occurred in 2008, again effectively eliminated credit constraints and brought the passthrough rate back to zero.

In sum, was Bennett right? Sometimes yes, and sometimes no. There is no such thing as a fixed single passthrough rate. Rather, the passthrough rate is time-varying, which helps reconcile the wide range of empirical estimates from the literature and begs for further investigation into the time-varying nature of passthrough rates.

Grey Gordon is a senior economist in the Research Department at the Federal Reserve Bank of Richmond. Aaron Hedlund is an associate professor in the Economics Department of the University of Missouri-Columbia.

Additional Resources

- Economic Brief: The Potential Impact of Public Service Student Loan Forgiveness in the Fifth District

- Economic Brief: Should More Student Loan Borrowers Use Income-Driven Repayment Plans?

- Econ Focus: Student Debt vs. Homeownership

- Econ Focus: Education Without Loans

1

The inclusion of workers is essential to the model — even though the analysis is focused on the higher education market itself — because prospective college students observe the evolving risks and rewards workers face from investing in college, which in turn feed into rich changes in the demand for college.

2

Income-based repayment is not an option in the model.

3

There was also a notable increase in 1994 in unsubsidized loans, which brings the passthrough rate down to zero. The FSLP is a bit more complicated than what we have said thus far. In particular, there are separate limits for dependent and independent students. We average these, placing a 37 percent weight on the independent limit in proportion to the fraction of independent students reported in the report "Findings From the Condition of Education 2002: Nontraditional Undergraduates." There is also no unsubsidized limit, but rather a combined limit (of subsidized plus unsubsidized).

4

Our work in progress "Accounting for Tuition Increases Across U.S. Colleges (PDF)" relates our passthrough rate findings to comparable estimates in the literature, which has not emphasized the time-varying nature of passthrough rates or credit constraints. One exception is the 2007 paper "The Changing Role of Family Income and Ability in Determining Educational Achievement." It directly argues for the time-varying nature of credit constraints by showing that the importance of parental income (which should influence how credit constrained one is) increased substantially from the NLSY79 (a dataset following youth in 1979) to NLSY97 (which follows youth from 1997 on) for determining attendance at two-year versus four-year colleges and hours worked in college.

To cite this Economic Brief, please use the following format: Gordon, Grey; and Hedlund, Aaron. (August 2022) "Do Student Loans Drive Up College Tuition?" Federal Reserve Bank of Richmond Economic Brief, No. 22-32.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us