Services Hitting a Snag on Snarled Supply Chains?

Macro Minute

February 1, 2022

How have snarled supply chains affected goods manufacturers and services providers in the Richmond Fed's Fifth Federal Reserve District? As mentioned in a couple of earlier posts last October and November, there's a bewildering mix of data we could track to try to answer this question.

"It may seem strange that services providers have become more sensitive to global supply chain stress than manufacturers."

Recently, economists at the New York Fed have published a new Global Supply Chain Pressure Index (GSCPI). The index condenses information from a number of indicators — including transportation and freight costs, order backlogs, inventories and supplier delivery times — into a single measure of global supply chain pressure. In this post, we use the GSCPI to explore how global supply chain disruptions have affected our region.

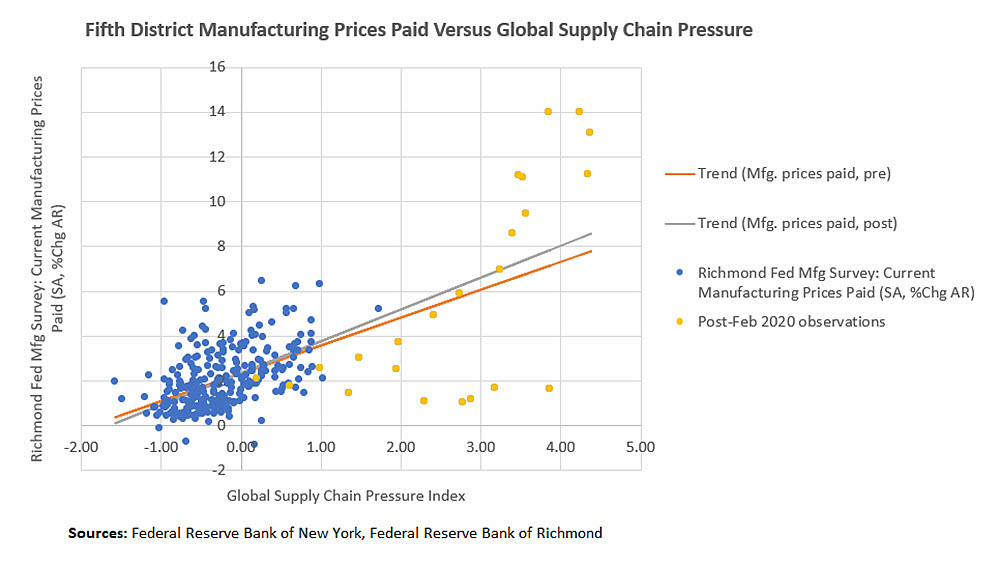

Figure 1 plots the GSCPI against the "prices paid" (i.e., for inputs) measure from the Richmond Fed's Survey of Manufacturing Activity. The index is normalized so that 0 indicates that the index is at its average value. Positive values represent how many standard deviations the index is above this average value, while negative values represent the opposite. The manufacturing survey's prices measure tracks the average percentage change in prices paid over the past 12 months.

The figure shows the estimated linear relationship between the GSCPI and the price measure using only pre-pandemic (September 1997-January 2020) data in the orange line and the full data through December 2021 in the grey line. Observations after February 2020 are colored in yellow.

For manufacturers in our region, there has been little change to the relationship between global supply chain pressures and prices since the start of the pandemic, with the orange and grey lines sharing a similar slope. In the early stages of the pandemic, surveyed changes in input prices fell below what levels of the GSCPI would imply while recent survey responses have indicated input price pressures above levels implied by the trend. These two forecast "misses" roughly offset and leave the slope of the line unchanged.

Based on the full sample, all else equal, a one standard deviation increase in global supply chain stress causes the 12-month growth rate of prices paid to rise by 1.4 percent. In the latest GSCPI reading from December 2021, global supply chain pressure was more than 4 standard deviations above its average, suggesting a significant impact of global supply bottlenecks on manufacturers' prices paid. Indeed, the prices paid measure in the manufacturing survey rose to 13.98 in December, versus a long-run average (with data beginning in 1997) of 2.38, and the latest reading from January 2022 reached a record high of 14.32.

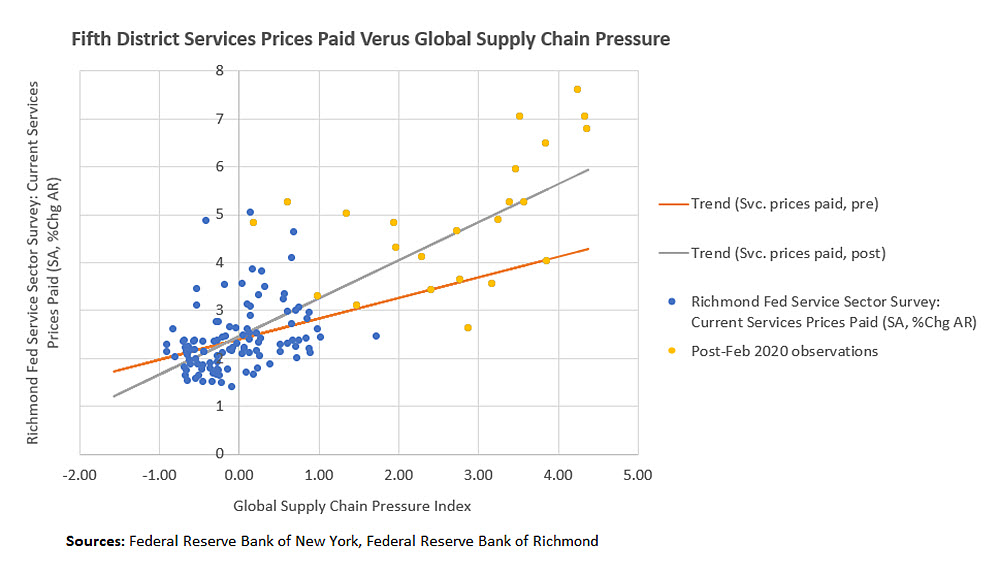

In contrast, for services providers in the Fifth District, the sensitivity of prices to global supply chain pressure increased after the pandemic started. In Figure 2, we plot "prices paid" in the Richmond Fed's Survey of Service Sector Activity against the GSCPI.

Prior to the pandemic, a one standard deviation increase in supply chain pressure was associated with a 0.4 percentage point increase in the 12-month growth rate of prices paid. But after February 2020, changes in prices paid by services providers were largely higher than predicted by the pre-pandemic relationship, increasing the slope of the trend line. Incorporating the full data through December 2021, a one standard deviation increase in supply chain pressure is now estimated to cause a 0.8 percentage point increase in the 12-month growth rate of prices paid.

It may seem strange that services providers have become more sensitive to global supply chain stress than manufacturers. But alongside the typical activities one might have in mind when thinking of services — like hairdressers, store cashiers, restaurant waitstaff and computer programmers — the Richmond Fed's services survey includes firms in the agriculture, mining, utilities and construction industries (and might be more accurately called a "nonmanufacturing" survey). For instance, construction firms make up about 9 percent of the panel of firms surveyed in the services survey. Businesses in these industries may be very dependent on the pricing and availability of materials and commodities, and recent supply chain disruptions may have caused a dramatic change in the way they do business.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us