Of Soft, Hard and Aborted Landings

Economic Brief

January 2024, No. 24-02

In this article, we compare two rate cycles from the 1980s (one of which resulted in a soft landing) with our current rate cycle. We describe the type of landing that resulted from each rate cycle through changes in the federal funds target rate, inflation, unemployment and consumption growth. Importantly, since monetary policy is not carried out in a vacuum, we underscore the importance of external shocks in affecting the economy and, ultimately, in determining (along with monetary policy) the rigidity of the landing.

Over the past 22 months, the Federal Open Market Committee (FOMC) has raised the federal funds rate target range by more than 500 basis points to combat the elevated levels of inflation. As inflation begins to descend toward the Federal Reserve's 2 percent target without significant downturn in the economy so far, it is only natural to ask whether a soft landing is in view.

This article compares the current rate cycle to the rate cycles in 1983 and 1987 and the events that led to their soft or hard landings. As in our previous work "A Rate Cycle Unlike Any Other," we define a rate cycle as beginning in the first month that the FOMC raised rates and ending in the last month that the FOMC lowered rates.

Rate Cycle: March 2022 Through Today

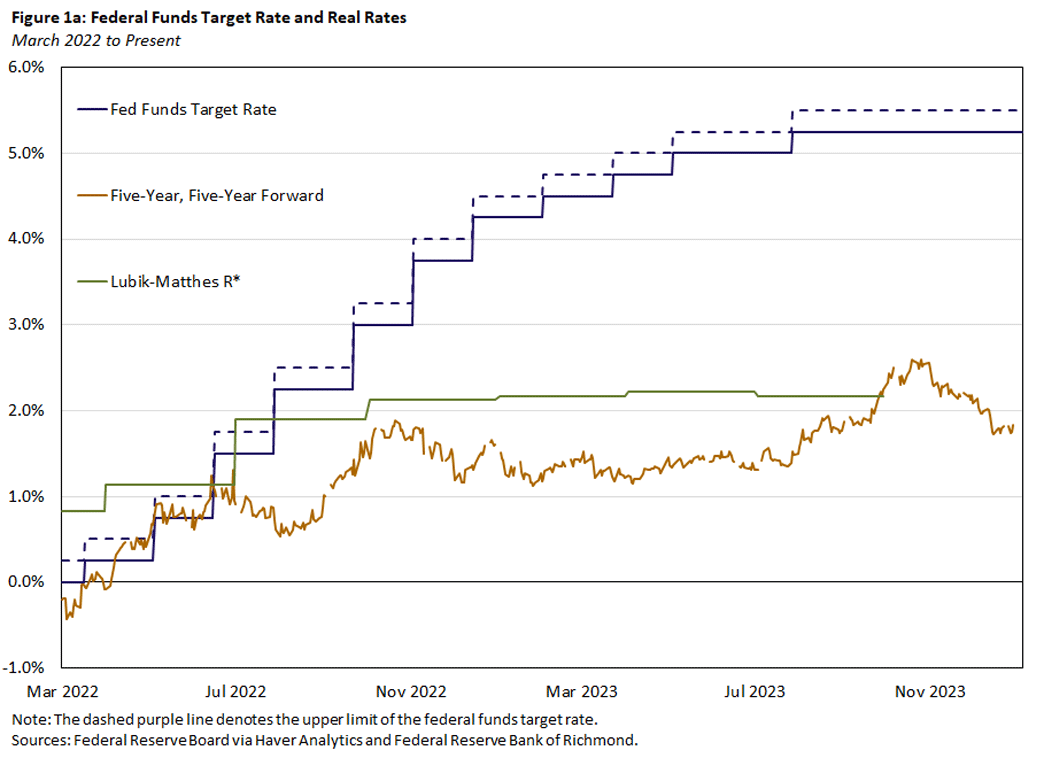

In March 2022, the federal funds target range was 0 to 0.25 percent. Less than two years later, the federal funds target range now sits at 5.25 to 5.5 percent. Figure 1a charts the change in the federal funds effective rate since March 2022, as well as the TIPS five-year, five-year forward rate and the neutral rate of interest (r*, calculated by economists Thomas Lubik and Christian Matthes) over the same period.1 We define r* as the level of real interest rate at which the economy is neither expanding nor contracting and, thus, where inflation is expected to be relatively stable.

We can see that, prior to October 2023, r* was above the market real rate as measured by the TIPS five-year, five-year forward rate. This suggests that while policy was getting progressively tighter, its level may have nevertheless been somewhat accommodative. However, policy has recently entered a phase where the real interest rate is now at or exceeding the neutral rate.

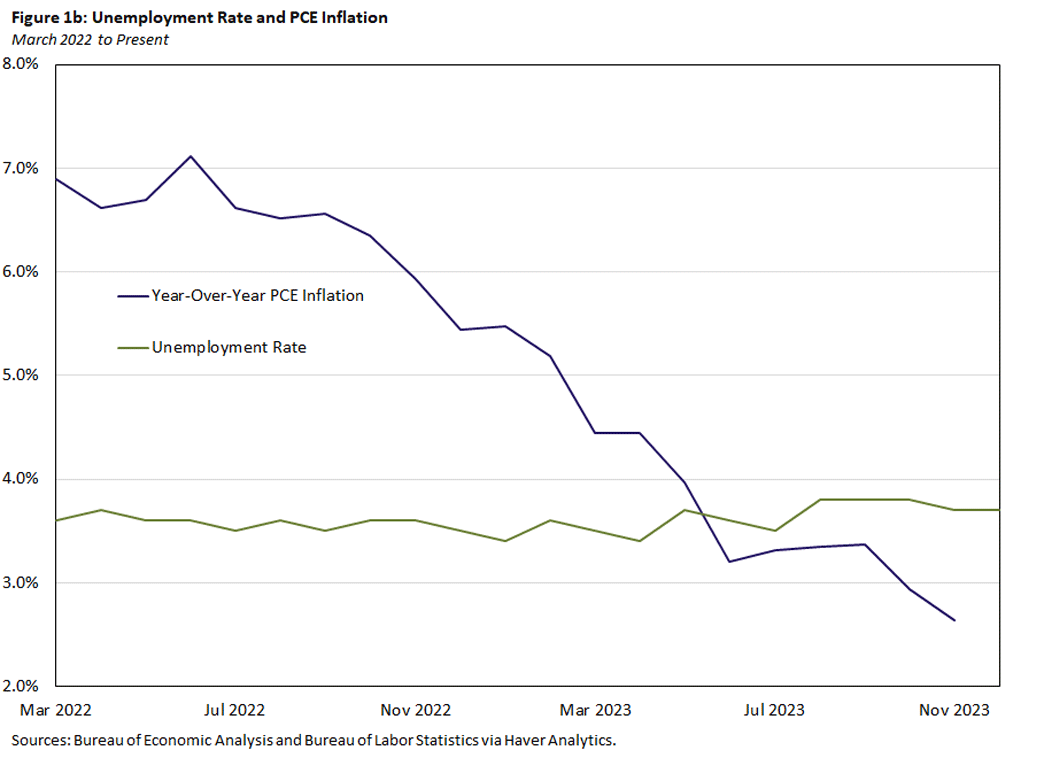

When the FOMC first raised the federal funds target rate in March 2022, the personal consumption expenditures (PCE) price index (the Fed's preferred measure of inflation) had increased to 6.9 percent year over year, well above the Fed's target of 2 percent. Since then, as seen in Figure 1b, PCE inflation has fallen to 2.6 percent (as of the most recent reading in December), while the unemployment rate's mark of 3.7 percent in December is only 0.1 percentage points above the March 2022 rate of 3.6 percent.

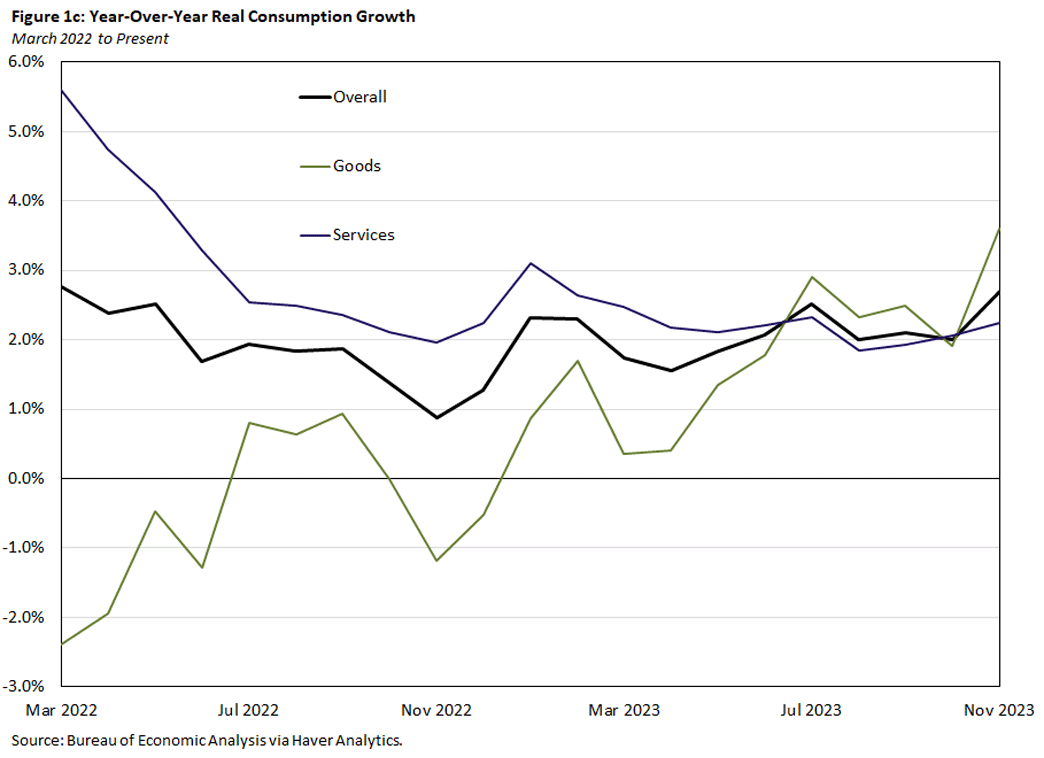

Meanwhile, consumption growth has remained surprisingly strong. As seen in Figure 1c, overall year-over-year real consumption growth has not shown any significant declines, and its November rate of 2.7 percent is only 0.1 percentage points below its March 2022 rate of 2.8 percent. Goods consumption has also been steadily increasing across the rate cycle, and despite services consumption initially falling, its November rate of 2.2 percent is in line with its longer-run average. This resilience in consumption growth and the unemployment rate have been welcome — though not necessarily taken for granted — following the amount and pace of increases in the federal funds rate.

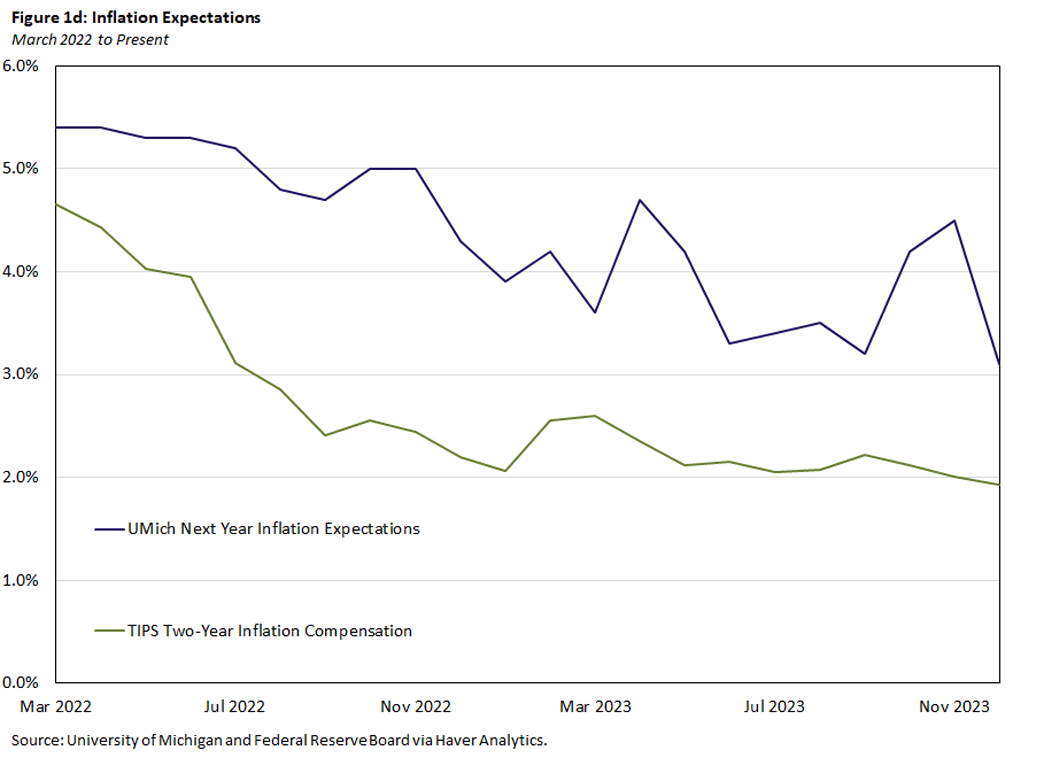

In Figure 1d, we chart inflation expectations as implied by the University of Michigan's Survey of Consumers for the next year as well as TIPS two-year inflation compensation. We see inflation expectations continuing to improve and trending downward since the start of the rate cycle. The continued improvement of inflation while maintaining strong consumption growth and a low unemployment rate makes a future soft landing appear increasingly plausible and — given the FOMC's decision in its last three meetings to hold rates steady — perhaps even likely.

Rate Cycle: March 1983 to August 1986

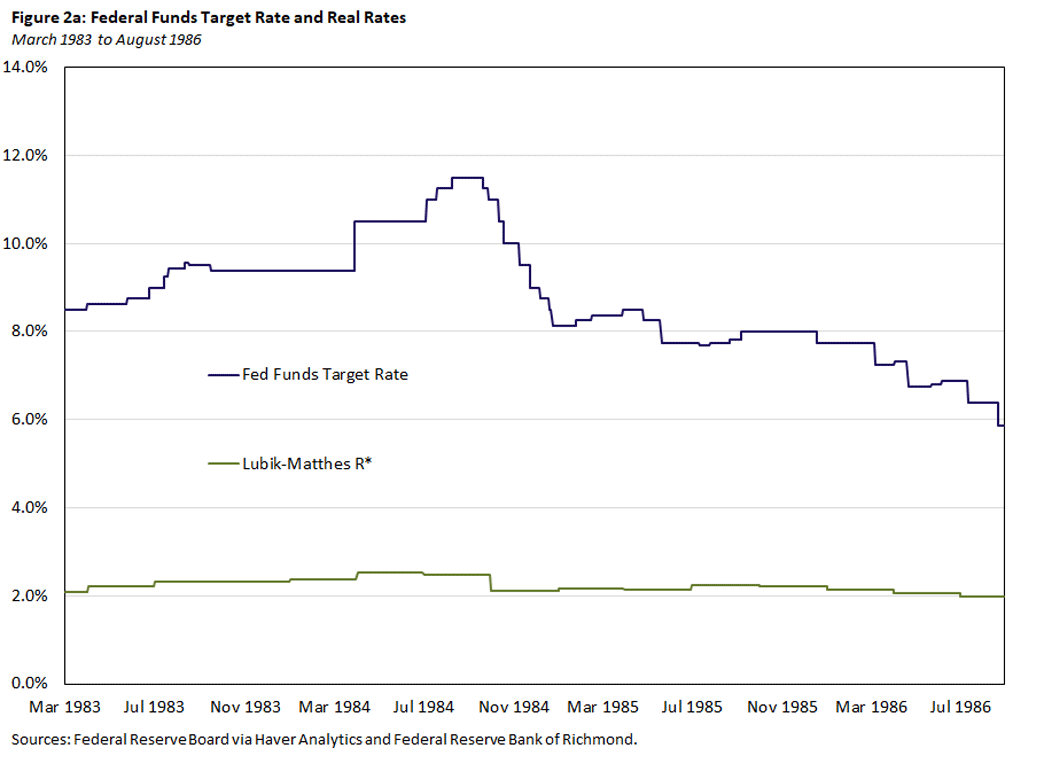

To place the current rate cycle in somewhat similar historical context, we look back at the rate cycle covering the period March 1983-August 1986. Inflation was still elevated after the late 1970s and early 1980s, prompting the FOMC (chaired by Paul Volcker at the time) to raise the federal funds target rate. When the Fed began raising rates in March 1983, the federal funds target rate was 8.5 percent. In August 1984, at the peak of the rate cycle as seen in Figure 2a, the federal funds target rate was 11.5 percent. It was then slowly lowered to its trough of 5.875 percent over the next two years.

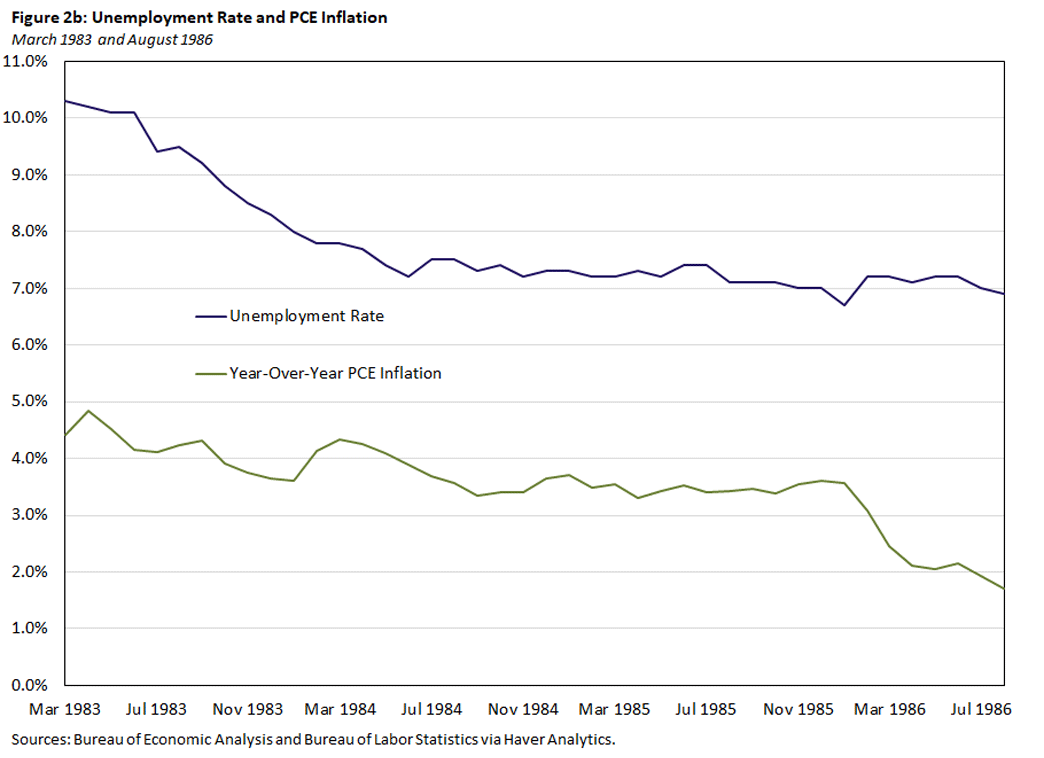

As seen in Figure 2b, both inflation and unemployment came down as the FOMC continued raising rates through August 1984. At the end of the rate cycle in August 1986, inflation was below 2 percent, and the unemployment rate had come down over 3 percentage points to 6.9 percent.

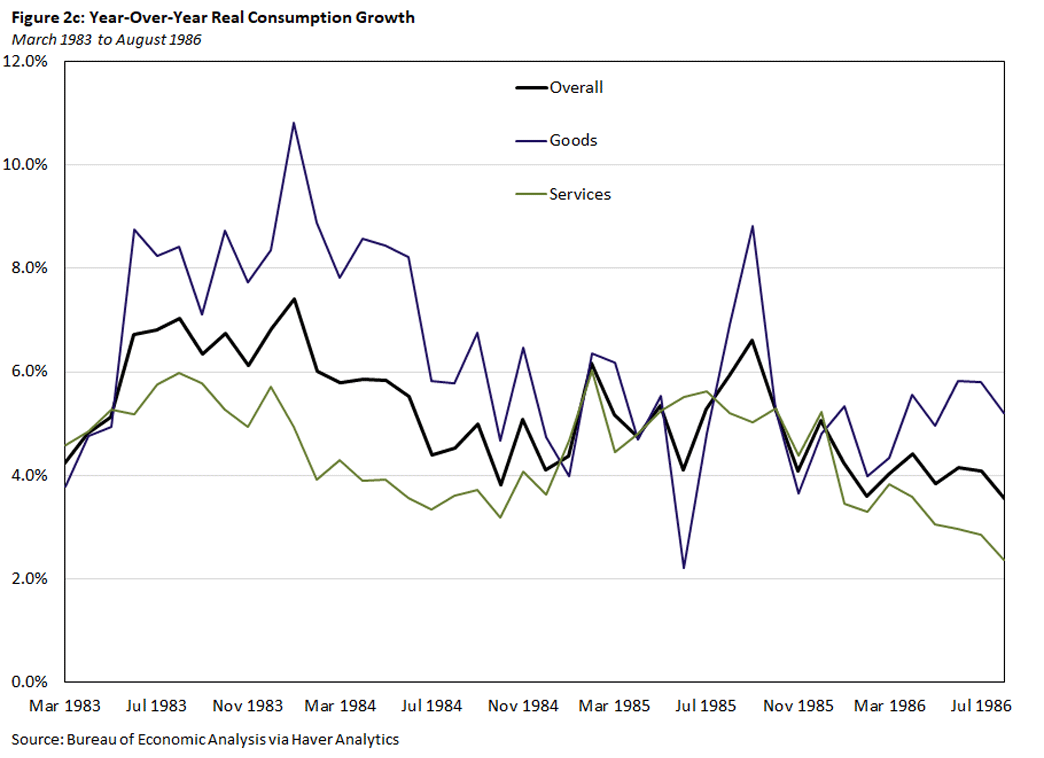

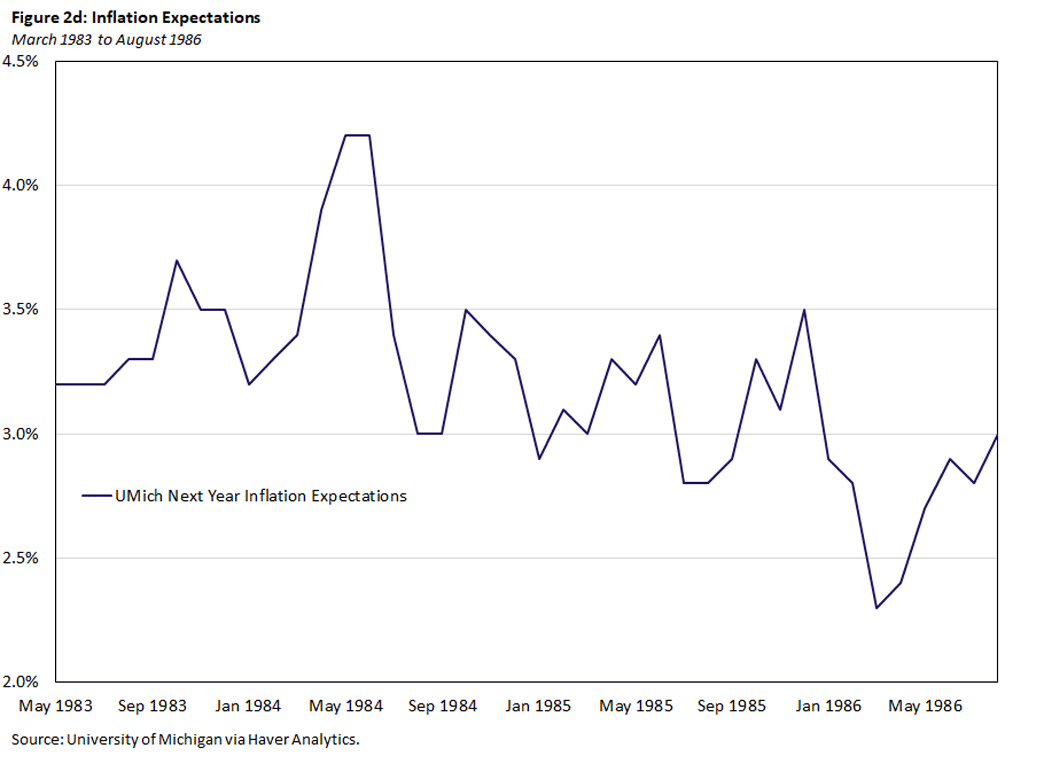

Additionally, consumption growth remained strong, and inflation expectations remained relatively flat around 3 percent, as seen in Figures 2c and 2d, respectively.

By the end of the rate cycle in August 1986, therefore, it seemed that the Fed had achieved a soft landing. The Fed attained its goal of low and steady inflation without a blow to consumption or a drastic rise in the unemployment rate, despite a total increase of 300 basis points in the federal funds target rate.

This apparent soft landing, however, turned out to be fragile: Less than six months later, inflation was rising once again, prompting the FOMC into a new round of rate hikes. What seemed like a soft landing in August 1986 was morphing into an aborted landing a couple of months later.

A Series of Shocks

A series of shocks combined with unprecedented fiscal policies in the mid-to-late 1980s coincided with a rise in inflation and the beginning of a new rate cycle in January 1987. High inflation and interest rates in the late 1970s were associated with financial turmoil for savings and loan institutions, which relied heavily on deposits with short-term maturities. Insolvent institutions were then permitted to remain open and appear solvent on paper due the number of failures and corresponding high costs to pay off insured depositors. The reduction in supervision and examination of savings and loan industries was followed by a period of growth in S&L assets during the period 1982-1985, as previously insolvent institutions took on more risks to try to attract additional business.2

Also, during this time, the Tax Reform Act of 1986 was signed into law. It lowered both the ordinary top tax rate and the corporate tax rate. This was the largest tax reform in four decades, and it laid the groundwork for a booming economy. The decrease in progressivity contributed an increase of an estimated permanent 0.12 to 0.34 percentage points in U.S. per capita GDP growth.3

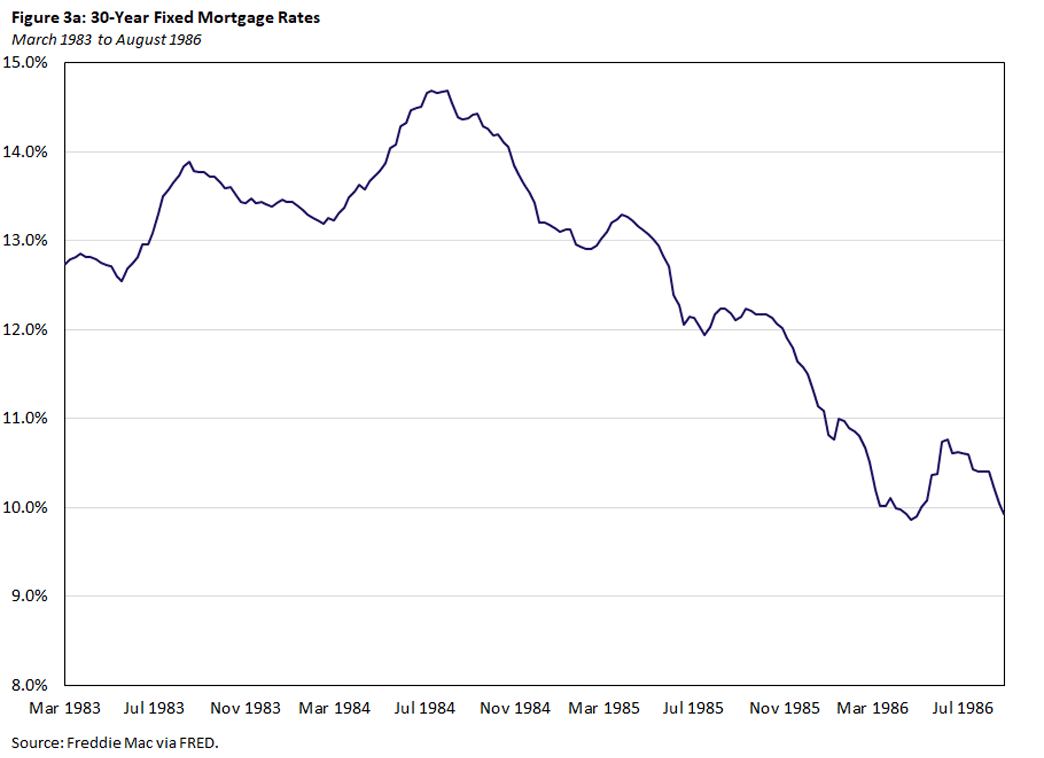

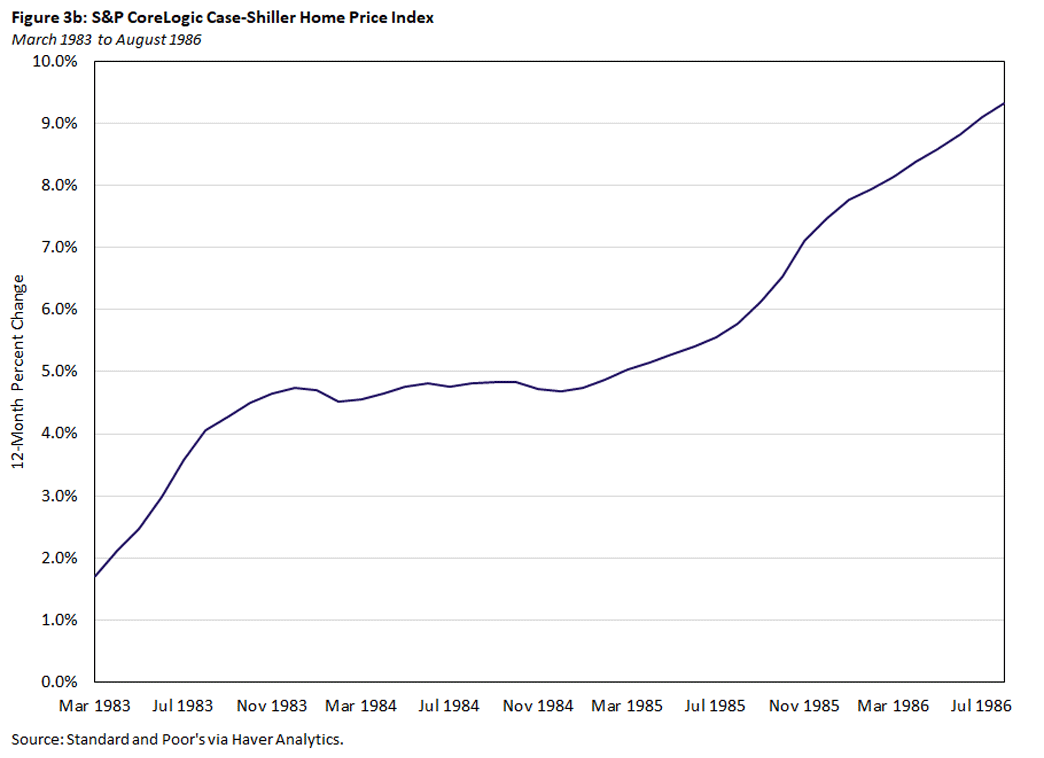

Additionally, in 1983 and the first half of 1984, mortgage rates rose to over 14.5 percent before falling sharply as the FOMC lowered rates beginning in August 1984. Meanwhile, the U.S. experienced what in hindsight came to be largely viewed as a housing bubble, with home prices rising over the entire March 1983-August 1986 rate cycle.4 Figure 3a charts average 30-year fixed mortgage rates over the rate cycle, and Figure 3b shows the 12-month percent change for the S&P CoreLogic Case-Shiller Home Price Index over the same period.

Rate Cycle: January 1987 to September 1992

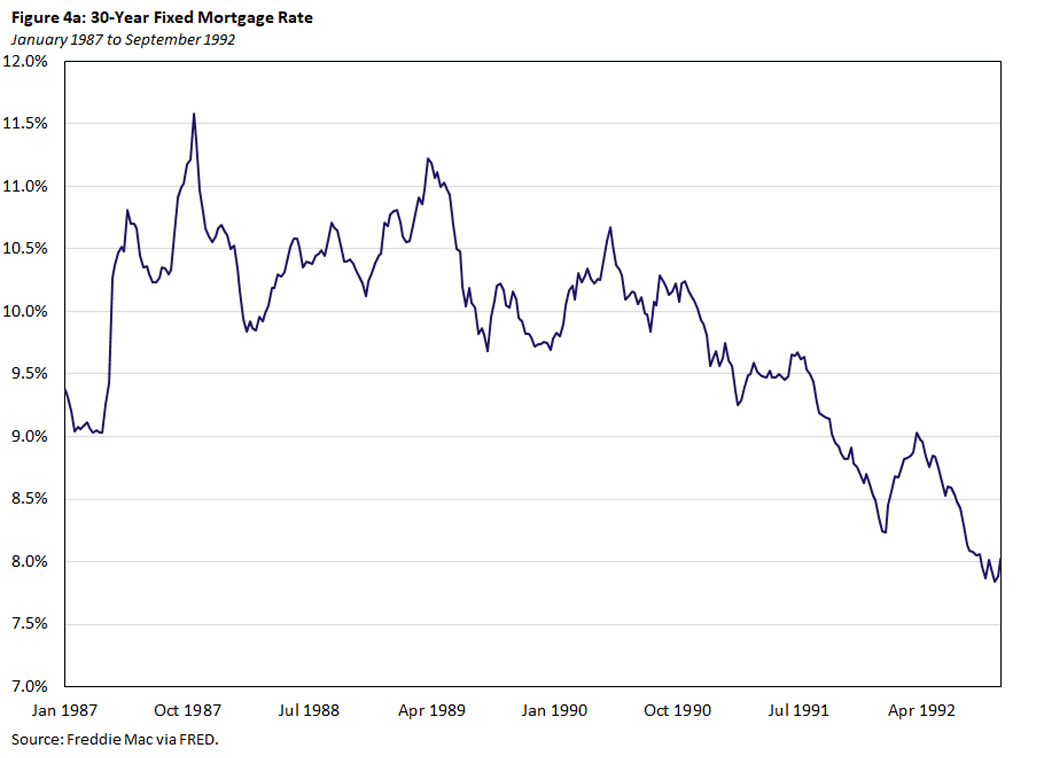

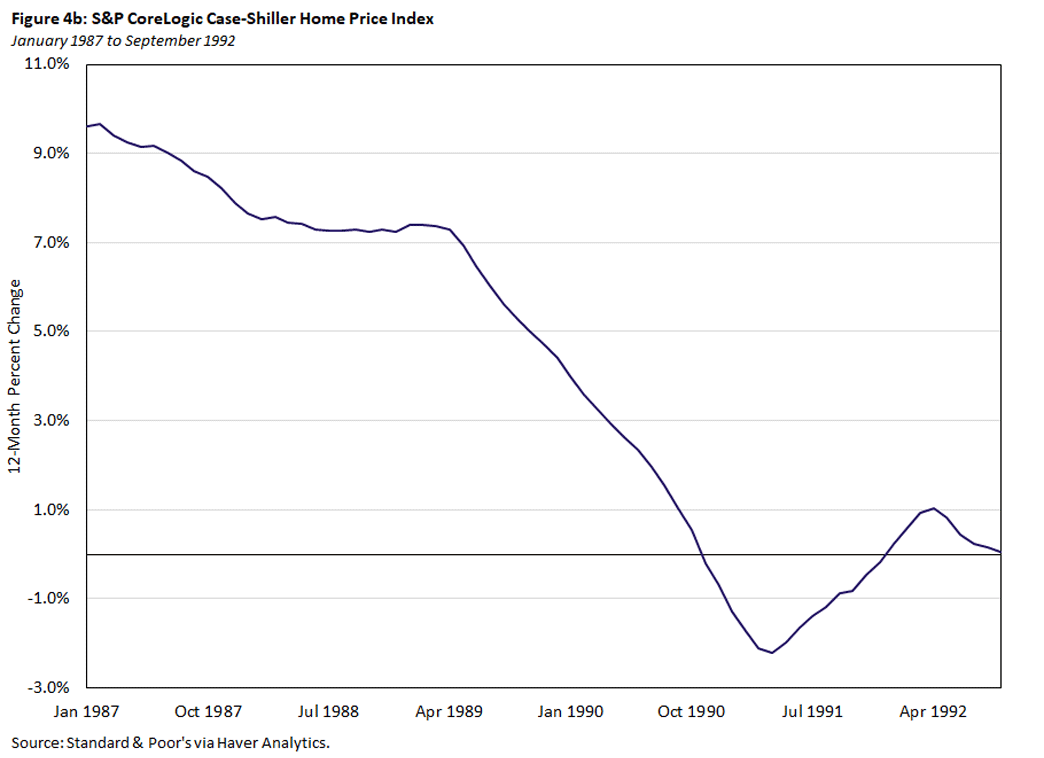

This housing bubble did not last long, as housing price inflation was already coming down sharply by January 1987. Figure 4a plots the change in average 30-year fixed mortgage rates during the January 1987-September 1992 rate cycle, and Figure 4b shows the 12-month percent change for the S&P CoreLogic Case-Shiller Home Price Index over the same period.

Compared to the previous cycle, the increase in the average 30-year fixed mortgage rate in 1987 and 1988 was modest, with a change of less than 1.5 percentage points between January 1987 and the peak of the rate cycle in June 1989. After June 1989, the mortgage average and 12-month percent change in home prices both fell considerably. Even more notably, the 12-month percent change in home prices fell below 0 percent in 1991, indicating negative growth in home prices.

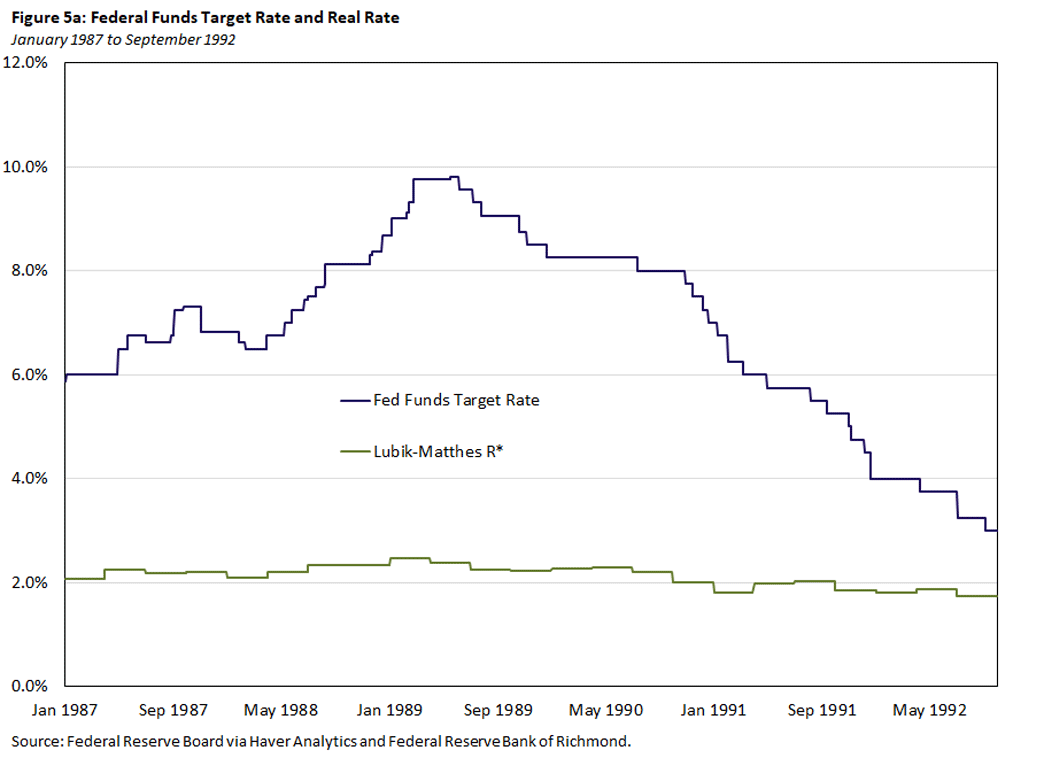

Against the backdrop of a booming U.S. economy and inflation rising again in the mid-1980s (in part reflecting rapidly increasing housing prices), the FOMC raised rates in January 1987 after holding them steady since August 1986. Figure 5a charts the fed funds target rate and Lubik-Matthes r* over the entire January 1987-September 1992 rate cycle. In the beginning of January 1987, the fed funds target rate was 5.875 percent and later reached its peak of 9.8125 percent in June 1989.

While inflation started around 1.5 percent in January 1987, it quickly increased and reached 4.7 percent in June 1989. As monetary policy tightened, inflation began to decline after 1989, and the housing bubble began to deflate. The savings and loan crisis described in the previous section came to a head in the latter half of the 1980s: By 1989, hundreds of insolvent S&Ls had billions of dollars in assets and needed to be resolved.

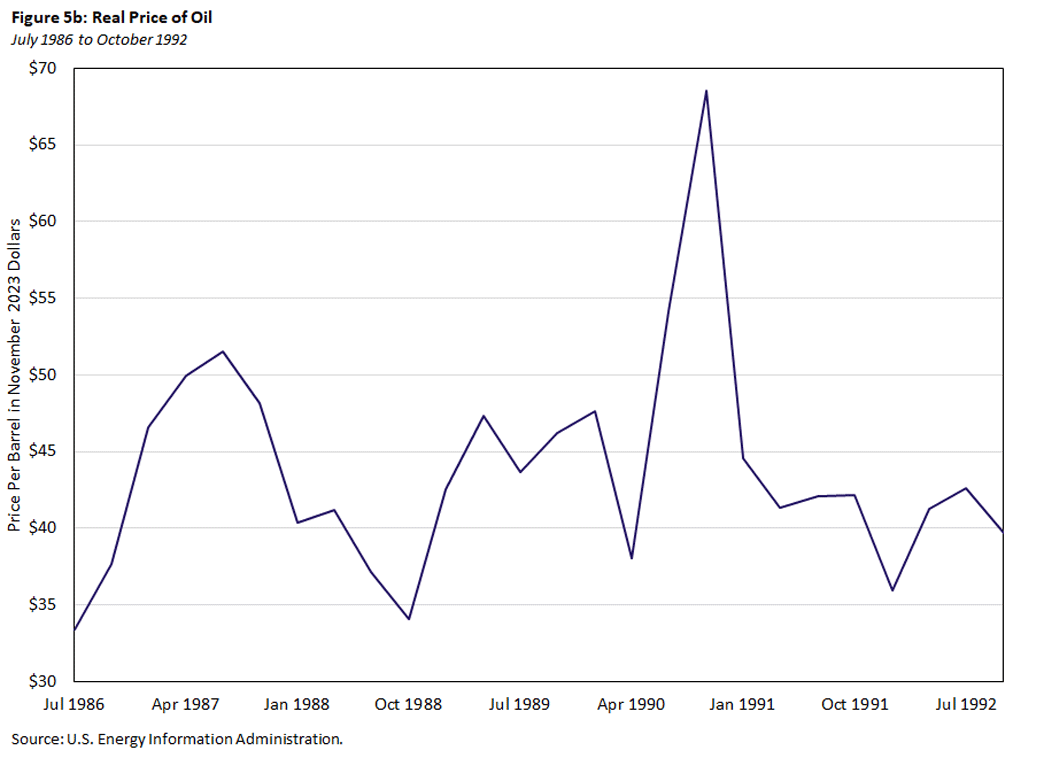

Also, Iraq invaded Kuwait (a small, oil-rich country in the Persian Gulf) in the summer of 1990. This invasion led to a shock to oil prices and resulted in the U.S.'s involvement in the Gulf War. Figure 5b charts the real price of oil in November 2023 dollars. We can see a substantial jump in the real price of oil, with the price per barrel increasing over $30 between April and October 1990. The effect of these events contributed to a U.S. recession from July 1990 to March 1991.

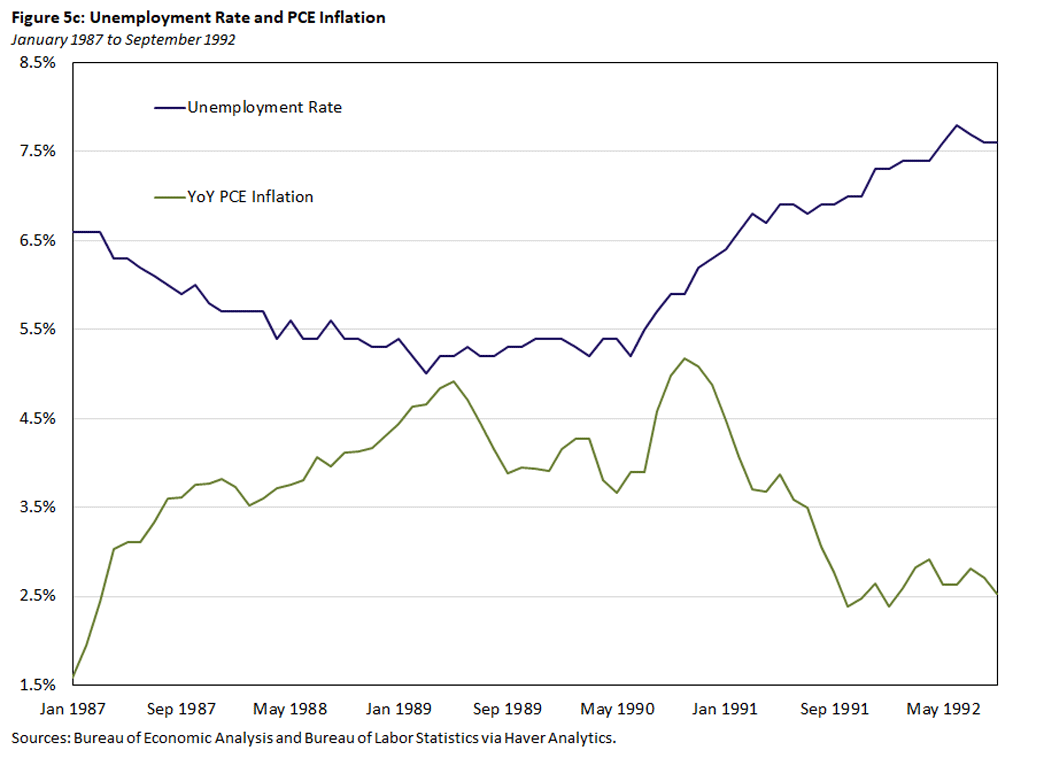

U.S. inflation rose sharply as the Gulf War began and the oil price shock hit. However, by 1991, inflation was falling again as the effects of the recession beginning in the summer of 1990 took effect. The unemployment rate picked back up during this recessionary period after gradually falling earlier in the rate cycle. Figure 5c plots the change in the unemployment rate and inflation rate over the entire rate cycle.

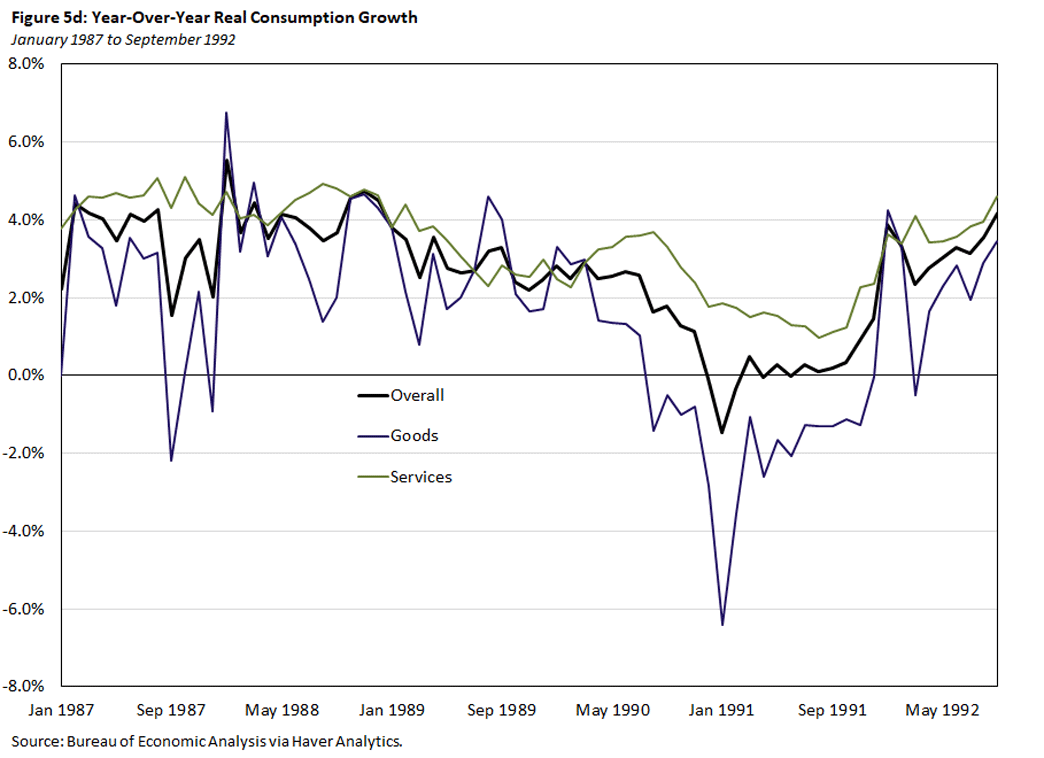

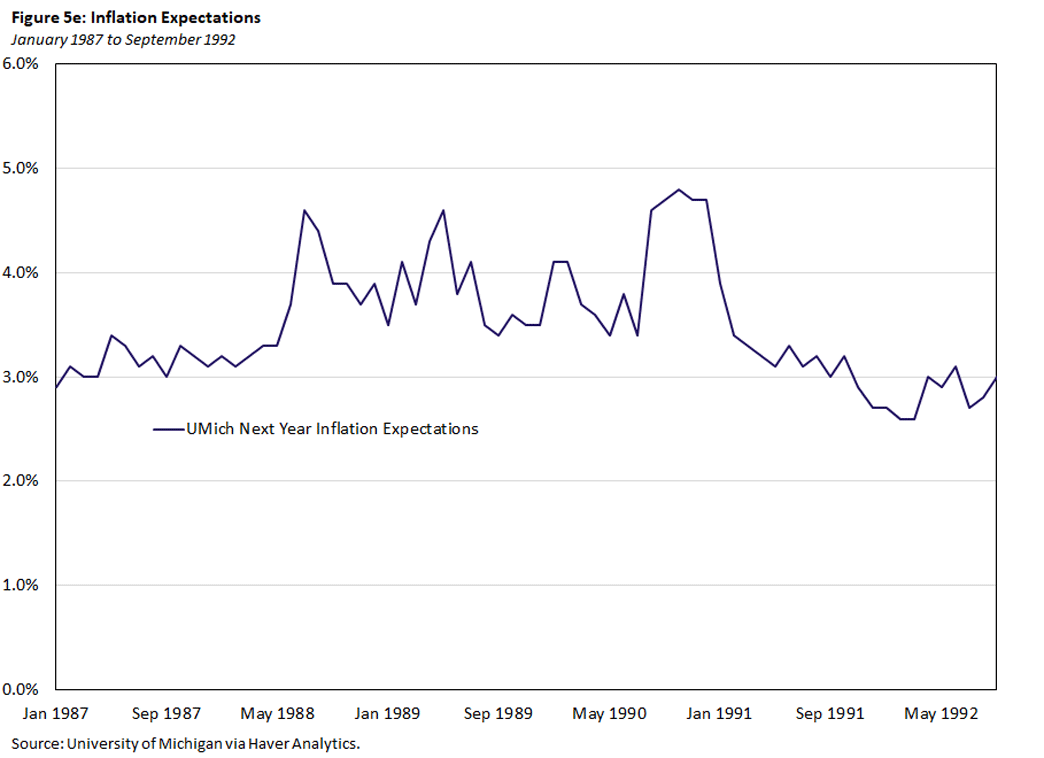

Similarly, in Figures 5d and 5e, we see a notable fall in consumption growth and a jump in inflation expectations, respectively, in late 1990 and early 1991 after remaining relatively constant.

The end of the rate cycle we just described may today be interpreted as a hard landing, or at least harder than one might have wished. In the FOMC's pursuit of achieving low and stable inflation as a recessionary shock hit, unemployment significantly increased, and consumption growth fell. It is important to recognize that a correction in housing prices had also been taking place along with an unfolding savings and loan crisis. Furthermore, the oil price shock from Iraq's invasion of Kuwait and the resulting Gulf War could not easily have been predicted and, therefore, been prepared for.

Conclusion

In the beginning of the current rate cycle, policy decisions by the FOMC seemed evident. In March 2022, inflation was running at several times its target, and more restrictive policy was needed to try to bring the level of inflation down. Now, the state of the economy is more nuanced. It will be especially important, therefore, to monitor not only inflation's progress in the next couple of months but also the emergence of other economic shocks that can materialize and affect unemployment and consumption growth.

One of the lessons drawn from the 1983 and 1987 rate cycles is that policy does not happen in a vacuum, as the economy is constantly buffeted by outside shocks. One needs to be mindful of how many and what types of shocks hit the economy in the coming year. Soft landings can be fragile, and hard landings have often been the norm over the U.S. post-war period.

Pierre-Daniel Sarte is a senior advisor, and Erin Henry and Jack Taylor are research associates in the Research Department of the Federal Reserve Bank of Richmond.

1

For additional information on the calculation of Lubik and Matthes' r*, see "Calculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches" and "The Stars Our Destination: An Update for Our R* Model."

2

References for information on the savings and loan crisis can be found in the Federal Reserve History's Savings and Loan Crisis, chapter 4 of the Federal Deposit Insurance Corp.'s History of the Eighties - Volume 1 and the FDIC's publication "The S&L Crisis: A Chrono-Bibliography."

3

Estimates can be found in my (Pierre's) 2004 paper "Progressive Taxation and Long-Run Growth," co-authored with Wenli Li.

4

Karl E. Case and Robert J. Shiller discuss the 1980s housing bubble in their paper "Is There a Bubble in the Housing Market? (PDF)"

To cite this Economic Brief, please use the following format: Henry, Erin; Sarte, Pierre-Daniel; and Taylor, Jack. (January 2024) "Of Soft, Hard and Aborted Landings." Federal Reserve Bank of Richmond Economic Brief, No. 24-02.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us