Is the Goods-to-Services Rotation Over?

Macro Minute

November 7, 2023

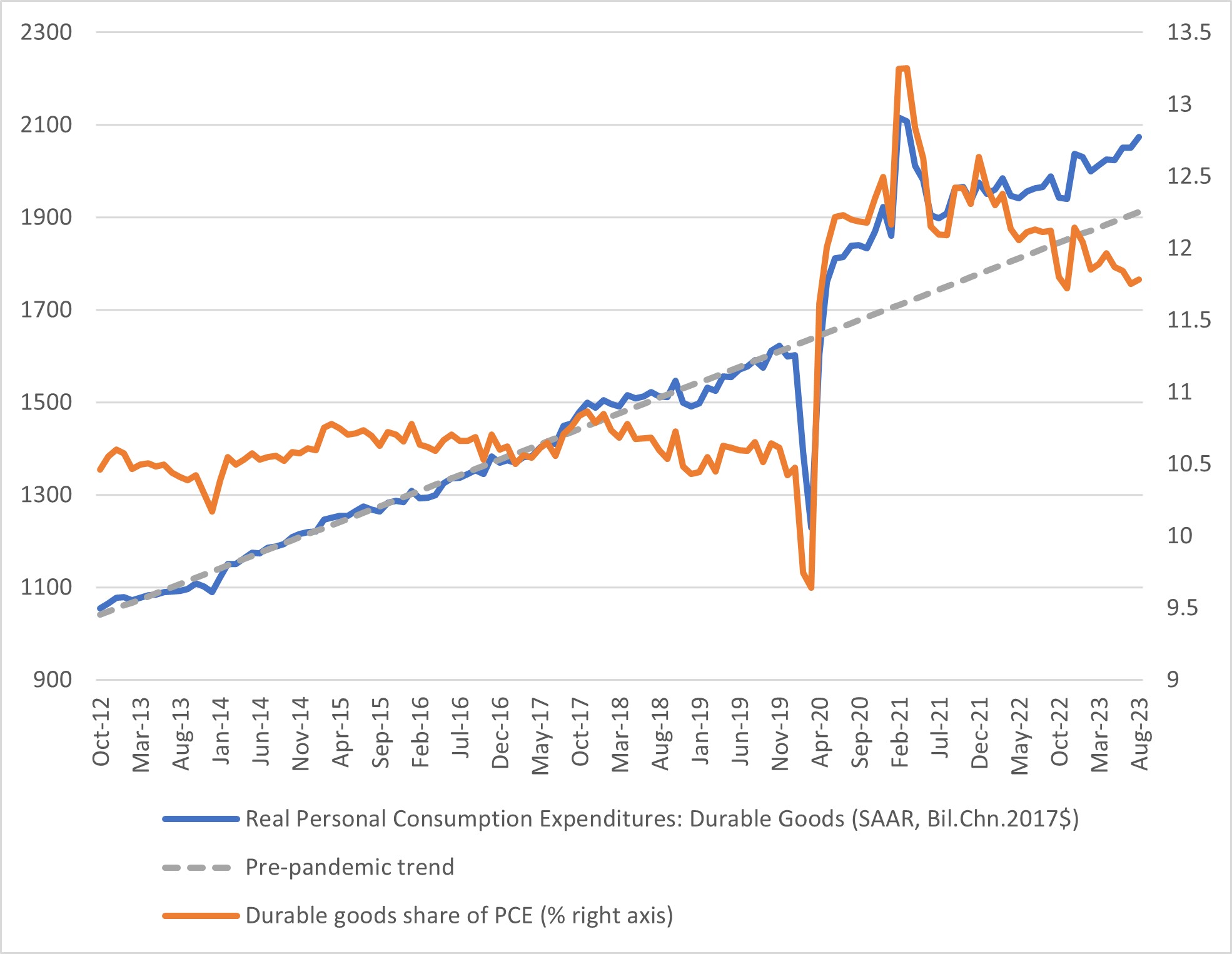

Consumers continue to spend robustly on durable goods: In September, real durable goods consumption rose 1.1 percent monthly and was 5.5 percent higher on a year-over-year basis. As shown in Figure 1 below, the level of real durable goods consumption remains higher than its pre-pandemic (2014-2019) trend, while the share of durable goods spending in overall personal consumption expenditures (PCE) remains more than 1 percentage point higher than its pre-pandemic share. Is it possible durable goods spending will settle above the pre-pandemic trend line? If so, what might this consumption shift mean for the aggregate economy?

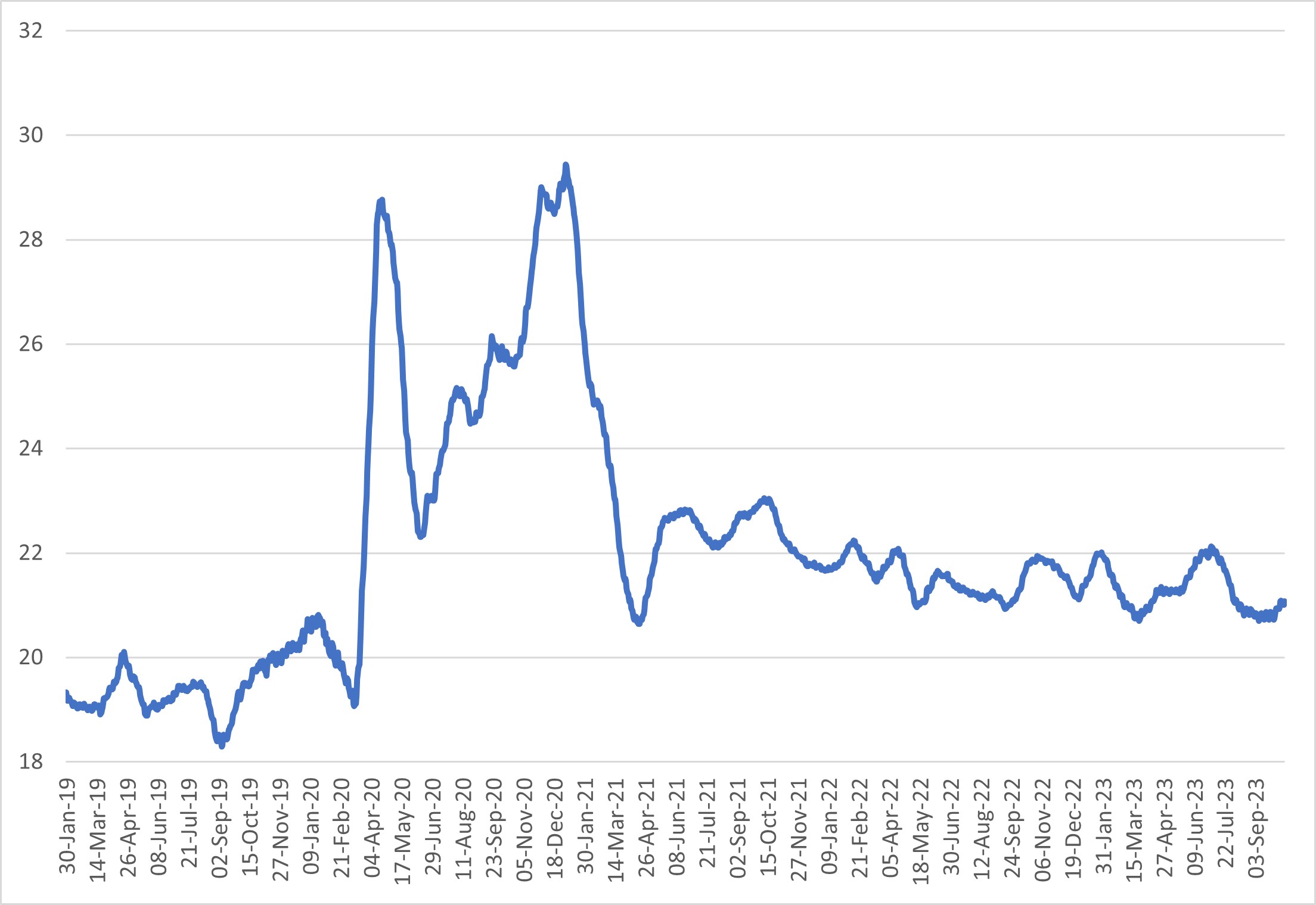

One reason consumer preferences may have shifted toward durable goods is that the pandemic may have induced long-lasting changes to people's lifestyles. Data collected from millions of mobile devices and published by the Bureau of Transportation Statistics suggests that the share of the population staying at home rose tremendously during the pandemic shock and has since settled to levels that remain above 2019 levels. (See Figure 2 below.)

Other data — such as the Back To Work Barometer produced by Kastle Systems, which tracks return-to-office rates via employee keycard and fob building access swipes — also appear to suggest that office occupancy has flatlined since the summer of 2022. With more people staying at home, consumers may have substituted durable goods consumption for outside-of-home services consumption.

If today's levels of durable goods consumption reflect a new higher trend, then perhaps we can return to using weakness in durable goods spending as a predictor of the future state of the economy. In a previous post ("What Are Leading Indicators Telling Us About Economic Growth?"), we discussed the Duncan Leading Indicator (DLI), which is the ratio of real durable goods spending and fixed investment to real final demand. Historically, this index has been able to flag recessions four quarters ahead. However, this relationship was challenged in 2021: A drop in real durable goods spending that year reflected normalization from a post-recession durable goods consumption surge from 2020 through early 2021, rather than weakness in consumer and business sentiment.

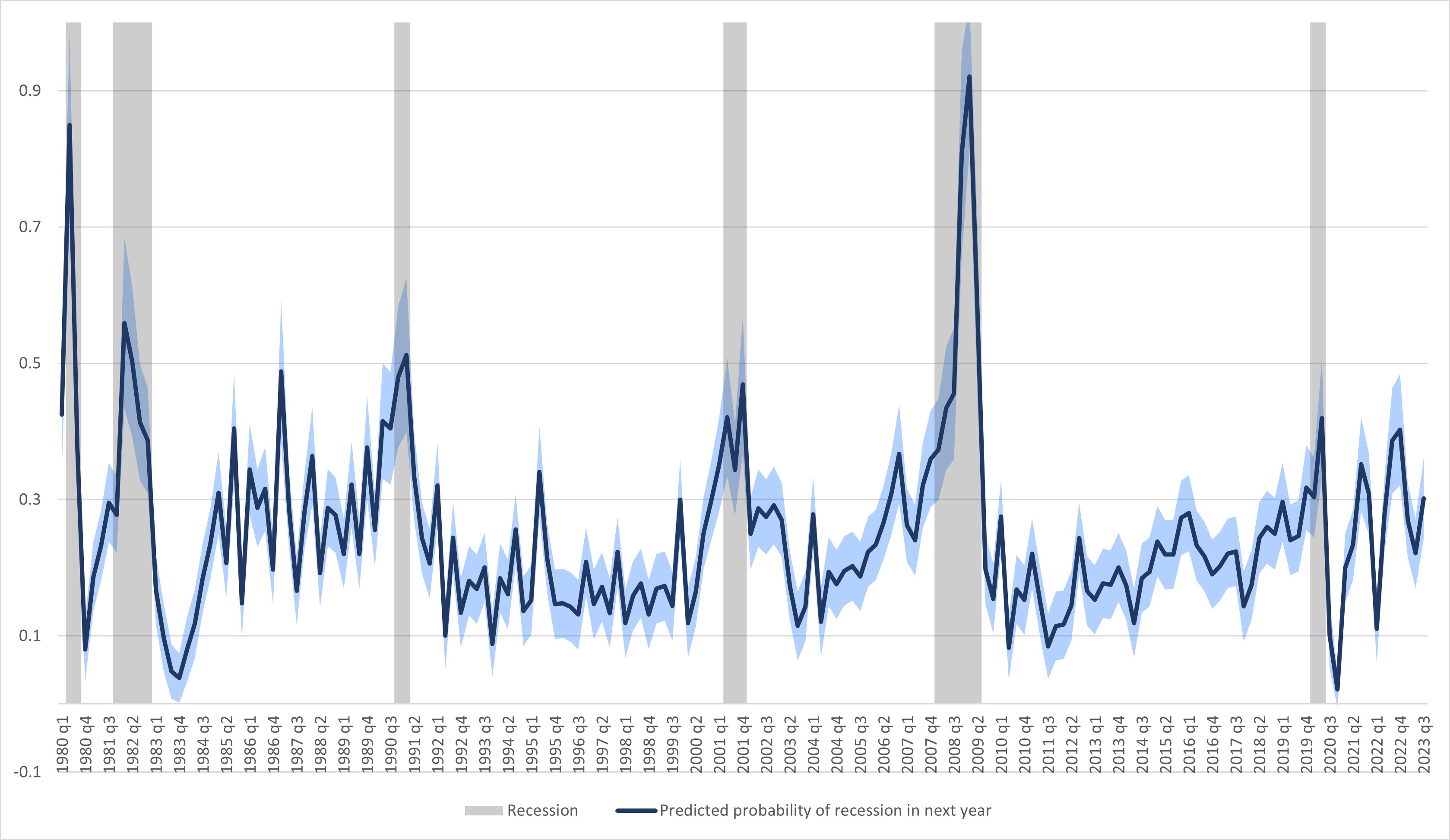

The leading indicator properties of durable goods consumption may be back if the post-recession normalization is over. To see what durable goods consumption is flagging for recession risk today, we calculated a probit model which relates quarter-over-quarter changes in the DLI against an indicator of recession in the next four quarters. We use this model to recover predicted recession probabilities, which are plotted in Figure 3 below.

Figure 3 shows that the latest quarter-over-quarter change in the DLI (-0.4 percent as of the third quarter of 2023) translates to a 30 percent probability of recession in the next four quarters. This is roughly the same probability flagged just before the 2020 pandemic recession and is at elevated levels compared to the 10 years before the pandemic recession.

While the historical record shows that recession does not always follow when the predicted probability hits 30 percent, the experience of the past five recessions suggests that the DLI is pointing to an economy that is in a more vulnerable state than the level of durable goods spending in the third quarter would suggest if viewed against the pre-pandemic trend.

Views expressed in this article are those of the author and not necessarily those of the Federal Reserve Bank of Richmond or the Federal Reserve System.

Contact Us