How Pump Prices Play With Monetary Policy

Macro Minute

October 4, 2022

This summer, the national average price of gasoline declined for 98 days straight, finally ending Sept. 20. Falling gas prices contributed to an easing in inflation, with monthly headline CPI growth dropping to 0 percent in July and 0.1 percent in August. Historically, declining gas prices have been correlated with improvements in consumer sentiment and expectations for the future. The Michigan consumer sentiment index improved from 50.0 in June to a preliminary reading of 59.5 in September.

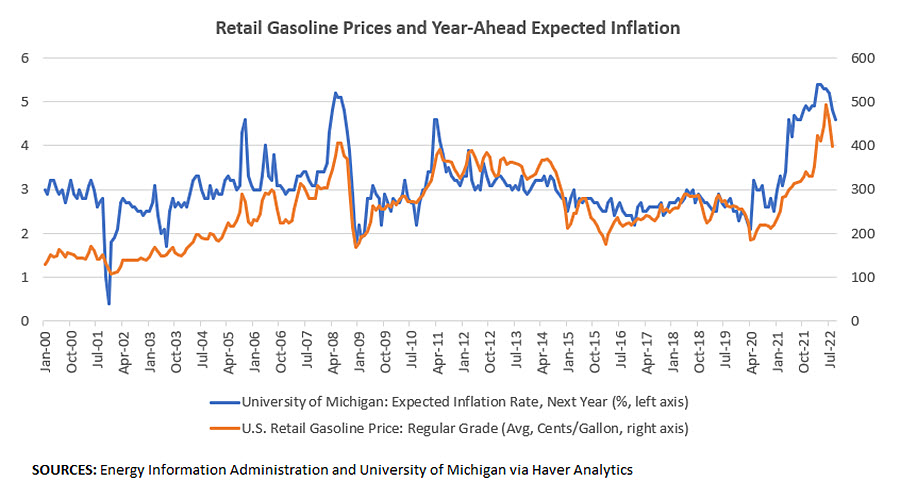

Cheaper gas prices have also affected households' expectations for near-term inflation. As shown in Figure 1 below, households' year-ahead inflation expectations in the Michigan survey fell to 4.6 percent in September's preliminary survey reading from 5.3 percent in June.

The gas-driven improvement in near-term inflation expectations has worked in tandem with the FOMC's rate increases to shift the stance of monetary policy towards levels that will bring inflation down. Given any level of the nominal policy rate, a decline in inflation expectations lifts the "ex ante" real rate. This refers to the nominal interest rate minus expected inflation, and it is this rate that, according to economic theory, should factor into household and business decision making. If expected inflation falls and nominal rates rise at the same time, the ex ante real interest rate rises even further, as both forces work in the same direction.

Ultimately, whether monetary policy is stepping on the gas or tapping the brakes of the economy is determined by the distance between the ex ante real interest rate and a threshold called the natural rate of interest, or the interest rate where inflation is at target and monetary policy is neither speeding up economic activity nor slowing it down. The natural rate of interest (which economists call "r-star") is unobserved and must be estimated from economic and financial data.

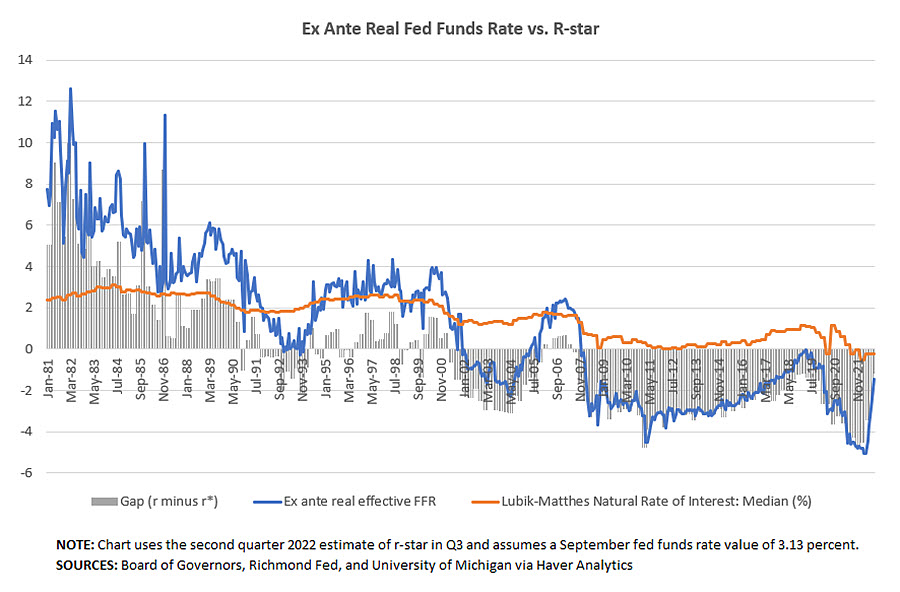

Figure 2 below shows one such estimate of r-star by economists Thomas Lubik and Christian Matthes as well as the gap between r-star and the latest monthly value of the ex ante real interest rate, calculated using the one-year ahead inflation expectation from the Michigan survey.

Assuming that September's r-star estimate is the same as the latest estimate from the second quarter — and with near-term inflation expectations falling by 20 basis points in September and the nominal fed funds rate rising by 75 basis points following the September FOMC meeting — the gap between r and r-star has narrowed from 346 basis points in June to 121 basis points in September. The narrowing gap points to a tighter stance of monetary policy, a necessary condition to get inflation closer to target.

The fact that this particular measure of the r minus r-star interest rate gap remains negative may not necessarily be a cause for concern. It may stem from the bias in survey measures of household inflation expectations: Starting in the mid-1990s, households seem to always expect higher inflation than actually materializes, which biases the ex ante real interest rate measure downwards.

In comparison, the r-star measure in Figure 2 is an unbiased measure. As a result, the level of the gap will tend to be negative, so it's best compared to its own previous values. By that comparison, monetary policy is as tight as it's been since the first quarter of 2019, when the gap was 119 basis points.

Still, further tightening may be needed. The latest Summary of Economic Projections suggests rates could peak next year between 3.9 percent and 4.9 percent. Part of the reason for the wide range of projections stems from uncertainty about the natural rate, as r-star estimates tend to have wide confidence intervals. There's also uncertainty around how the economy will evolve: As this summer's dance of gas prices, inflation expectations and rate hikes has shown, a multitude of factors can affect the restrictiveness of monetary policy, and not all are in the FOMC's control.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us