Elevated Margins in the PPI

Macro Minute

September 5, 2023

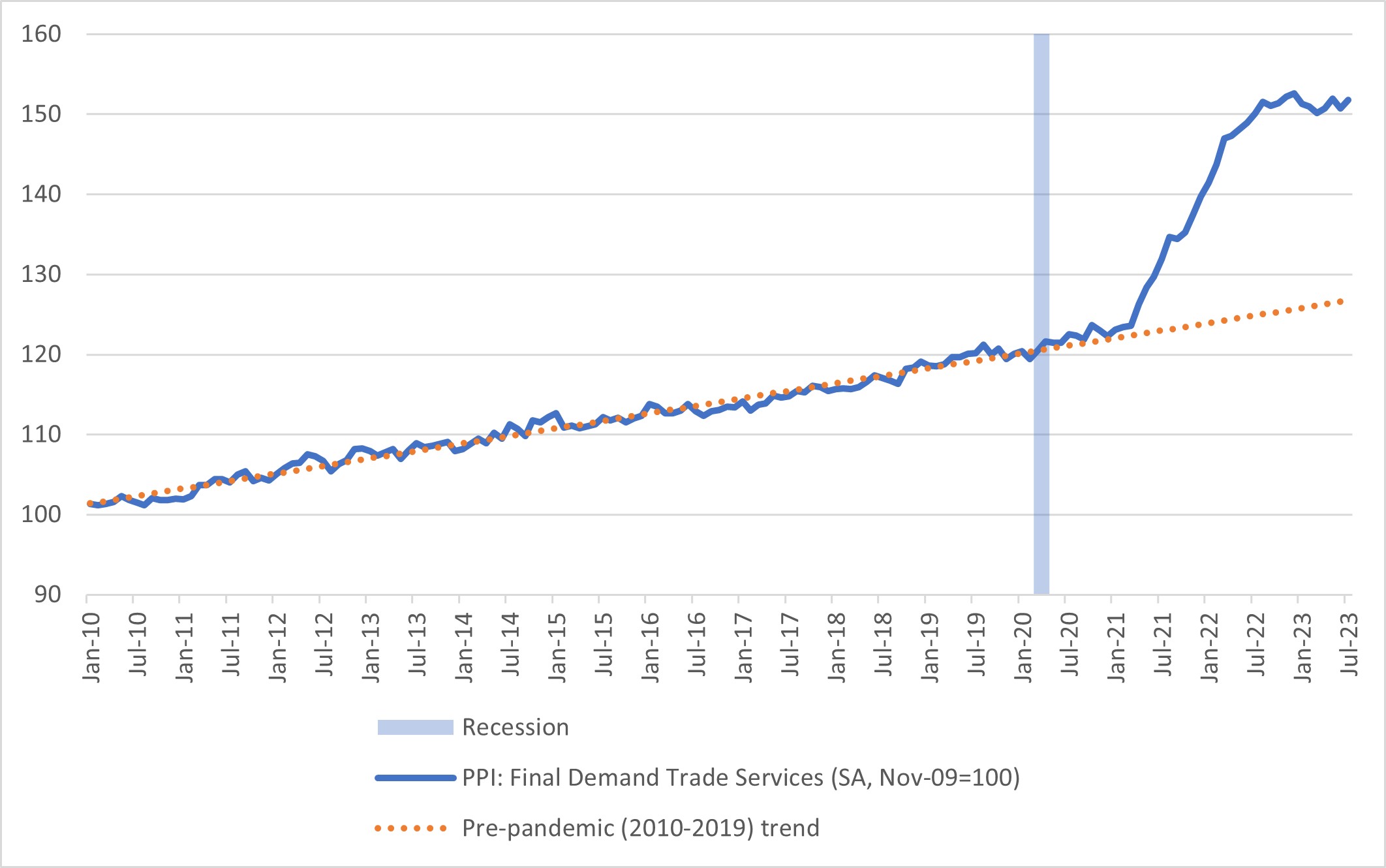

As discussed in a previous post, the producer price index (PPI) may hold clues for consumer price inflation. Out of the many components that make up the PPI, one particularly relevant item from the perspective of shoppers may be the PPI's trade indexes. These indexes measure changes in "margins" received by wholesalers and retailers, the businesses from whom most households directly purchase goods and services (i.e., rather than directly from manufacturers themselves). As explained below, these margins reflect the difference between a trader's purchasing cost of a good and the price that the trader charges the final buyer. Figure 1 below shows that this PPI for trade services — and, thus, wholesale and retail margins — remains elevated versus the pre-pandemic trend level.

What do these trade margin PPIs measure? Measuring the output of the trade sector is challenging, because it isn't directly observed: Wholesalers and retailers do little alteration or transformation of the goods they receive from producers. According to Bureau of Labor Statistics staff, the PPI's trade services index seeks to measure the sector's output through margin prices. These margin prices "track changes in prices received, less the acquisition price of goods sold by wholesalers and retails." (See Figure 2 below.)

When people (particularly those in commerce) hear the word "margin," their minds may quickly jump to "profits." But readers should note that the gap between current selling prices and current acquisition prices illustrated in Figure 2 may not fully flow to the bottom line of a traders' net income accounting. Some of the difference goes toward covering costs incurred by traders. Wholesalers incur costs for selling, promoting, buying, assortment building, bulk breaking, warehousing and transporting. Retailers may also incur costs for storing, marketing, shipping, handling and displaying products. The PPI's trade services price index could be elevated because of higher costs of performing these trade services.

Is there a better way to measure the actual profits of wholesalers and retailers? One possibility: The Bureau of Economic Analysis's quarterly GDP release includes data on nonfinancial corporate profits. We can look into one of the underlying sources of this series — the Census Bureau's Quarterly Financial Report (QFR) for Manufacturing, Mining and Trade Corporations — to see how it records the profits of wholesalers and retailers.

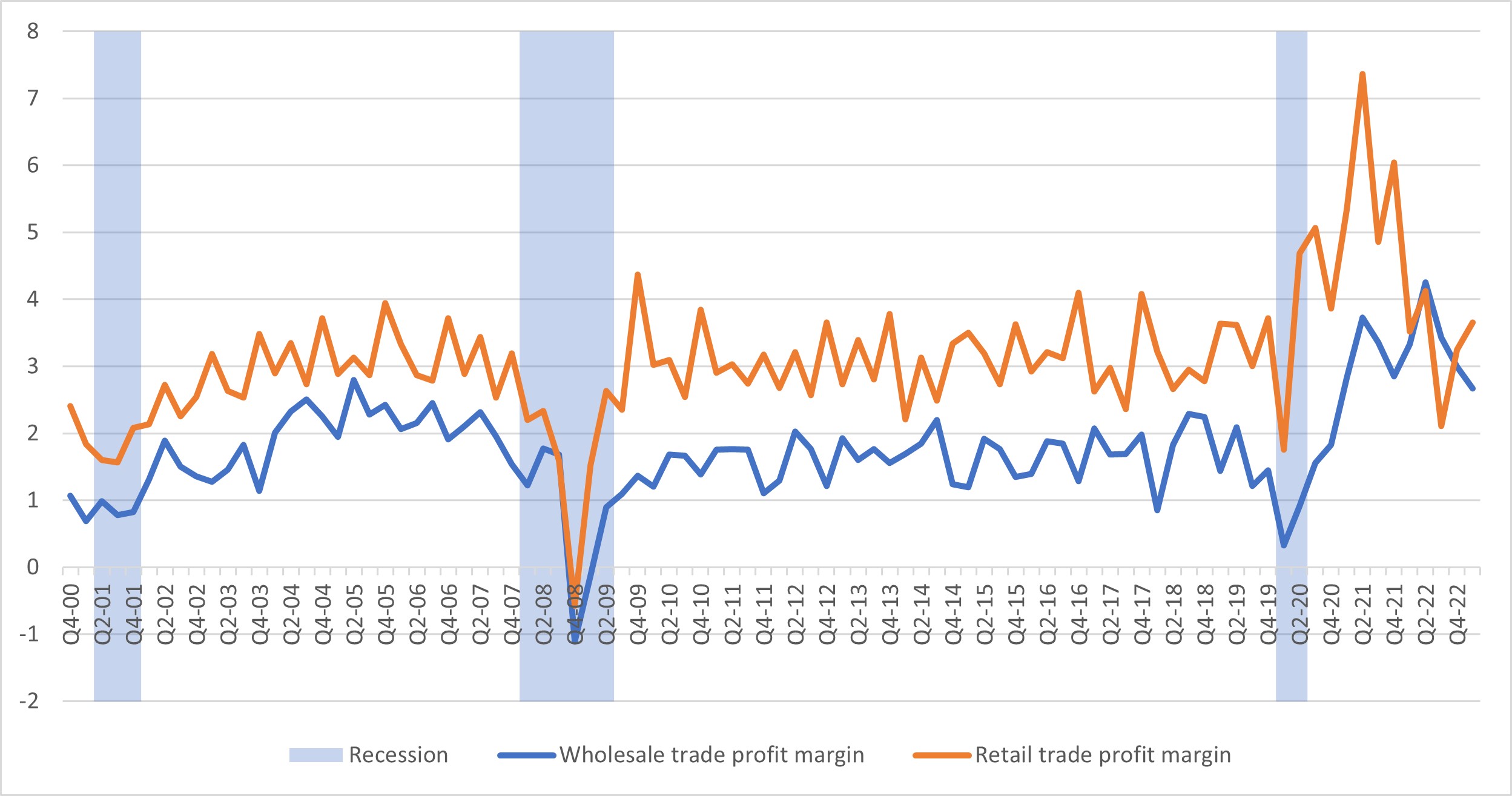

Figure 3 below plots an alternative "profit margin" — defined as after-tax profits as a percentage of sales as defined by the QFR — for the wholesale and retail trade sectors. As of the first quarter of 2023, profit margins for wholesalers averaged 2.7 percent, down from a peak of 4.3 percent in the second quarter of 2022 but still elevated versus the 1.4 percent profit margin observed before the pandemic (the fourth quarter of 2019). For retailers, profits margins were 3.7 percent as of the first quarter, down from a peak of 7.4 percent in the second quarter of 2021 and equal to the pre-pandemic profit margin in the fourth quarter of 2019.

Interestingly, profit margins as depicted in Figure 3 rose alongside inflation in 2021-2022, which some have taken as a symptom of "greedflation," where inflation is driven higher in part because businesses are excessively charging higher prices simply to attempt to garner higher profits. However, despite profit margins being used to measure "profits" for GDP accounting, even this measure may not fully account for the costs incurred by businesses in the wholesale and retail trade sectors. (In particular, this measure may not reflect the costs of capital incurred by these businesses.) These measurement issues and their solution — along with an assessment of greedflation — will be the focus of an upcoming Richmond Fed Economic Brief by Andreas Hornstein. Readers should stay tuned for his insights!

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us