Stargazing: Estimating r* in Other Countries

Economic Brief

March 2024, No. 24-10

We provide estimates of r* — a central concept in monetary policy — for a set of countries using the same methodology as for the Richmond Fed's own r* estimate for the U.S. We generally find that the estimated r* paths are country specific, but that they behave more similarly to each other than to the U.S., indicating its central role in the international monetary system.

The concept of the natural real rate of interest (denoted r*) has gained considerable attention of late, as it is a key element in informing monetary policy decisions. It represents the equilibrium level of the real interest rate (computed as the nominal policy rate less a measure of inflation) when the economy is at its long-run trend level of growth, inflation is at the Federal Reserve's target, and there are no excess supply or demand pressures. Policymakers can use this rate as a metric for gauging how expansionary or contractionary policy is or should be. However, an important caveat of r* is that it is unobserved and thus must be inferred from actual data by use of theoretical or empirical models. One of the authors of this article (Thomas) has developed an empirical model of r* together with Christian Matthes of Indiana University, and estimates of the Lubik-Matthes r* are reported quarterly.1

In this article, we report on our efforts to extend these estimates to other countries, examining Canada, the eurozone and the U.K. We select this set of countries for a variety of reasons: data availability, industrialized economies, independent monetary policy and close economic connection with the U.S.2 Overall, we find that there are some differences in r* estimates between countries, but the pattern of r* paths are more alike to each other than they are to the U.S.

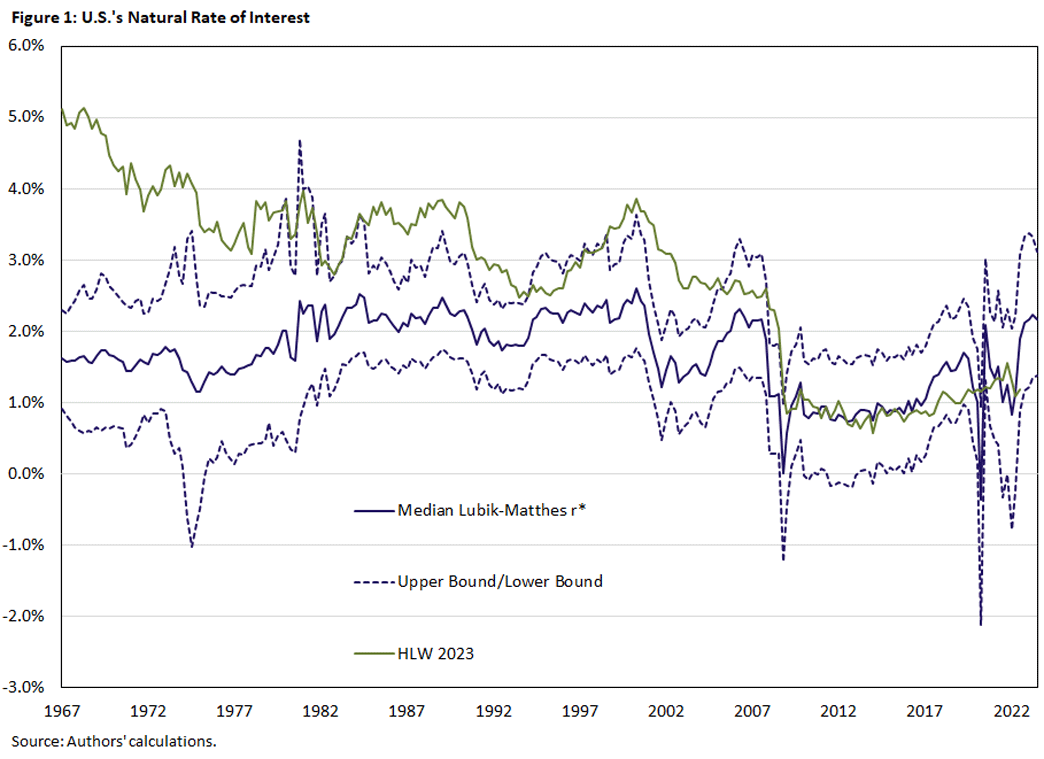

The U.S.: the Guiding r*

Figure 1 shows the most recent r* estimate for the U.S. (as of December 2023), with a current value of 2.2 percent. According to this estimate, the natural real rate was between 1 percent and 2 percent from the beginning of the sample in 1967 until 1980, after which it rose above 2 percent and remained at this level until the early 2000s.

With the onset of the Great Recession in the U.S., r* fell toward 1 percent and remained at that level even during the zero-interest policy period of the 2010s. The pandemic induced some volatility in the estimates, but with the subsequent recovery r* has been rising steadily to its current level. What we do not necessarily observe in these estimates is a pattern we'll see in other countries' estimates, namely a seemingly secular decline toward values close to zero.

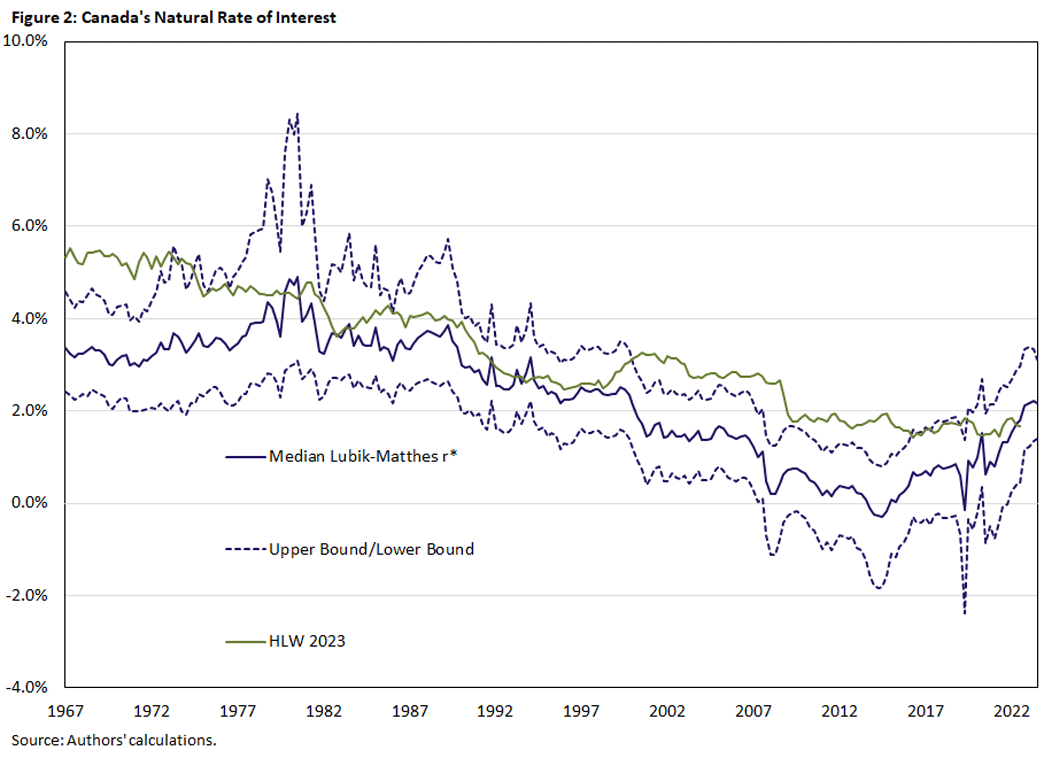

Canada: the North r*

Our estimate of Canada's r* is reported in Figure 2. The sample period is the same as for the U.S.: from the first quarter of 1967 through the third quarter of 2023. We chose the same baseline specification as for the U.S. estimate, which limits the extent to which the coefficients of the model are allowed to vary as compared to the original Lubik-Matthes model. This tends to result in a smoother, less variable r* path and allows for direct comparison with the U.S.

We find that Canada's r* was in a 3-3.5 percent range for the first 20 years of the sample (except for a short uptick above 4 percent in the late 1970s to early 1980s). In the late 1980s, r* started a secular decline until the mid-2010s. It reached a low point of -0.3 percent in the third quarter of 2014, after which r* rose steadily to its current estimate of 2.2 percent.

In comparison with the U.S., Canada's natural rate was a full 2 percentage points higher in the first part of the sample and fell to lower levels in the wake of the global financial crisis (GFC). Moreover, the steady overall decline in rate levels is more pronounced in Canada than in the U.S., which exhibits more of a level shift.

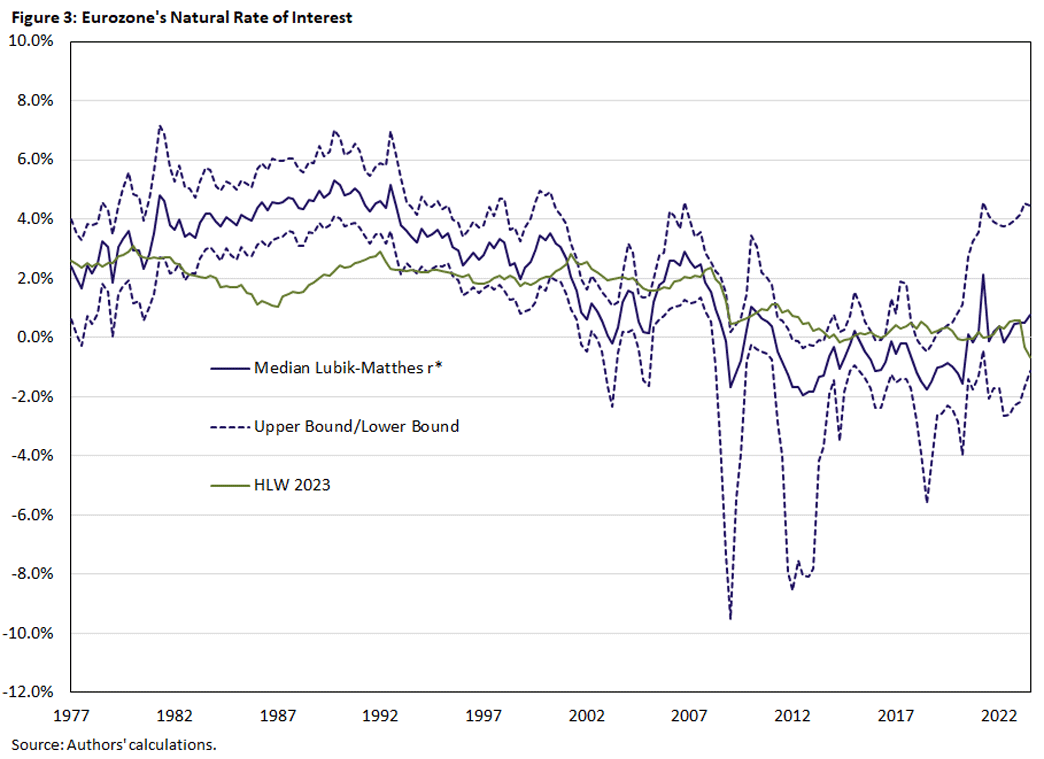

The Eurozone Constellation

We now turn to the eurozone r* estimate, which is reported in Figure 3. The sample starts in the first quarter of 1977, and it covers all countries that have currently adopted the euro and are thus subject to the European Central Bank's monetary policy decisions. To provide a longer time series for the respective aggregates, the sample has been artificially extended to pre-euro periods.

These estimates appear more volatile than the corresponding estimates for the U.S. and Canada. In addition, the second half of the sample (from the creation of the euro in 2001 to the present) is more volatile than the synthetic sample period before. Since the start of the euro, r* has been consistently below 2 percent (with a short exception in the mid-2000s), which is broadly in line with the experience of other leading economies. As a very open economy, the eurozone is very open to capital flows and thus exposed to arguably the leading driver of international real rates, namely the global savings glut. It also supports the idea that the euro was quickly adopted as an international reserve currency and that eurozone debt was considered a safe asset.

Since the 2010s, eurozone r* has been consistently negative, even close to -2 percent in 2012. In the pre-euro period, r* rose at first in a steady manner from around 2 percent to nearly 5 percent in the late 1980s. Commensurate with a generally observed decline in real rates, the 1990s show our estimated r* gradually falling to zero.

The sample period has witnessed several economic crises in Europe. However, they seem visible only in the euro period. Europe was buffeted by the same shocks in the 1970s as other industrialized countries and had similar high-inflation episodes as the U.S.

Throughout the 1980s, r* remained high, the flip side of which is high actual real rates and high policy rates. Arguably, it was the Deutsche Bundesbank's restrictive policy stance that eventually drove inflation out of Europe. At the same time, the crisis of the European Exchange Rate Mechanism (a precursor to the introduction of the euro) is not noticeable in the early 1990s, except that it appears to be the starting point for a decline in r*.

Eurozone r* turned decidedly negative at the onset of the GFC and the European debt crisis that centered on Greece. When the ECB most definitively addressed the crisis, our estimated r* hit -2 percent, presumably due to the negative policy rate that the ECB implemented during this time.

The level of r* indicates, however, that even negative policy rates would still have been restrictive or at best neutral. This observation is consistent with a view that the European policy responses to the GFC were too timid, especially in comparison with the U.S. As a case in point, the real rate gap in the U.S. was largely negative during the 2010s as the Fed pursued a policy of lower for longer. It is only in the aftermath of the pandemic that r* has turned decidedly positive.

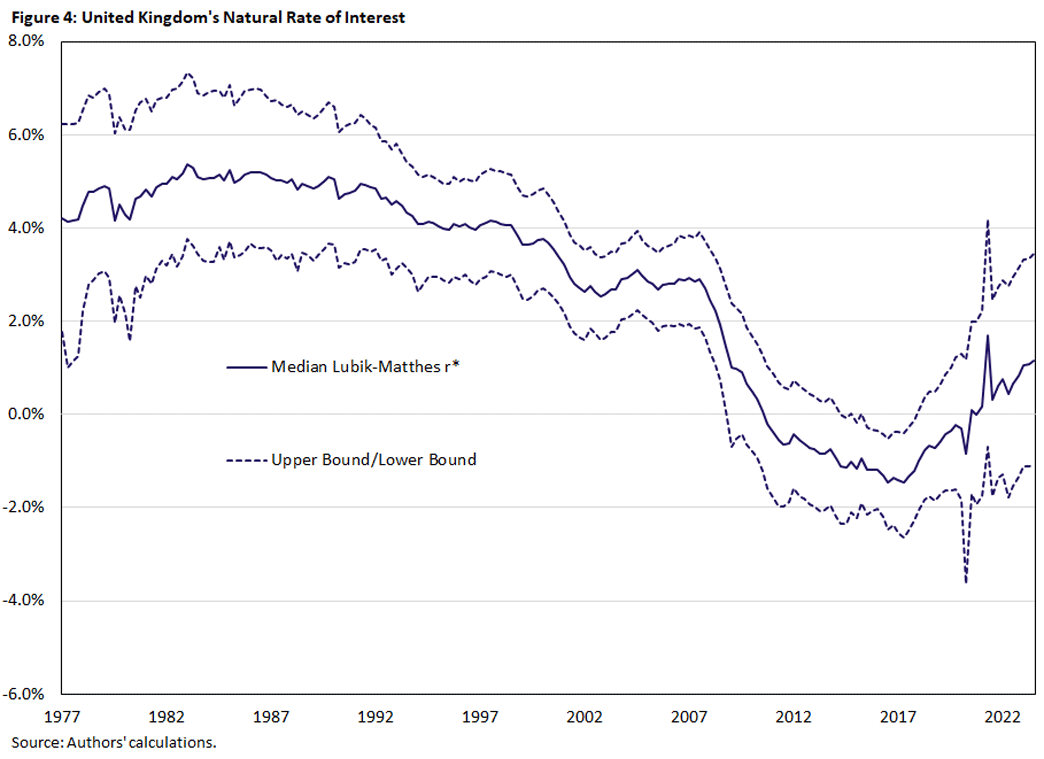

The U.K.: a Shooting r*

Finally, we also examine r* in the U.K., which is shown in Figure 4. The start of the sample coincides with that for the eurozone. It is noteworthy that our estimated path appears smoother than for the other countries under consideration. Similar to Canada, we can identify several episodes. First, r* remained in a 4-5 percent range until starting to decline in the early 1990s. From 2001 until the onset of the GFC, r* remained stable at close to 3 percent before falling precipitously into negative territory. Its path turned around in 2017 and rose steadily to its current level of 1.1 percent.

These episodes can plausibly be tied to other events shaping the economy. As is the case for the other countries, we see the secular decline in interest rates starting in the late 1980s. The Bank of England received operational independence in 1997, which was followed by the period of stable r* estimates in the 2000s. The GFC had, again, a dramatic impact, leading to negative interest rate policies.

Shortly after the Brexit referendum, r* started rising, although this is also coincident with an end of the accommodative policy stance by the Bank of England. It may be tempting to draw a connection with expectations of higher growth after Brexit, which did not materialize. Other drivers of a higher real rate — such as reduced savings and higher investment demand — are also not quite identified in the data, leaving the conclusion that it perhaps reflects global r* increases.

A Comparison With Other Estimates

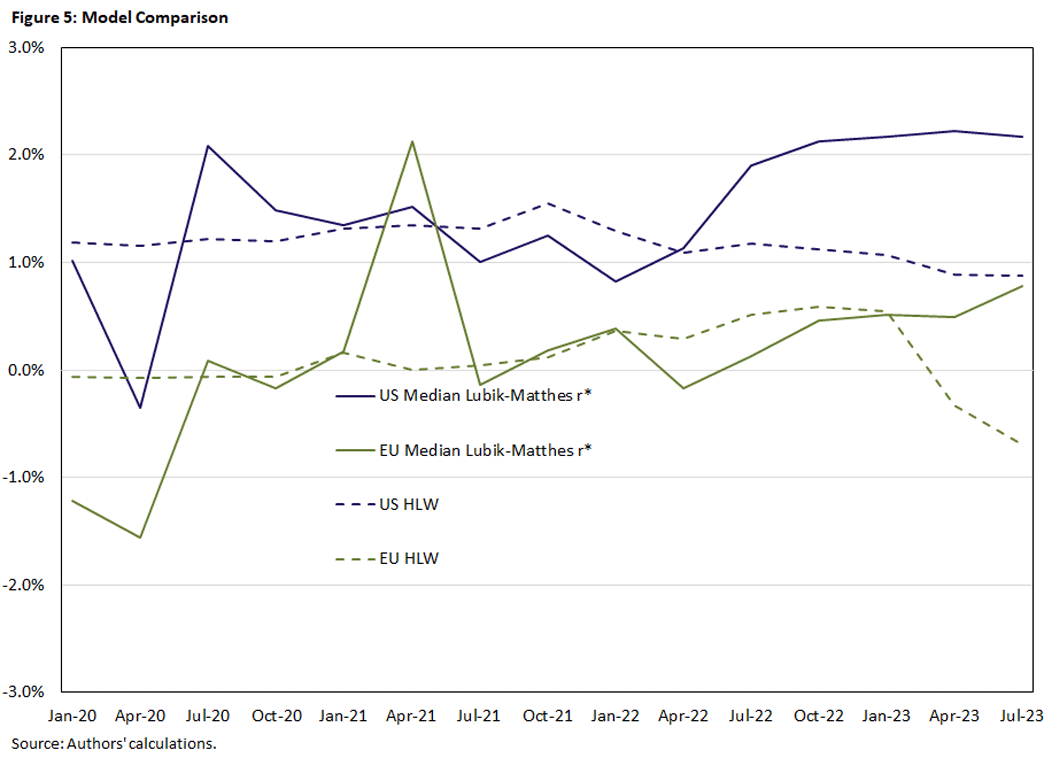

The New York Fed provides r* estimates for Canada and the eurozone. These are based on the Holston-Laubach-Williams (HLW) model that also underpins the main natural rate estimates for the U.S. There are some marked differences between their estimates and our estimates.

The HLW estimates are broadly less volatile and less reactive to recent data, except for perhaps Canada. For example, during the GFC, HLW estimates a decline in r* of 1.9 percentage points in the eurozone (1.5 percentage points in the U.S.) from January 2008 until January 2009, whereas we estimate a decline of 4.1 percentage points (1.6 percentage points in the U.S.) that started in July 2007.

This volatility may be a factor in the recent divergence between HLW and Lubik-Matthes r* estimates in the U.S., which we observe also occurs in the eurozone. Figure 5 shows our median estimate compared to HLW since the pandemic. Except for the second quarter of 2021, the estimates track each other quite closely in both regions but have recently diverged as recent data point toward a recovery from the high inflationary period.

Table 1 summarizes the most recent r* estimates for these countries. Notably, HLW is below any of our estimates, which suggests that the discrepancy could be due to methodological differences. This is also notable in the entire estimated r* path, as HLW has a more pronounced downward trend than ours.

| Q3:2023 | US | Canada | Eurozone | UK |

|---|---|---|---|---|

| Lubik-Matthes | 2.17 | 1.78 | 0.78 | 2.59 |

| Holston-Laubach-Williams | 0.88 | 1.34 | -0.69 |

Conclusion

This article expands on the set of Lubik-Matthes r* estimates that the Richmond Fed reports quarterly. We estimate natural real rates for Canada, the eurozone and the U.K., using the same methodology as employed for our benchmark U.S. model. We find that there are common features in these estimates:

- The secular decline in interest rates after the 1980s

- The impact of the GFC and subsequent zero or even negative interest rate policies in the 2010s

- The recent rise in r* following the pandemic

At the same time, country-specific factors are also at play: turning points that can be loosely associated with political events in the case of the U.K., and the very low and negative r* estimates in the case of the eurozone.

Perhaps the most striking observation is that these additional r* estimates appear much more aligned with each other than with the U.S. The secular decline in rates is much less visible in the latter, while there are fewer noticeable turning points.

A final caveat concerns the range of uncertainty within individual estimates and between alternative methodologies. A comparison with other prominent and publicly available country estimates shows quite different r* paths, which suggests that methodology matters in extracting such hidden stars from observable data.

Thomas Lubik is a senior advisor, and Brennan Merone and Nathan Robino are research associates, all in the Research Department at the Federal Reserve Bank of Richmond.

1

Previous articles that describe the model used for estimating r* include the 2015 paper "Time-Varying Parameter Vector Autoregressions: Specification, Estimation and an Application" and the 2015 article "Calculating the Natural Rate of Interest: A Comparison of Two Alternative Approaches." The model was updated recently, which is explained in detail in the 2023 article "The Stars Our Destination: An Update for Our R* Model."

2

Data for the U.S. were collected from the Federal Reserve Board and the Bureau of Economic Analysis. Data for Canada were collected from the Bank of Canada and the International Monetary Fund. Data for the eurozone were collected from the European Central Bank. Data for the U.K. were collected from the Bank of England, International Monetary Fund and Organization for Economic Cooperation and Development. Data for the HLW estimates were collected from the Federal Reserve Bank of New York.

To cite this Economic Brief, please use the following format: Lubik, Thomas; Merone, Brennan; and Robino, Nathan. (March 2024) "Stargazing: Estimating r* in Other Countries." Federal Reserve Bank of Richmond Economic Brief, No. 24-10.

This article may be photocopied or reprinted in its entirety. Please credit the authors, source, and the Federal Reserve Bank of Richmond and include the italicized statement below.

Views expressed in this article are those of the authors and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Subscribe to Economic Brief

Receive a notification when Economic Brief is posted online.

Contact Us